Nov 26, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Stop worrying about the world ending today. It’s already tomorrow in Australia.” – Charles Schulz

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s only Wednesday, but today is the last full trading day of the week, so it feels like a Friday. Futures look poised to extend the rally from last Friday into a fourth day with S&P 500 and Nasdaq futures up 0.2% after reclaiming their 50-day moving averages yesterday. The Nasdaq’s gain comes despite another 1% decline for Nvidia (NVDA), which has hit a rough patch of news in the last few days. After yesterday’s reports that Meta (META) was looking to purchase some AI chips from Alphabet (GOOGL) to diversify from NVDA, this morning, The Information is reporting that China continues to move away from NVDA chips, with the latest example being a government order blocking ByteDance from using NVDA chips in its datacenters.

Since markets are closed tomorrow, weekly jobless claims came out early this week, so after weeks of delayed reports, now we’re getting an early report! The early news was also good as both initial and continuing claims came in lower than forecast. Durable Goods and Cap Goods orders were also released and came in better than expected. Along with these reports, the Chicago PMI report for November comes out at 9:45.

Outside of equities, treasury yields are basically flat, with the 10-year yield right at 4%. Crude oil is fractionally lower again, while gold trades marginally higher, and bitcoin is lower.

Asian markets finished the mid-week session mostly higher. The lone exception was China’s Shanghai Composite, which saw a modest decline. South Korea led the region higher with a gain of 2.7% while Japan finished up 1.9%. European markets are mostly higher, with the STOXX 600 up 0.4%, but Germany is underperforming after the IMF says that the economy is likely to undershoot growth expectations given its current trajectory.

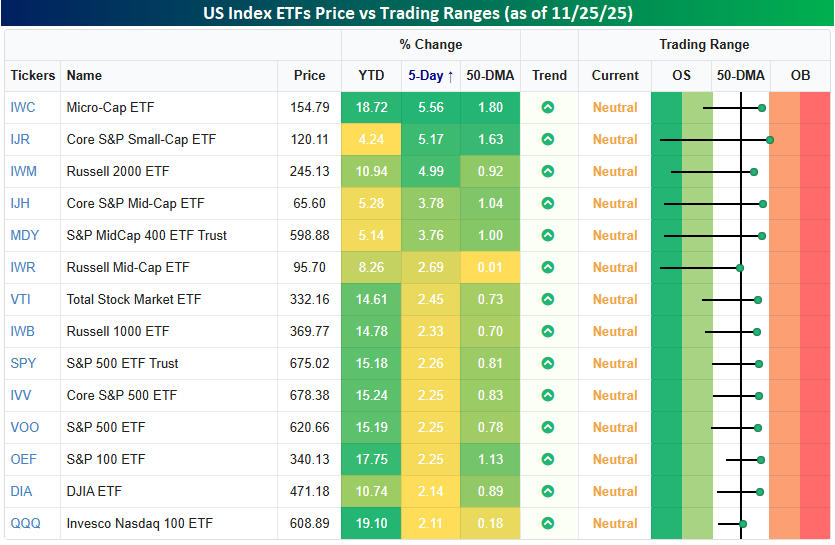

Whenever we hear the term “neutral,” we associate it with the word stuck giving it a negative connotation. There’s nothing negative about the neutral state of the major US equity indices, though, since it follows what were mostly oversold conditions last week at this time. As shown in the snapshot below, a week ago, all the index ETFs in our Trend Analyzer snapshot were below their 50-day moving averages, and most of them were oversold. As of yesterday’s close, none of them were oversold, and all of them were above their 50-DMAs. We’ll take neutral!

