May 11, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The toughest thing about success is that you’ve got to keep on being a success.” – Irving Berlin

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures point to a lackluster start to the new week as the S&P 500 and Nasdaq are both indicated to open the week 0.10% lower. Given the move higher in crude oil, though, it could be worse. WTI is trading up over 3% to more than $98 per barrel after the US rejected Iran’s latest peace proposal as a non-starter. The 10-year yield is nearly 3 bps higher but still under 4.4%, while gold is down over 1%, and Bitcoin is fractionally higher.

Overnight in Asia and Europe this morning, it’s been a negative start to the week on the Iran news, but in the US, attention will likely shift from the Middle East to inflation – at least in the short term – with Tuesday’s release of CPI and Wednesday’s PPI.

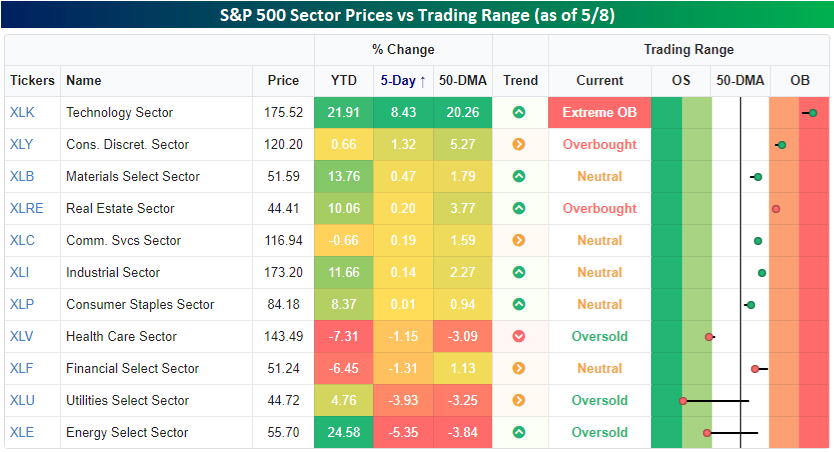

Every week is interesting, but last week’s breadth was a standout. The S&P 500 finished 2.33% higher, but mega caps did most of the heavy lifting as the average stock in the index finished the week higher by just 0.64%. Check out the snapshot below from our Trend Analyzer showing each sector’s performance and where they traded relative to their trading ranges. Again, while the S&P 500 was up over 2%, the only sector that outperformed the index was Technology, and with a gain of 8.43%, it outperformed by a lot! The only other sector that rallied more than 1%, though, was Consumer Discretionary (+1.32%), and no other sector even finished the week higher with a gain of 0.5%.

Not only did most sectors underperform last week, but more sectors were down 1% than up 1%. In fact, there were just as many sectors that finished down by over 3% – Energy and Utilities – as there were that finished up at least 1%!

Where each sector settled out the week relative to its trading range also varied widely. While Technology heads into the new week at ‘extreme’ overbought levels, Utilities is right on the cusp of ‘extreme’ oversold levels, and Energy and Health Care also finished the week at oversold levels.

However weak overall breadth was, a gain is a gain, and the S&P 500, Nasdaq, and Russell 2000 now all have winning streaks of at least six weeks. Six-week winning streaks aren’t that out of the ordinary for any of the three indices on their own, but for all three to have one simultaneously is much less common. Since the Russell 2000 started in 1979, there have only been ten other periods.

