Feb 17, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Builders FirstSource’s (BLDR) Q4 2025 earnings call.

Builders FirstSource (BLDR) is the largest US supplier of building materials and manufactured components to professional homebuilders and remodelers, operating over 550 locations nationwide. The company offers everything from lumber and windows to prefabricated trusses, wall panels, and installed services, making it a barometer for single-family and multi-family housing activity, construction labor dynamics, and building product pricing. Q4 was weaker than expected as large builders aggressively pulled back starts late in the year to burn through excess housing inventory, driving a 12% sales decline and 44% adjusted EBITDA drop. Gross margins held at 29.8%, above the pre-transformation 27% level of 2019, but management guided a wide 28.5%–30% range for 2026, given early-year contract resets and volume uncertainty. BLDR is leaning into a $100 million SG&A cost-action plan, has consolidated 55 facilities over two years, and acquired Pleasant Valley Homes to experiment with factory-built modular housing as an affordability solution. The 2026 outlook assumes flat starts with a back-half-weighted recovery driven by easier comps. BLDR shares opened 1% lower on 2/17, but touched positive territory around noon after reporting EPS and revenue misses…

Continue reading our Conference Call Recap for BLDR by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Feb 17, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I’ve missed more than 9000 shots in my career. I’ve lost almost 300 games. 26 times, I’ve been trusted to take the game-winning shot and missed. I’ve failed over and over and over again in my life. And that is why I succeed.” – Michael Jordan

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It may be Tuesday morning, but futures are in a Monday mood as the S&P 500 is indicated to open down by 0.40% while the Nasdaq is down double that. The main culprit is the software sector as iShares Expanded Tech Software ETF (IGV) is down 1% in the pre-market, continuing a trend that has been in place for weeks now.

Treasury yields are also lower as the 10-year trades below 4.03%. Will we see a 3-handle this week? While yields are lower, crude oil prices are rallying over 1% to nearly $64 per barrel as President Trump made comments over the weekend that regime change “would be the best thing that could happen” in Iran. Despite the higher oil prices on geo-political concerns, though, gold prices are down 2% and back below $5,000, while silver is down over 4%. Along with lower metals prices, Bitcoin and other crypto assets are also down about 1%.

It was a quiet session in Asia as most markets are closed for the Lunar New Year. Japan was open for trading, though, but with a drop of 0.4% in the Nikkei, maybe it should have stayed closed too!

In Europe, it’s been a more positive tone as the STOXX 600 is up fractionally, led by larger gains in Italy and Spain. Economic sentiment, as measured by ZEW, was significantly weaker than expected, which perhaps makes the odds of rate cuts more likely.

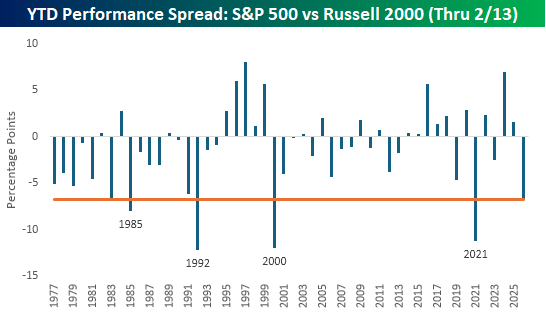

The S&P 500 went into the holiday weekend with a modest decline of 0.14% on a YTD basis, but the small-cap Russell 2000’s performance looks entirely different, as that index has already gained 6.64%. With 6.8 percentage points separating the two indices, small caps are off to their best start relative to large caps since 2021 and the fifth-best start to a year in the index’s history. The only other years besides 2021 when small caps got off to a better start were in 2000, 1992, and 1985.

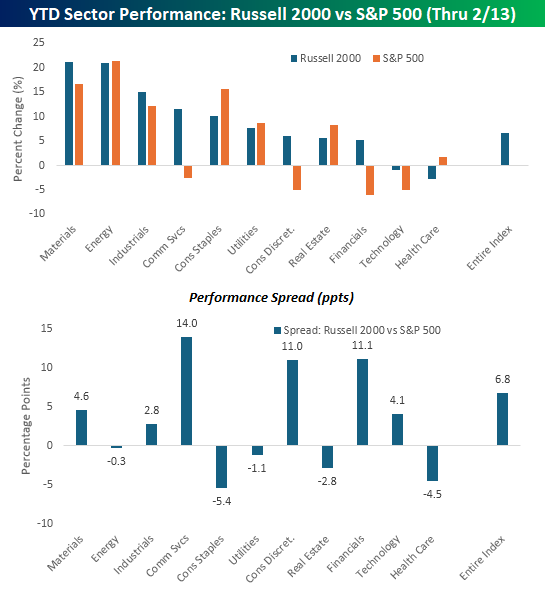

For most sectors, the performance disparity between small and large-cap stocks has been narrower. The top chart below shows the YTD performance (through 2/13) of each sector in both the Russell 2000 and the S&P 500, and the lower chart shows the performance spread between the two. As shown, the only three sectors where the performance disparity is wider than it is at the index level are in Communication Services, Consumer Discretionary, and Financials, and in all three cases, the disparity is, like it is at the index level, in favor of small caps.