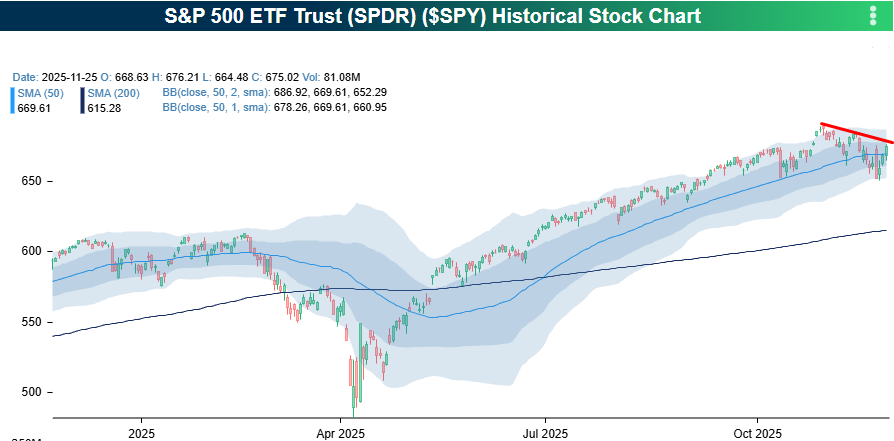

While bulls have welcomed the rebound in US equities, large-cap stocks still have more work to do before breaking the short-term downtrends that have been in place since the October highs. As shown in the two charts below, the S&P 500 ETF closed yesterday just below that downtrend line, while QQQ tested that downtrend yesterday and even peeked above it, depending on how hard you squint.

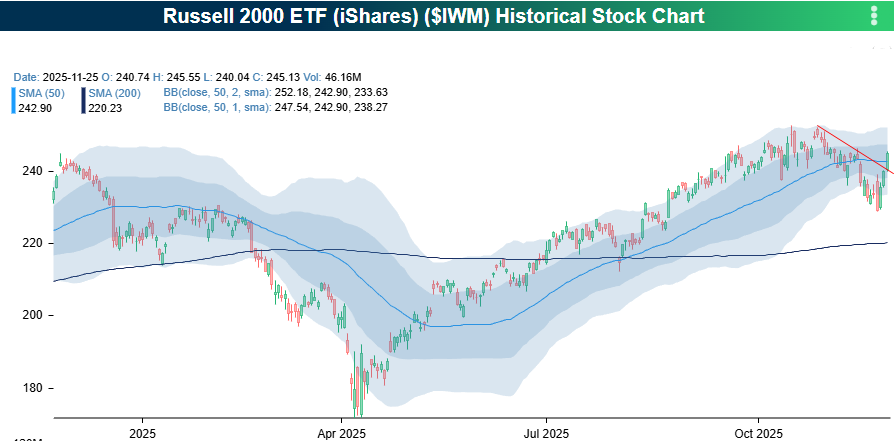

As the snapshot above illustrates, small-cap stocks have led the rally over the last five trading days with gains of about 5% compared to gains of about half that for their large-cap peers. With that outperformance, the Russell 2000 broke its downtrend from the October highs. Is this the long-awaited broadening we’ve all been waiting for?

Nov 25, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You have put me in here a cub, but I will come out roaring like a lion, and I will make all hell howl!” – Carrie Nation

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s an eventful morning in markets, but futures are little changed on all the cross-currents with the S&P 500 indicated to open up less than 0.10% while the Nasdaq is indicated to open down less than 0.10%. While futures on the Nasdaq are little changed, it comes are the index’s largest component – Nvidia (NVDA) – is down 5% while its third-largest component – Alphabet (GOOGL) – is up 4%.

Crude oil is down over 1% on reports of a truce in the Russia-Ukraine war while gold is up over 1%, and Bitcoin is down 2%. In Asia, major benchmarks were modestly higher, even as Softbank fell 10% as that stock corrects hard as investors question some of its massive and concentrated AI investments. In Europe, the tone is also muted with the STOXX 600 up 0.2%.

We also got some government economic data this morning, although it was from September, so it’s as stale as the bread you may be using for your Thanksgiving stuffing. Overall. the Retail Sales report for September was modestly weaker than expected while PPI was also slightly weaker.

It’s up again?

It’s up again!