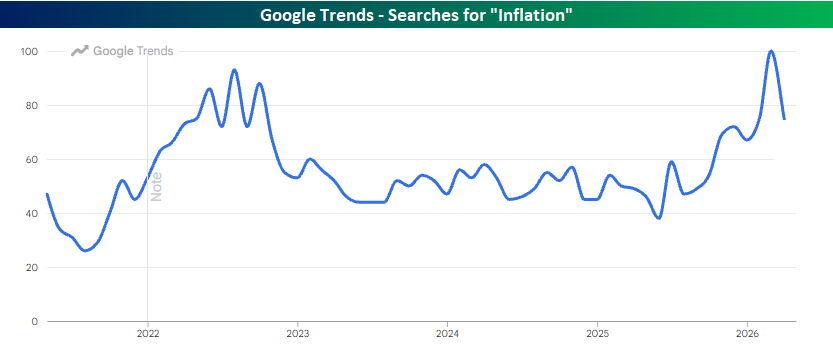

Finally, inflation will be a big topic this week with the release of CPI on Tuesday and PPI on Wednesday. Obviously, the market is expecting big upticks in inflation. What surprised us, though, is the uptick in search activity related to inflation. According to Google Trends, searches for “inflation” during March surpassed the peak levels seen during 2022 when CPI surged as high as 9.1% y/y. For tomorrow’s CPI, economists are only forecasting an increase to 3.7% from 3.4% in April.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 8, 2026

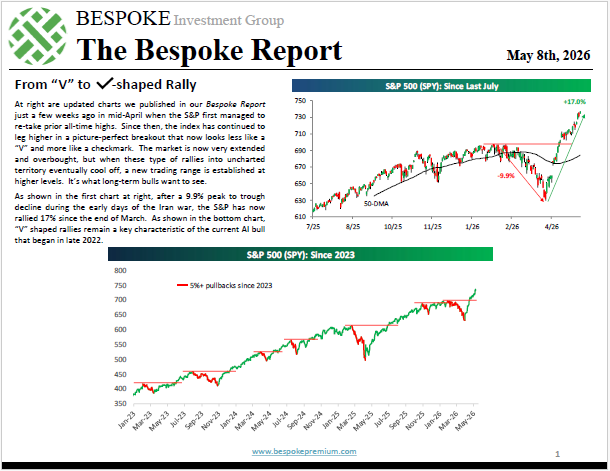

The S&P has continued to leg higher in a picture-perfect breakout that now looks less like a “V” and more like a checkmark.

The market is now very extended and overbought, but when these type of rallies into uncharted territory eventually cool off, a new trading range is usually established at higher levels. It’s what long-term bulls want to see.

We cover everything going on across markets and the economy in this week’s Bespoke Report newsletter.

To read this week’s newsletter and gain access to the rest of Bespoke’s daily research, start a 30-day trial to one of our three unique membership levels. CLICK HERE to sign up today!

May 8, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There is nothing new in the world except the history you do not know.” – Harry Truman

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

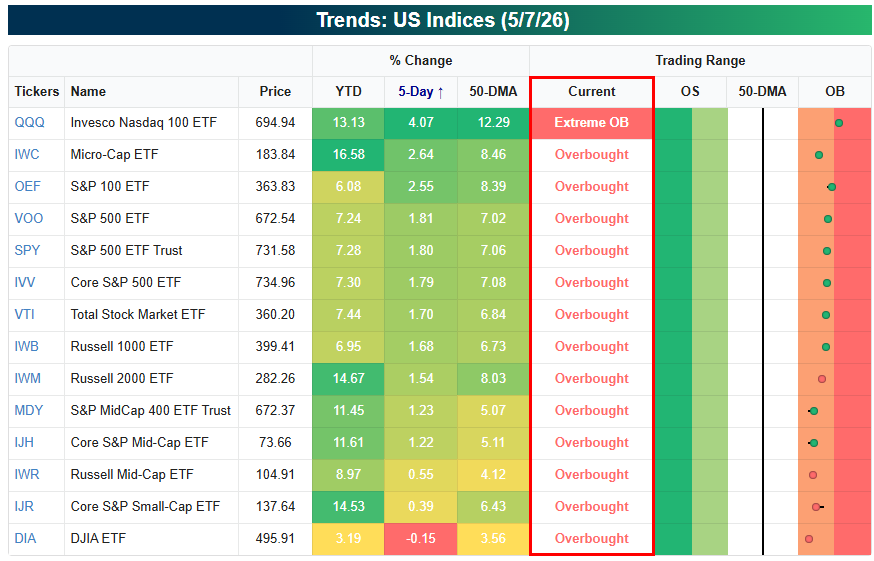

As shown below, we’re entering the last trading day of the week with all of key US index ETFs still in overbought territory:

