Apr 15, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers BlackRock’s (BLK) Q1 2026 earnings call.

BlackRock (BLK) is the world’s largest asset manager, overseeing trillions across ETFs (iShares), active funds, private markets, and its Aladdin risk/portfolio technology platform. The company delivered a strong Q1 with $130B in net inflows, 8% organic base fee growth, and 27% revenue growth. The call centered on three big ideas: (1) clients consolidating assets with fewer firms, benefiting BlackRock’s “whole portfolio” model; (2) private credit demand staying strong on the institutional side despite some retail noise, with spreads widening and opportunity improving; and (3) retirement reform, especially the push to bring private assets into 401(k)s, as a major long-term growth driver. Management also highlighted rising demand for international exposures, continued momentum in ETFs and direct indexing (Aperio), and the role of AI in driving infrastructure investment and data needs. Shares rose 3.1% on 4/14 in reaction to the better-than-expected results…

Continue reading our Conference Call Recap for BLK by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Apr 15, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Citigroup’s (C) Q1 2026 earnings call.

Citigroup (C) is one of the world’s largest financial institutions, providing banking, payments, trading, and wealth management services to corporations, governments, and consumers across more than 90 countries. Citi delivered a strong Q1 with $5.8B in net income and 14% revenue growth, driven by standout performance in Services (+17%) and Markets (best quarter in a decade, equities +40%). Management emphasized resilience in US consumers (card spend +5%, improving credit) while flagging rising macro risks from Middle East conflict and inflation. Services continue to be a key differentiator, with mandates up 40% and cross-border activity +12%, reinforced by investments in tokenization and real-time payments. Investment banking remains active, especially M&A, though sponsors are more cautious. The stock was up 2.7% on 4/14 after posting better-than-expected results, and it’s up almost 23% since 3/30…

Continue reading our Conference Call Recap for C by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Apr 15, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We contend that for a nation to try to tax itself into prosperity is like a man standing in a bucket and trying to lift himself up by the handle.” – Winston Churchill

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

In an unusual picture relative to the post-war periods, US equity futures aren’t showing much in the way of gains or losses. Treasury yields and crude oil are modestly higher, while gold and Bitcoin are slightly lower. Asian stocks were higher overnight, and European stocks are mixed in early trading. Empire Manufacturing and Import Prices both just hit the tape, wth Empire exceeding forecasts while Import Prices came in weaker than expected.

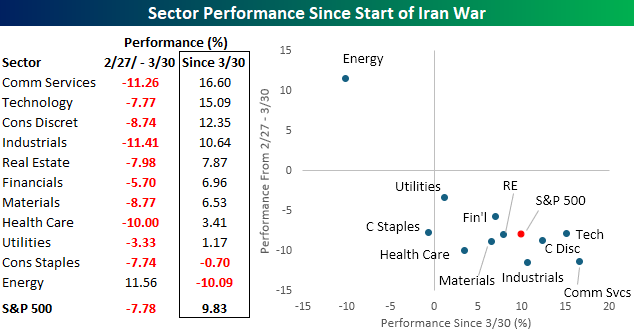

It’s been ten trading days since the S&P 500’s Iran war low, and during that time, the index has rallied just under 10%. Along with that impressive gain, four sectors have rallied more than 10%, including Communication Services and Technology, which are up over 15%. Not bad for two weeks! It’s been almost an everything rally over the last two weeks as the only two sectors to trade lower are Energy and Consumer Staples, although while the latter has only experienced a marginal decline, the former is down over 10%.

Sector moves over the last two weeks have largely been a reversal of the moves since the start of the war. Energy was the only sector to rally from 2/27 through 3/30, and it’s easily the worst performer since then, erasing all its Iran war gain. Conversely, the Technology sector has also more than erased its losses from 2/27 through 3/30. Technology is also a standout. It held up relatively well on the way down (5th best performing sector), but it has still been the second-best performing sector on the way up. Another notable sector has been Consumer Staples. While no sector traded higher in both the periods from 2/27 through 3/30 and since 3/30, Consumer Staples is the only sector to trade lower in both periods.