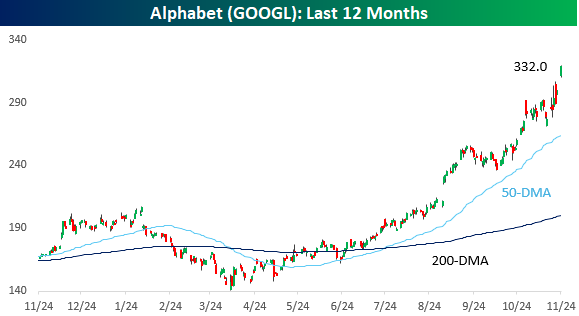

When it comes to Alphabet (GOOGL), whether you identify with the phrasing above that uses the question mark or the exclamation point depends on whether you own it or not. We’ve seen a lot of unbelievable moves in mega-cap stocks in the last few years, but the recent surge in GOOGL ranks right up there with any of the others. Following news reports this morning that Meta Platforms (META) is considering the purchase of Google TPU chips for its data centers in 2027, the stock is up another 4% this morning which would take its one week gain to 16.7%. After trading as low as $140 back in April, the stock is up over 135%.

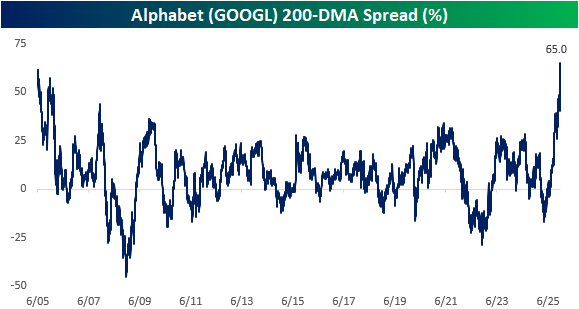

With the steep rally we have seen in GOOGL shares over the last few months, the stock is poised to trade 65% above its 200-DMA today. In the company’s entire history as a public company, that would be the most extended the stock has ever traded relative to its 200-DMA.

Besides the 135% rally off the April lows, over the last six months, GOOGL shares have rallied nearly 90%. The table below lists the ten largest gainers in the S&P 500 over the last six months, and GOOGL currently ranks eighth. In another sign that Tech and Communication Services still rule this market, the only two stocks on the list not from these sectors were Albemarle (ALB) and Robinhood (HOOD). What makes GOOGL stand out from the rest of the names is its market cap. At $3.8 trillion through yesterday’s close, GOOGL’s market cap is more than ten times larger than the next closest stock listed. It’s like an aircraft carrier sprinting with a fleet of skiffs.