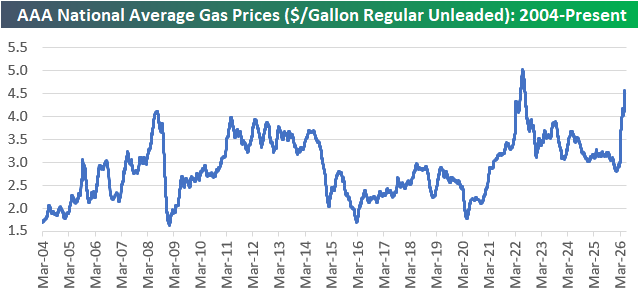

Gas prices continue to spike with the average price for a gallon of regular unleaded up to $4.55/gallon nationally. Ten days ago near the end of April, prices were at $4.17/gallon, so they’ve seen another meaningful pick-up recently.

Just before the Iran War, gas prices had fallen down into the $2s. Now they’re closer to $5/gallon than $4.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 7, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I shall seize Fate by the throat; it shall certainly not bend and crush me completely.” – Beethoven

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Today is the last super-busy day for earnings this season, so we’ll be providing a nice summary of all the results in tomorrow’s Bespoke Report newsletter.

In Monday’s Chart of the Day, we pointed out that Datadog (DDOG) was reporting earnings Thursday morning with a 100% historical EPS and sales beat rate. As a member of the Software group, DDOG took it on the chin from November through March, but it has recovered nicely in the last two months and broken out of its downtrend in the process.

DDOG has historically been a triple play beast, and it delivered once again this morning with another beat on EPS and sales and raised guidance. Shares are up 22% pre-market. The pop highlights that not all “software” stocks are the same, and when names get “thrown out with the bathwater” – the AI Doom trade in this case – opportunities arise.

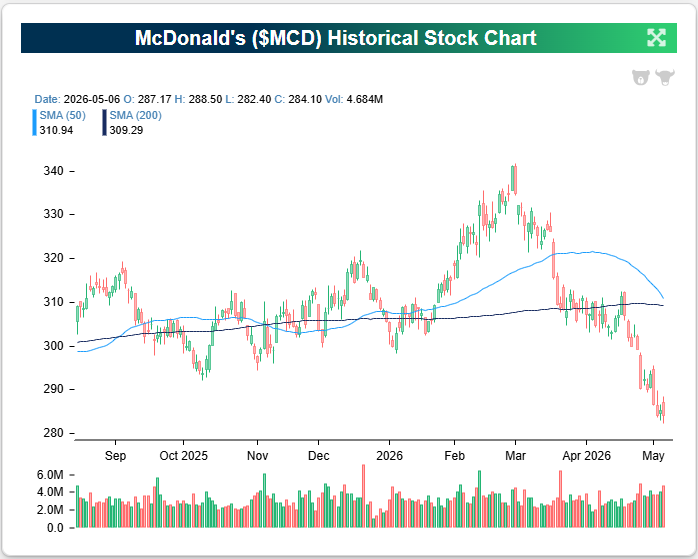

McDonald’s (MCD) is another name that reported this morning, and the company reported a nice EPS beat on roughly inline revenues. Same-store sales growth was up just under 4% in both domestic and international markets.

As shown below, MCD has had a rough run since the Iran War began as investors worried about both consumer demand and higher input costs. This morning’s earnings assuages some of those fears, and shares are up 3% pre-market.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 6, 2026

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

May 6, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Good judgment comes from experience, and a lot of that comes from bad judgment.” – Will Rogers

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US equity futures are up 1% this morning due to more gains from semis and a headline from Axios that the US and Iran are “closing in on a one-page memo to end the war.”