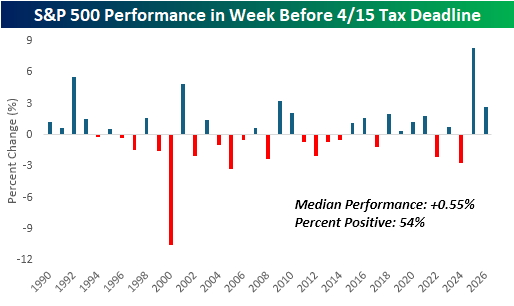

Have you done your taxes yet? With today being the Federal Tax deadline, we wanted to highlight the S&P 500’s performance leading up to and after 4/15. The chart below shows the performance of the S&P 500 in the week before 4/15, dating back to 1990. During that period, the S&P 500’s median performance has been a gain of 0.55% with positive returns 54% of the time. Just looking at the chart, the market has been trendless leading up to the tax deadline.

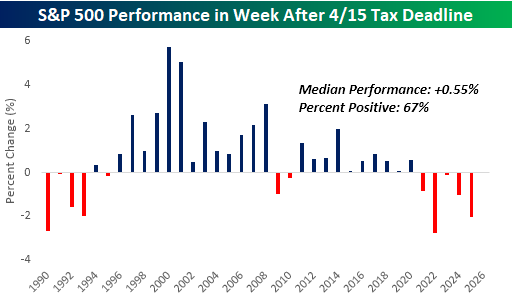

Market performance in the week after Tax Day has shown an evolving pattern over the last several years. While the S&P 500’s median performance in the week after 4/15 has been the same as its performance in the week before Tax Day, there has been a weakening pattern since the turn of the century. The S&P 500’s post-Tax Day performance peaked with a 5.75% gain in the week after Tax Day in 2000, and since then, it has been gradually trending lower to the point where the S&P 500 has declined in the week after for five straight years.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Apr 14, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Goldman Sachs’ (GS) Q1 2026 earnings call.

Goldman Sachs (GS) is a leading global investment bank and financial services firm. The company posted ROE of 19.8%, driven by heavy client engagement as volatility picked up late in the quarter. Trading and financing grew as clients repositioned portfolios amid geopolitical tension, AI disruption concerns, and energy market swings. M&A activity remained highly resilient with a strong backlog, while IPOs and sponsor activity lagged but are expected to rebound. Private credit was a major focus given rising concerns around retail fund outflows and where the industry stands in a late-stage credit cycle, but Goldman pushed back on the narrative, highlighting that its exposure is heavily institutional, spreads are becoming more lender-friendly, and a downturn could actually create better deployment opportunities. The firm is leaning into financing growth (record lending, strong Asia expansion) while investing heavily in AI infrastructure to drive efficiency and long-term growth. Management flagged AI capex, regulatory easing, and fiscal stimulus as key tailwinds, but noted rising uncertainty from geopolitics and energy prices. GS recorded better-than-expected EPS and revenue, though shares fell 1.9% on 4/13…

Continue reading our Conference Call Recap for GS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Apr 14, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The clouds appeared and went away, and in a while they did not try anymore.” – John Steinbeck

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Can we make ten in a row? Along with the Dow and S&P 500, futures on the Nasdaq indicate a gain of over 0.5% at the open, and if those gains hold throughout the session, it would be the Nasdaq’s 10th day in a row of gains. Treasury yields are little changed, but at 4.299%, the 10-year yield is still well off its recent highs. Oil prices are also down over 2% to below $97 per barrel on reports Iran may pause shipping in the Strait of Hormuz to keep potential talks later this week from falling apart. As has been the case recently, signs of easing tensions have also put a bid under gold with the metal up 0.65% to $4,800 per ounce. Lastly, Bitcoin is up another 2% this morning and back above $74K to its highest level since St. Patrick’s Day. If those gains hold, it would also break the downtrend that has been in place since the highs late last year.

