Feb 12, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Volatility obscures the future but does not necessarily determine the future.” – Peter Bernstein

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Bespoke’s Paul Hickey appeared on CNBC’s Worldwide Exchange this morning to discuss AI disruption and other issues impacting the market. To view the segment, click on the image below.

US equity futures are higher across the board this morning, with gains ranging from 0.25% to 0.30%. Treasuries are also catching a bid with the 10-year yield falling 2 basis points to 4.16%. Oil prices are taking a rest and trading down fractionally, which is also the case for gold and silver. Crypto is catching a modest bid with Bitcoin prices inching up towards $68K.

In Asia, it was a mixed session. The Nikkei was down 0.02% after being closed for a holiday yesterday, but South Korean stocks were higher again as the KOSPI rallied 3.1%. Those types of moves for a major country benchmark were once considered out of the ordinary, but lately, multi-percentage point moves in the KOSPI (mostly to the upside) have become commonplace.

In Europe, stocks are trading higher across the board. The STOXX 600 is up 0.4%, and the German DAX is leading the gains with a rally of 1.3%. UK GDP for Q4 was weaker than expected, but outside of some individual earnings reports, it’s been a quiet session.

Here in the US, it’s also a quiet day for data. The main report will be jobless claims at 8:30, followed by Existing Home Sales at 10. Since it’s Thursday, the weekly individual investor sentiment survey from AAII showed that optimism towards the stock market fell for the second week in a row to 38.5%, its lowest level since Christmas. Bah humbug!

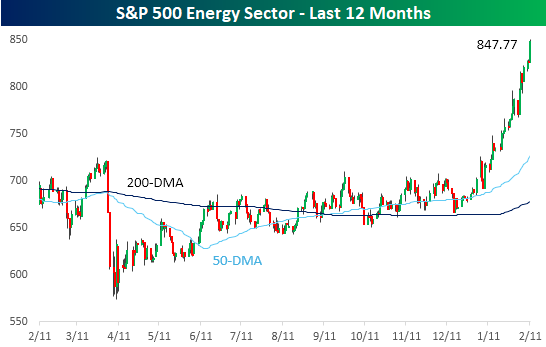

You need energy for a rocket to lift off, and boy, does the Energy sector have a lot of it! After essentially trading rangebound for the second half of 2025, the sector broke out in mid-January and has been gaining altitude ever since.

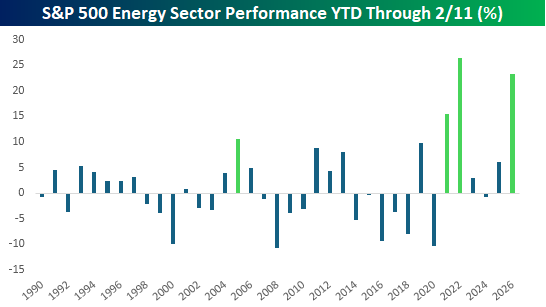

While most sectors have outperformed the S&P 500 YTD, none of them hold a candle to Energy’s gain of over 23%. Since sector data begins in 1990, this year’s gain ranks as the second-best start to a year through 2/11, trailing only the 26.5% gain to start 2022. That was a bit of a different situation, though, as the market was gearing up for Russia’s invasion of Ukraine. This year also now ranks as just the fourth year since 1990, that the Energy sector was up at least 10% YTD through 2/11. The others were 2021 and 2005.

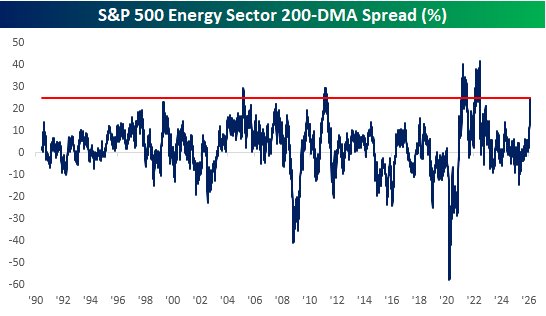

As the sector’s price has gone parabolic over the last few weeks, the spread between the Energy sector’s price and 200-DMA has ballooned to one of its highest levels on record. The only times it was wider were in 2005, 2011, 2021, and 2022.

Feb 11, 2026

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a deep dive into the employment situation report (pages 1 – 3). We then review markets action today including the moves in bonds, the dollar, tech stocks, and more (pages 4 and 5). We cap off with an update on the latest petroleum inventory data (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Feb 11, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The greatest minds are capable of the greatest vices as well as of the greatest virtues.” – Rene Descartes

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Anticipation is the word of the morning, as markets waited for the delayed January jobs report. Heading into the report, S&P 500, Nasdaq, and Dow futures were all up a modest 0.10%. The 10-year yield was down a basis point to 4.13%, and crude oil was up over 2% and back above $65 per barrel. Precious metals are back in rally mode as gold rallies 1.5%, silver surges 6%, and Platinum rises 4%. Crypto, meanwhile, is struggling as Bitcoin pulls back 3% and trades back below $67. Metals rallying, crypto falling? Looks like things are getting back to normal!