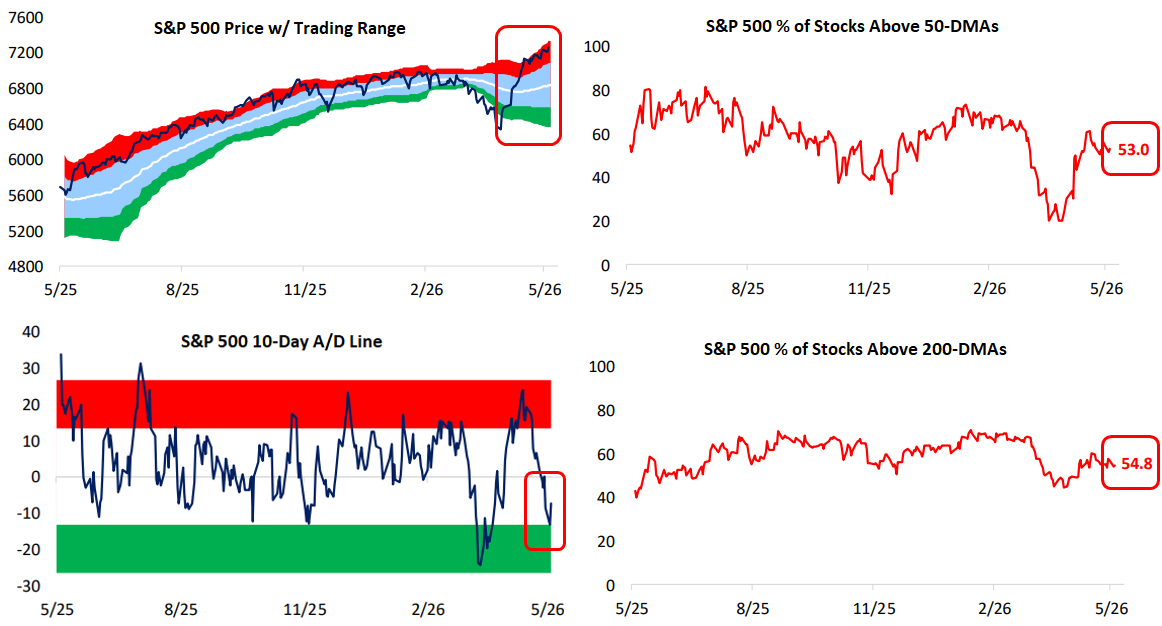

Notably, while the S&P 500’s price is still looking quite overbought, underlying breadth is neutral at best. As shown below, just over 50% of stocks in the S&P are above their 50-DMAs and 200-DMAs, and the S&P’s 10-day advance/decline line is still close to oversold territory.

So while price is extended to the upside, internals suggest that the rally still has room to run before we’d categorize it as overheated in the near term.

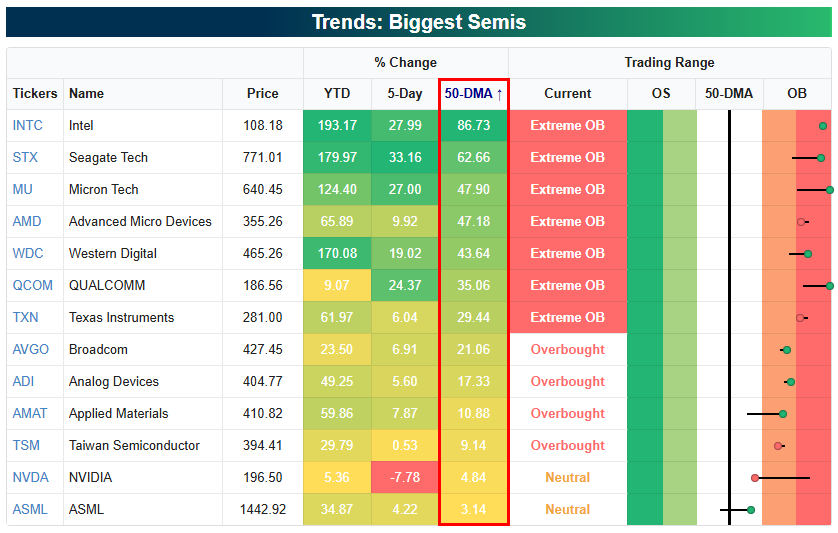

The semis are a different story, however. They’re currently experiencing one of the most epic runs in history, and the group is about as overbought as it gets.

As shown below, stocks like Intel (INTC), Seagate (STX), Micron (MU), and Advanced Micro (AMD) are up anywhere from 10-33% over the last week, and they’re set to open up sharply again this morning. When the opening bell rings, all four of these stocks will be more than 50% above their 50-DMAs.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.