After a sluggish start to the week for Asian markets, the region surged overnight with the Nikkei up over 2%, while South Korea’s KOSPI rocketed 2.7% higher. Chinese stocks rallied more than 1% despite a stronger-than-expected trade surplus as imports surged 27.8% y/y compared to expectations for an increase of 11.1% while exports rose less than expected (2.5% vs 8.3%).

European stocks are also higher, although not by as much as in Asia. The STOXX 600 is up 0.6% with Germany leading the way higher (+1.0%) while the UK lags (+0.1%). One area of weakness in the region is the luxury goods sector, where weak results from LVMH drag that group lower.

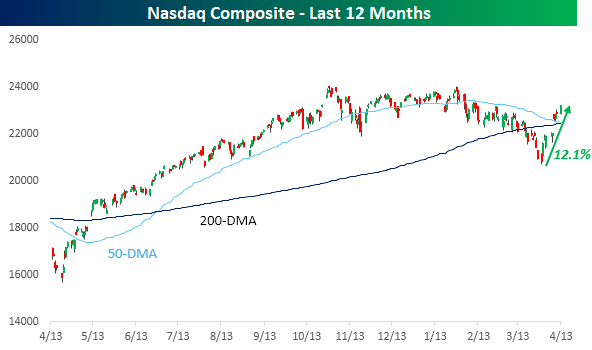

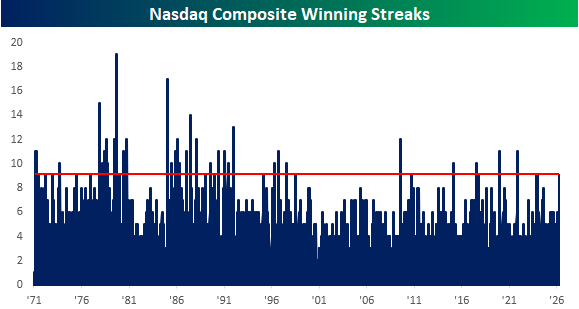

The Nasdaq has now rallied over 12% since its intraday low on 3/30, and the rally ironically comes just as the index’s 50-day moving average (DMA) looks to cross down through its 200-DMA. That’s traditionally considered a bearish development, although history shows that theory is misplaced.

Since the rally off the March 30 lows, the Nasdaq hasn’t had a down day, rallying for nine straight days. That’s tied for the longest winning streak in the index since November 2021, and if today’s pre-market gains hold, it would be the index’s 34th double-digit winning streak. As shown in the chart below, these types of streaks were relatively common in the 1970s and 1980s, but their frequency has waned since 2000.

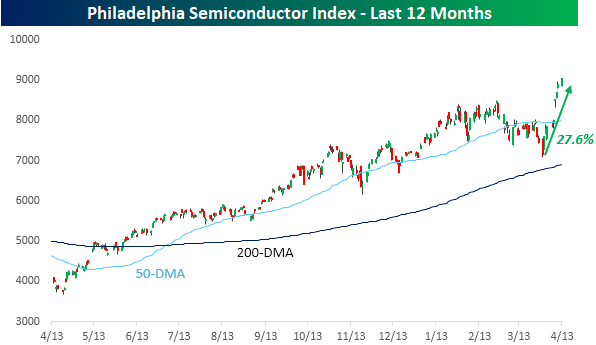

One driver of the Nasdaq’s gains has been semiconductors, which have been cooking. Since its low on 3/30, the Philadelphia Semiconductor Index (SOX) rallied an impressive 27.6%. Making this even more impressive is that the index’s largest component – Nvidia (NVDA) – has rallied just 15% off its intraday low on 3/30. One stock in the sector stealing the show has been Intel (INTC), which, as we noted yesterday, has had its largest nine-day rally in at least 40 years. Whatever stock has been driving the SOX, the index has more than erased its declines from the Iran war and now trades at record highs.