The January payrolls report just hit the tape, and it was higher across the board. Non-Farm Payrolls were twice as much as expected (130K vs 65K), while the Unemployment Rate dropped to 4.3% 4.4% expected. Average hourly earnings and the average workweek were also both higher than expected. In response to the report, the 10-year yield ripped higher to just under 4.2% while equity futures added to their gains.

Japan was closed overnight, but most other major benchmarks in the region finished the session higher, with Australia rallying 1.6% while South Korea added another 1.0%. South Korea reported an 44.4% y/y increase in exports during the first ten days of February, aided by a 138% increase in chip exports. In China, January CPI came in weaker than expected, rising 0.2% versus an expected 0.3% increase.

In Europe, the STOXX 600 isn’t closed, but it’s unchanged on the session. The FTSE 100 is up nearly 1%, but every other major benchmark in the region is lower. It’s been a quiet session in terms of economic data, with Italian Industrial Production (better than expected) being the only major report on the calendar.

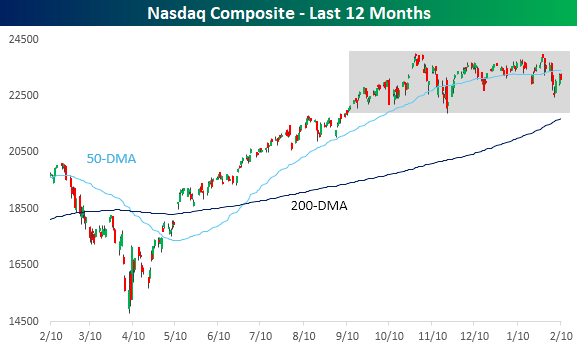

If I told you that software stocks had lost a third of their value over the last five months, you’d say the Nasdaq was in a deep correction, at minimum. Conversely, if I told you that the number of stocks hitting new 52-week highs was routinely at the highest levels in at least a year, you’d be asking when the Nasdaq crossed 25,000. Well, both trends outlined above have played out, but neither assumed result has played out for the Nasdaq, as both forces have essentially cancelled each other out, creating a period of stasis that has been going on for the last five months.

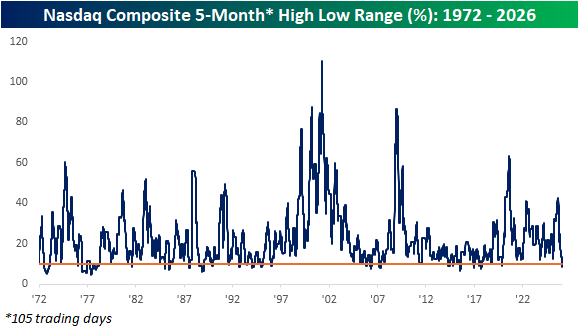

With the Nasdaq basically going nowhere since September, the spread between the index’s closing high and low recently dropped below 10%, and as of yesterday’s close, it was just 8.7%. That’s the first time that the five-month trading range dropped below 10% since 2019, and the narrowest range since October 2017. Back in the mid-teens, the Nasdaq’s five-month range was routinely below 10%, but since 1972, it has only occurred on less than 10% of all trading days.

Feb 10, 2026

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with a review of the latest labor market data including ADP and ECI figures (page 1). Then we recap the latest retail sales report the day’s Fedspeak (page 2). Next up is a recap of the latest earnings reports including those results from Ford (F), Lyft (LYFT), Robinhood (HOOD), and more (page 3). We then give a follow up on today’s Chart of the Day in looking at that S&P 500’s tight trading range (page 4) before capping off with an update of the latest sentiment data (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Feb 10, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We are all wrong so often that it amazes me that we can have any conviction at all over the direction of things to come.” – Jim Cramer

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After two big days of gains, investors are taking some profits this morning as futures on the major averages are all down a modest 0.2% or less. Bonds are catching a bid, though, as the 10-year yield is all the way down to 4.17% after testing 4.3% yesterday. Oil prices are modestly higher, while precious metals are modestly lower, with gold and silver each down less than 1%. When was the last time each of those moved under 1% on the same day?

In international markets, Asia was positive with Japan surging another 2%, while other major benchmarks were all up less than 0.5%. In Europe, the tone is also modestly positive, with the STOXX 600 up 0.1% while no other major benchmark is up or down more than 0.3%.

In the US today, small business sentiment unexpectedly fell in January, and at 8:30, we got the latest reports on the Employment Cost Index and Retail Sales. ECI was weaker than expected, and Retail Sales (for December) came in well below forecasts.