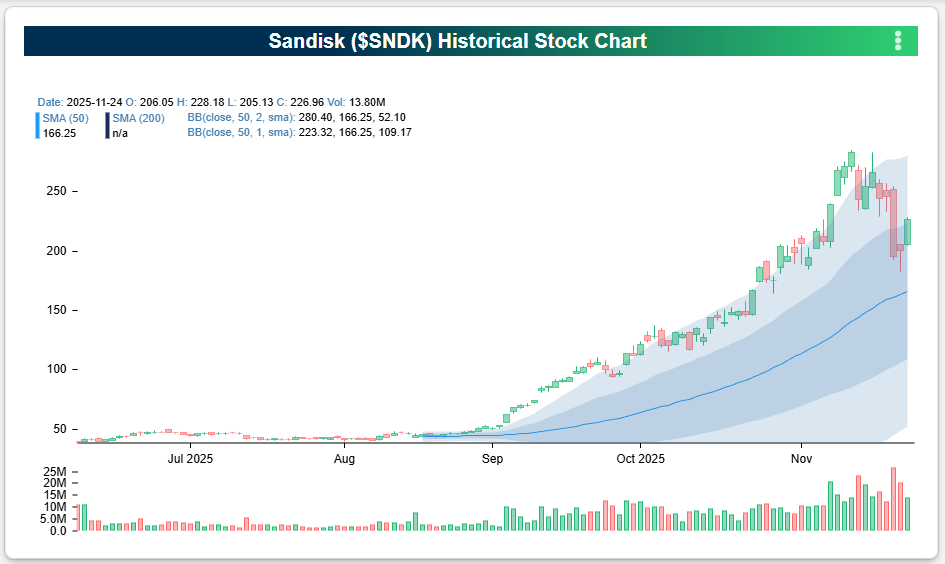

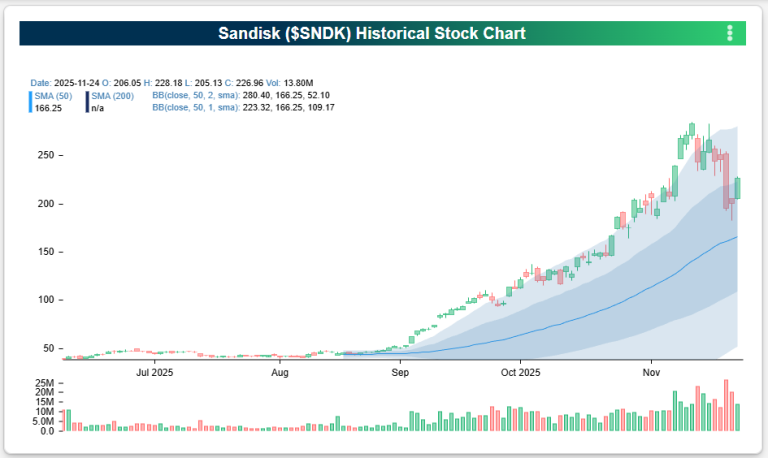

Last night after the close, news hit the tape that Sandisk (SNDK) would be added to the S&P 500 effective Friday (11/28). With the stock up nearly 500% over the last six months, the list of current top performers over the last six months is eating its dust. Looking at the chart below, it’s hard to imagine why, from a market timing perspective, anyone would think that now is a good time to add the stock to an index.

The people who make the decisions to add and subtract stocks to the various indices aren’t market timers, though. And while there are plenty of other stocks out there that would make worthy candidates, SNDK currently resides in the S&P 600 Small Cap Index. With a market cap of over $33 billion, though, it’s hardly a small cap, and it casts a large shadow over all the other stocks in the index in terms of size. After SNDK, the next largest stock in the S&P 600 is SPX Technologies (SPXC), but its market cap is less than a third of SNDK’s market cap. So, why not put it in the S&P 400 Mid Cap Index, you may ask. That would have been an option, but even in that index, SNDK would have already been the largest company in the index based on market cap. Even in the S&P 500, SNDK will still be larger than 228 of the index’s 500 components. Sometimes stocks become so large that there’s just nowhere else to put them!

Nov 24, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“No man becomes rich unless he enriches others.” – Andrew Carnegie

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Following a Friday rebound on the back of comments from NY Fed President John Williams that he was open to a rate cut at the December meeting, the week is starting on a positive note. S&P 500 futures have rallied 0.5% while Nasdaq futures point to a gain of 0.76% as shares of Alphabet (GOOGL) trade up another 3% following comments from Marc Benioff saying how much better Gemini 3 is than ChatGPT and that he’s ‘not going back’.

Japanese stocks were closed for a holiday, but Hong Kong stocks surged 2% while South Korean stocks declined modestly in what was a generally quiet session to start the week. European stocks are generally off to a quiet start this week as well. The STOXX is basically unchanged, while Germany (0.5%) leads and Italy (-1.0%) lags. One major weakness in the region, though, is the defense sector, as a potential end to fighting in the Ukraine war has that sector selling off. In terms of data, it’s been quiet. The only report was German Business confidence from ifo, which showed an unexpected decline from October, falling from 88.4 to 88.1 versus forecasts for an uptick to 88.6.