Looking in the other direction, there are actually five sectors where large caps are outperforming their small-cap peers. The widest disparities in favor of large caps are in Consumer Staples and Health Care, but large-cap Real Estate, Utilities, and Energy are also outperforming.

Feb 13, 2026

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Feb 13, 2026

The “AI Boom to AI Doom” shift has happened: Software stocks have collapsed 25%+ while defensive sectors rocket higher in a rotation that’s never happened this fast—get the full 38-page analysis now. Read this week’s Bespoke Report newsletter and gain access to the rest of our product suite with a Bespoke trial. CLICK HERE or on the image below to proceed.

Feb 13, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Volatility obscures the future but does not necessarily determine the future.” – Peter Bernstein

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After yesterday’s sharp declines, bulls were in no rush to get back to work this morning ahead of the January CPI report, with futures on the major indices all down about 0.20%. The 10-year yield was basically unchanged at 4.10%, down from 4.23% earlier in the week. Crude oil was also modestly lower, while gold is marginally higher and silver rallies close to 3%. Bitcoin is up a little over 2% but still below $67K.

In Asia, equities were lower across the board with the Nikkei down 1.2%, Hong Kong down 1.7%, and China’s Shanghai Composite falling 1.3%. Despite those losses, Japan still finished the week 5% higher, while South Korea rallied more than 8%!

In Europe, equities were mostly lower but by more modest amounts. The STOXX 600 is down 0.4%, putting it in the red for the week, while Germany bucks the trend with a gain of 0.1%. Q4 GDP for the continent grew 0.3%, which was right in line with expectations.

CPI just hit the tape, and the market liked it! Headline CPI came in weaker than expected, with the y/y reading was 2.4% compared to forecasts for 2.5%. Core CPI was right inline with forecasts at 0.3% m/m. In reaction, futures have bounced into positive territory, while the 10-year yield dropped to 4.07%. Is a 3-handle on the way?

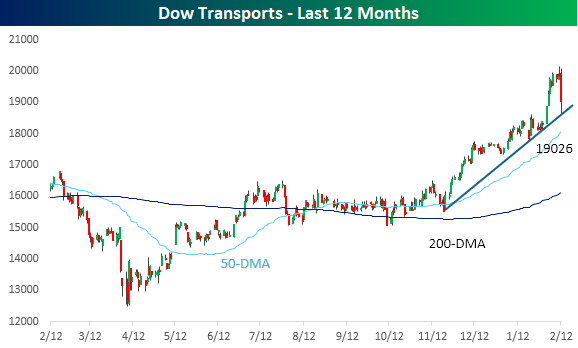

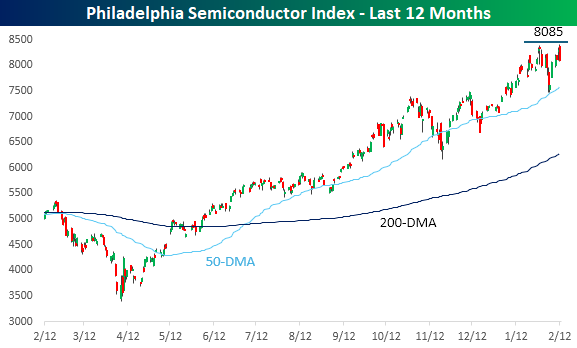

It was a rough day for two very important sectors often considered leading indicators of the physical and digital economy, as the Dow Transports fell 2.5% while the Philadelphia Semiconductor index (SOX) plunged just over 4%. That’s enough to instill some fear in the minds of already nervous investors.

Starting with the Transports, yesterday’s pullback found support right at the index’s uptrend line that has been in place since late last year. Looking at the chart, even bulls have to admit that as painful as yesterday’s sell-off was, the surge in the prior couple of weeks had also gotten ahead of itself.

Moving on to the transports of the digital economy, the SOX has been on a tear for nearly a year now, and even after yesterday’s decline, it has more than doubled off its April lows. Doubled! That being said, yesterday’s decline came right after the index had come up just shy of taking out its prior high from January, so until that resistance is taken out, the burden of proof is on the bulls.

Feb 12, 2026

Log-in here if you’re a member with access to the Closer.

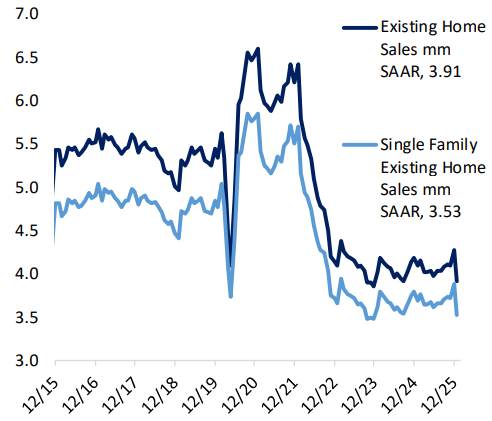

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin by showing the next pain points as a result of AI (page 1) followed by a dive into the strong showing by long bonds at auction this afternoon (page 2). After recapping claims (page 3) we then turn to an overview of the reversal in January home sales data (page 4). We cap off tonight’s report with earnings reviews (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!