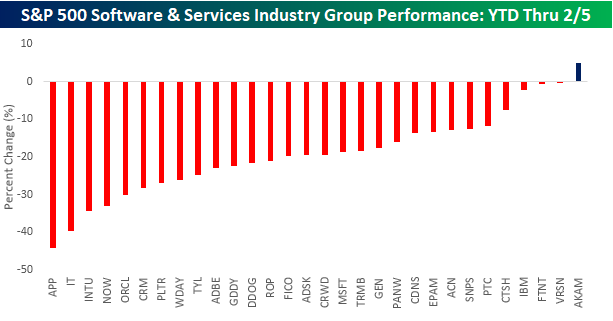

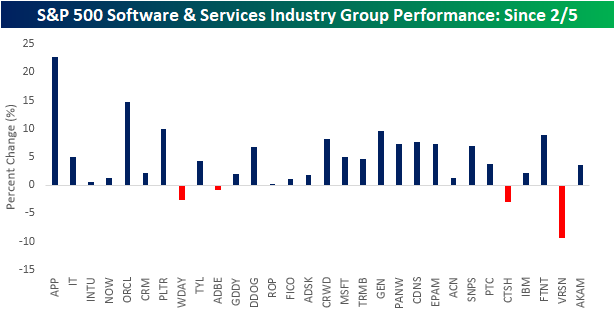

Through last Thursday’s close, the S&P 500 Software and Services Group was easily the worst-performing industry group in the S&P 500. With a decline of over 20% YTD, the group was down more than twice as much as the next closest group (Autos & Auto Parts). Over the last two days, Software has bounced back sharply, rallying more than 5%, but Semiconductors, which weren’t down nearly as much YTD heading into last Friday, are up by more than 8%!

Within the Software group, we wanted to look at which stocks led it to the downside and whether the rebound has been a reversal of the YTD trend or have investors become more discerning, trying to decipher the winners from the losers. The chart below shows the YTD performance of the industry group’s components through last Thursday’s close. Leading the way down was AppLovin (APP), which was down a staggering 44% through last Thursday. Along with APP, Gartner (IT), Intuit (INTU), ServiceNow (NOW), and Oracle (ORCL) were all down 30% for the year! In terms of winners, there practically weren’t any as Akamai (AKAM) was the lone stock in the group up YTD.

After sharp declines like we have seen in software stocks this year, when you see a bounce, it’s usually the biggest losers that bounce the most, while the stocks that held up the best don’t see nearly the juice. Based on that logic, you would expect the stocks mentioned above that were down 30% YTD to be up the most over the last two days, while a stock like AKAM would underperform. Looking at how the group’s stocks have performed in the last two trading days, that hasn’t exactly played out.

With gains of 22.7% and 14.7% since last Thursday’s close, APP and ORCL have been two of the best performers during the current bounce, but the other three stocks that were down over 30% have all either performed in line with or below the average performance of stocks in the group. At the other end of the spectrum, even after rallying YTD through last Thursday, AKAM still managed to rally in the last two trading days. Not only that, but stocks in the group that held up relatively well during the pullback this year have also outperformed on the way up.

The fact that we haven’t simply seen the biggest losers YTD bounce the most over the last two trading days, and vice versa, can be interpreted as a healthy sign suggesting that rather than indiscriminately going in and buying whatever is down the most, investors have been more discerning in their actions, attempting to weed out the ultimate winners and losers. Whether they end up being right is a big if, but it still strikes us as a healthy sign.

Feb 9, 2026

Log-in here if you’re a member with access to the Closer.

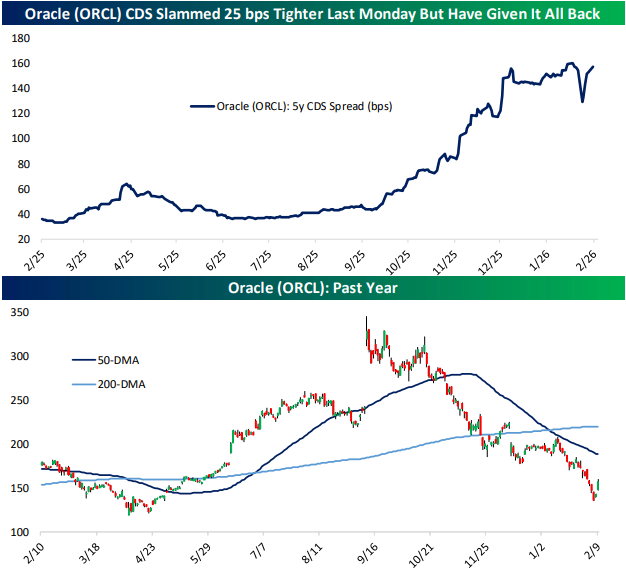

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a look at the sale of $20bn of debt from Alphabet (GOOGL) in addition to an update on Oracle (ORCL) credit spreads (page 1). Next up, we show the bounce in AI driven names (page 2). We then recap the latest findings of the New York Fed’s Survey of Consumer Expectations (pages 3 and 4) before capping off with a review of the latest positioning data (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!