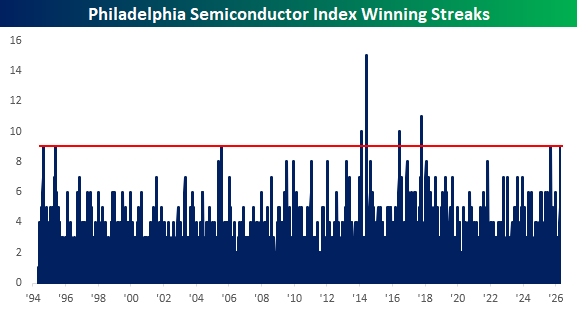

Like the Nasdaq, yesterday’s rally took the SOX’s winning streak to nine days. That’s already tied for the longest winning streak since 2017, and if today’s pre-market gains hold, it would be just the fifth double-digit winning streak in the index’s history.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Apr 13, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Nothing gives one person so much advantage over another as to remain always cool and unruffled under all circumstances.” – Thomas Jefferson

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The week hasn’t even started yet, but it’s been volatile already as equity futures gapped down more than 1% at the open last night and then rallied right up until around 7 AM when Goldman (GS) reported. That stock is down over 4% in pre-market trading, and the S&P 500 is now set to gap down 0.63%.

The culprit behind this morning’s weakness is once again the Middle East, as President Trump’s plan to put a blockade on the Strait of Hormuz has crude oil up over 7% and back above $100 per barrel. With crude oil up as much as it is, you could argue that equities should be down more based on the relationship between the two since the war started, but as earnings season kicks off, the market is starting to trade on more than just oil prices.

In Asia and Europe overnight and this morning, the overall trend is lower as major averages on both continents declined or are trading down about 1%. Gold prices are also trading down about 1%, while Bitcoin is only fractionally lower, just below $71K.

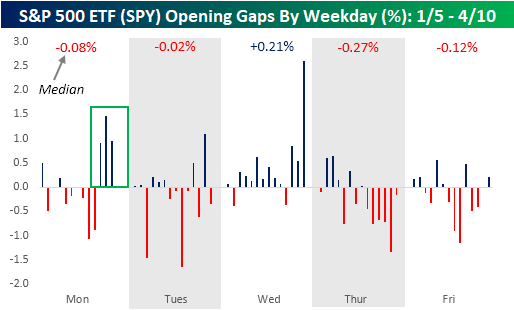

As mentioned above, futures are off the initial lows from last night, but with the S&P 500 ETF (SPY) on pace to gap down 0.62% at the open, it would be the third-largest downside opening gap on a Monday of the year. It would also break a streak of four straight weeks where the market gapped higher on a Monday. Even during a war, Mondays haven’t been that bad lately. For the entire year, though, SPY’s median gap on Mondays has been a decline of 0.08% with positive returns half of the time.

The weakest day of the week in terms of where the market opens has clearly been Thursday. For the entire year, the average downside gap on Thursdays has been a decline of 0.27%, and since the war started, SPY has gapped down on every Thursday. As bad as Thursdays have been at the open, Wednesdays have been solid. On the 14 Wednesdays so far in 2026, SPY has gapped higher 12 times for a median gain of 0.21%.

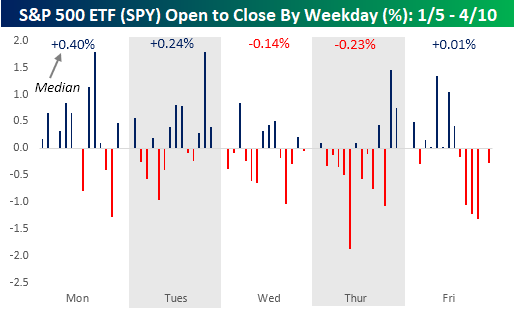

Where the market opens is one thing, but where it goes for the next 6.5 hours from the open to close is just as important. While Mondays have been modestly negative at the open, it has been the best day of the week from the open to close with a median gain of 0.40% and positive returns 75% of the time. With a median open-to-close gain of 0.24%, Tuesdays haven’t been as bad either. From there, though. The trading day only goes downhill from there, though. SPY’s median change from the open to close on Wednesday has been a decline of 0.14%, with positive returns barely more than a third of the time. Thursdays are even worse with a median decline of 0.23%. While Friday’s median open-to-close change has been slightly positive, since the war started, SPY has declined from the open to close on Fridays every time for a median decline of just over 1% (-1.04%).

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.