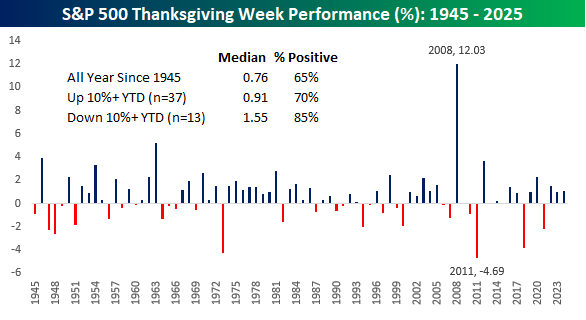

With the market only open for trading three-and-a-half days this week, it’s one of the shortest trading weeks of the year. With many on Wall Street usually taking Friday off, it’s only a three-day work week for many. It may be short, but Thanksgiving week has historically been strong. Since 1945, the S&P 500’s median performance during the week has been a gain of 0.76% with gains 65% of the time.

This year is the 38th time since 1945 that the S&P 500 was up by double-digit percentages heading into the week, and in the 37 prior years, the S&P 500’s median gain for Thanksgiving week was even stronger at 0.91% with positive returns 70% of the time. There have also been 13 years when the S&P 500 was down by double-digit percentages heading into Thanksgiving week. While you wouldn’t expect that investors would have had much to be thankful for in those years, the S&P 500’s median gain during the holiday week was a gain of 1.55% with positive returns 85% of the time.

As shown in the chart below, recent Thanksgiving week performance have also been positive. In the last three years, the S&P 500 rallied more than 1% in each Thanksgiving week, and it’s been positive during this week in eleven out of the last 13 years.

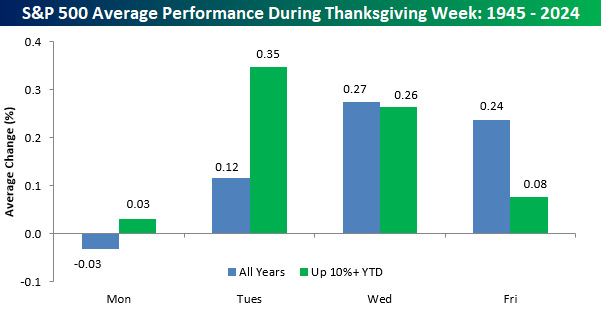

Looking at day-to-day returns, the chart below shows the S&P 500’s average performance during each day of Thanksgiving week for all years since 1945 and years when the S&P 500 was up 10%+ YTD. For all years since 1945, the strongest days of the week have been Wednesday and Friday (maybe you want to reconsider taking Friday off!), but in years when the S&P 500 was already up by double-digits, Tuesday and Wednesday were the best days of the week. One constant trend for Thanksgiving week? Monday was the weakest in terms of performance for all years and just years when the S&P 500 was already up 10%. What would you expect for a Monday?

Nov 21, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“To expect the unexpected shows a thoroughly modern intellect.” – Oscar Wilde

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

To view yesterday’s CNBC segment discussing yesterday’s sell-off and Nasdaq 5% pullbacks, in general, click on the image below.

After trading lower overnight, equity futures are higher across the board this morning following comments from New York Fed President John Williams, who says the Fed has room to lower rates in the short-term as weakness in the labor market poses a bigger risk than inflation. In response, S&P 500 futures are up 0.5% while Nasdaq futures are up slightly less. For both indices, the rebound is nowhere near enough to make up for yesterday’s declines, let alone getting us anywhere near the intraday highs from less than 24 hours ago.

Crude oil and 10-year yields are both lower, gold is basically flat, and crypto is seeing steep losses with Bitcoin and Ether both down about 4% while less ‘blue-chip’ coins in the space are down even more.

After yesterday’s weakness, it should come as no surprise that Asian stocks were creamed overnight, putting them all deep in the red for the week. European stocks are also lower, but not by the same degree, as the STOXX 600 is down 0.8%, but all major indices on the continent are on pace for weekly losses of at least 2%.

What started out yesterday as a Dr. Jekyll moment yesterday quickly turned into a Mr. Hyde event as the S&P 500, led by tech, turned a gain of nearly 2% into a decline of over 1.5%. Bulls started off the day strutting their stuff, got a little nervous as they headed out to lunch, and then came back ready to throw up.

Within the S&P 500, there were some major reversals. 13 stocks in the index closed more than 10% lower than their intraday high, which is nearly unheard of for large-cap stocks unless there’s a stock-specific event causing the move. Looking at the list of the biggest intraday reversals, not only were eight of them from the Technology sector, but most of the ones that aren’t were still AI-adjacent stocks.

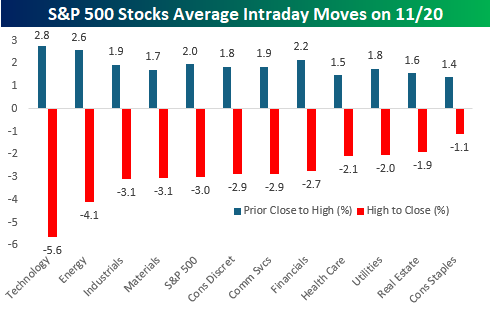

While tech led the reversal, it wasn’t solely about Tech. Within the S&P 500, 420 stocks traded down from the open to close, and the average stock in the S&P 500 finished the day down more than 3% from its intraday high. The chart below shows the average change of individual stocks yesterday from Wednesday’s close through the intraday high and then the intraday high to the close.

Tech stocks rallied the most initially, with an average gain of 2.8% and then reversed an average of 5.6% from the open to close. Besides Technology, though, the only two sectors where the average decline from the intraday high to the close was less than 2% were Consumer Staples (-1.1%) and Real Estate (-1.9%). In three sectors besides Technology (Energy, Industrials, and Materials), the average decline was more than 3%. So, again, Tech led the way but it had plenty of company.

Nov 20, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Great ideas come from everywhere if you just listen and look for them. You never know who’s going to have a great idea.” – Sam Walton

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Strong results from Nvidia (NVDA) have pushed global markets higher. The stock is trading up over 5% in the pre-market, and as a result, S&P 500 and Nasdaq futures are both trading more than 1% higher. Even Russell 2000 futures, which have no exposure to NVDA, are up over 1%. Heck, the Dow is even trading higher!

International markets were also higher overnight in Asia and this morning, with gains of mostly 1% or more. Treasury yields are basically unchanged, crude oil is back to $60 per barrel, gold is flat, and crypto assets are up at least 3%.

We’re finally getting some economic data this morning, and the main report was the September Non-Farm Payrolls report, which showed 119K jobs created versus forecasts for an increase of 50K. Despite the larger-than-expected increase, the Unemployment Rate ticked up to 4.4% versus estimates of 4.3%. More timely data on jobless claims came in at a relatively benign 220K.

In his last press conference following the Federal Reserve’s October meeting on 10/29, Fed Chair Powell made comments regarding the consumer, noting that “Data available prior to the shutdown show that growth in economic activity may be on a somewhat firmer trajectory than expected, primarily reflecting stronger consumer spending.” He then went on to simply state, “Consumers are still spending.”

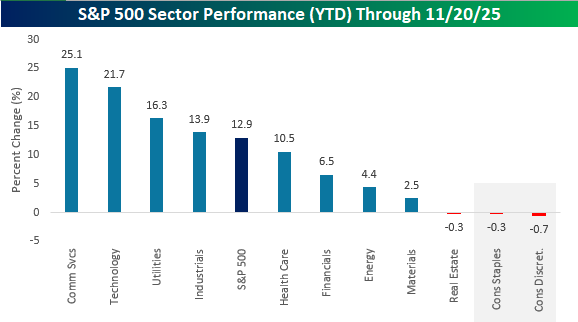

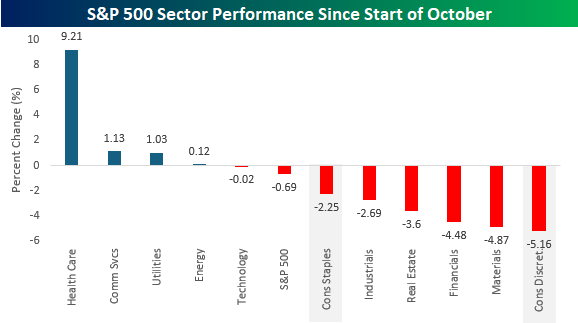

Based on data that the Federal Reserve has, consumer activity still looks strong, but the stock market seems to be sending a different message. The chart below shows YTD sector performance, and while the S&P 500 is still up close to 13% on the year, the Consumer Discretionary sector is the worst performer, and Consumer Staples is tied for the second worst. Both sectors are also two of just three sectors down on the year.

While neither consumer sector was a market leader at any point this year, both sectors have seen significant underperformance since the start of October, when the government shutdown started. While only four sectors are higher, Consumer Staples is down three times more than the S&P 500, and Consumer Discretionary is the worst-performing sector with a decline of 5.2%.

Nov 19, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“What we anticipate seldom occurs, what we least expected generally happens.” – Benjamin Disraeli

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After rallying off the morning lows yesterday, the major averages rallied back near the unchanged line but then drifted lower in the final hour of trading. This morning, equity futures are fractionally higher, while the 10-year yield is unchanged. Crude oil is sharply lower with a decline of 2.7% down to $59 per barrel on reports that the US and Russia may be near an agreement to end the war in Ukraine. Lower oil prices should be a welcome signal for anyone worried about inflation.

In Asia overnight, it was a mixed session with no major index up or down 1%, so maybe we’re starting to see some stabilization following a couple of days of weakness. It was a similar picture in Europe, as the STOXX 600 is up 0.1% and no major country benchmark is up or down 0.5%. Eurozone CPI increased 0.2% m/m in October, which was slightly higher than the 0.1% forecast, but core CPI was right in line with expectations, rising 0.3%.

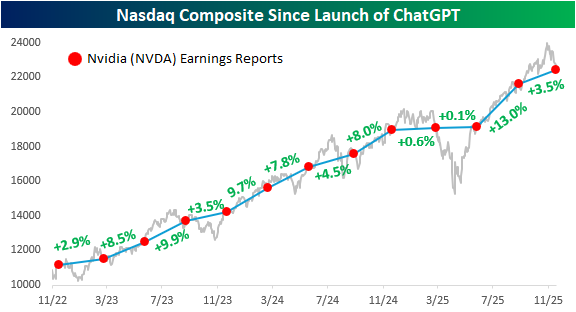

Tom Petty said, “waiting is the hardest part,” and the market and investors can’t wait for Nvidia (NVDA) earnings after the close in hopes that it will help to get the market rally back on track. While results are widely expected to be good, if not great, the stock’s reaction will say a lot about the market’s posture heading into year-end.

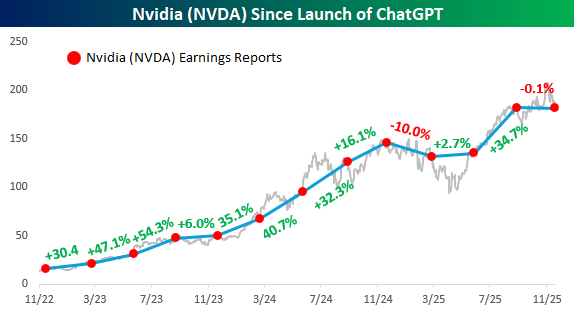

The chart below from yesterday’s Chart of the Day shows the performance of Nasdaq since the launch of ChatGPT, and each red dot indicates days when Nvidia (NVDA) reported earnings. The label between each pair of dots shows how the S&P 500 performed in that span. What’s amazing about the last three years is that in every period between NVDA earnings reports, the Nasdaq has traded higher. That kind of consistency is extremely uncommon and won’t last forever.

Below we show the same chart but have swapped out the Nasdaq for NVDA. While NVDA’s run has been impressive, it hasn’t traded higher between each of its earnings reports over the last three years. It fell 10% from last November to March of this year, and through yesterday’s close, it’s once again on pace for a decline, although a much more modest one than three quarters ago. If there’s one takeaway from the chart, the smooth, seemingly uninterrupted pace of gains since the launch of ChatGPT has ended.