Feb 24, 2017

When it comes to rankings, a “ten” is typically considered as good as it gets. In many sports, a “ten” is considered the best possible score. In 1976, Nadia Comaneci was the first gymnast to ever score a perfect ten when she was flawless on the uneven bars. Then, in 1979, Bo Derek also taught us that a ten was perfect.

In 1984, the “perfect ten” was one-upped when ‘guitarist’ Nigel Tufnel from Spinal Tap introduced the world to amps that had a volume control that topped out at eleven. His reasoning was that every once in awhile there are those times where you have the volume up to ten and everything is going great but there is nowhere else to go from there. To solve the problem Tufnel tells the interviewer (played by Rob Reiner) that his amps go to eleven for those times when the band needs the “extra push off the cliff.”

In 1984, the “perfect ten” was one-upped when ‘guitarist’ Nigel Tufnel from Spinal Tap introduced the world to amps that had a volume control that topped out at eleven. His reasoning was that every once in awhile there are those times where you have the volume up to ten and everything is going great but there is nowhere else to go from there. To solve the problem Tufnel tells the interviewer (played by Rob Reiner) that his amps go to eleven for those times when the band needs the “extra push off the cliff.”

This week, the DJIA was more than perfect, and like the amps from Spinal Tap, it pulled an eleven. And it did so in dramatic fashion, as the only time that the DJIA traded in positive territory was in the final seconds of the trading day. So where do we go from here?

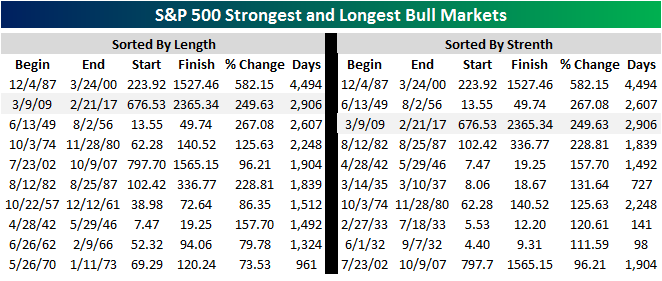

Along with the DJIA this week, all of the major averages hit new bull market and all-time highs, as one of the most unloved bull markets of all time continues to chug along. For the S&P 500, the current bull ranks as the second longest and third strongest of all time. While it will be some time before the current bull makes a run for the top spot in either category, in strength terms, a gain of 5% from here will put the current bull into second all-time as well.

Our just-published Bespoke Report newsletter (included weekly with all of our membership packages) includes a recap of the markets this week as well as what to expect going forward based on the events of the last week. If you’d like to read our thoughts in this week’s Bespoke Report newsletter, take advantage of our one-month Bespoke Premium free trial offer. Sign up now at this page.

Have a great weekend!

Feb 17, 2017

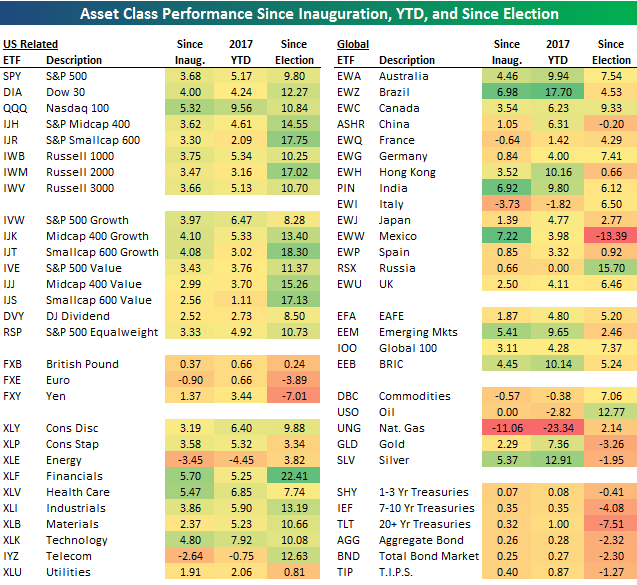

The screen below is one of many graphics included in our just-published Bespoke Report newsletter (included weekly with all of our membership packages). It shows the recent performance of various asset classes using our key ETF matrix. Note that the Mexico ETF (EWW) is up more than any ETF in the entire matrix since Trump’s Inauguration on January 20th!

If you’d like to read our thoughts on recent performance plus the rest of this week’s Bespoke Report newsletter, take advantage of our one-month Bespoke Premium free trial offer that includes our 2017 Outlook Report. Sign up now at this page.

Have a great weekend!

Feb 10, 2017

And you thought politics was crazy! After record high temperatures in the Northeast on Wednesday, Thursday brought a freak snowstorm that dumped more than a foot of snow in the tri-state area, grounding pretty much everything to a halt. After digging out the summer clothes Wednesday, shovels were the order of the day on Thursday. Through the weather and everything else, though, the stock market continued to serve as a rock of stability, steadily rising in what was a relatively uneventful week in terms of the market. After a small decline to start the week, the S&P 500 saw four straight days of gains for its longest winning streak of the year.

In our Bespoke Report a few weeks back, we highlighted the S&P 500’s stair-step pattern of the last year and how the recent pattern looked to be in the middle stages of completing the tread of a stair. With each day that the sideways pattern went on, an increasing number of pundits were busy writing off the so-called Trump rally. It only seems fitting that just when doubts over the sustainability of the rally reached their highest levels since the election, the S&P 500 broke out of its recent range to new all-time highs and forming a new riser in the stair step pattern. Wherever the rally stops, nobody knows, but when it ends it will be at precisely the point when everyone who called an end to the rally decides that the rally “now has legs.”

If you’d like to read our thoughts on recent performance plus the rest of this week’s Bespoke Report newsletter, take advantage of our one-month Bespoke Premium free trial offer. Sign up now at this page.

Have a great weekend!

Feb 3, 2017

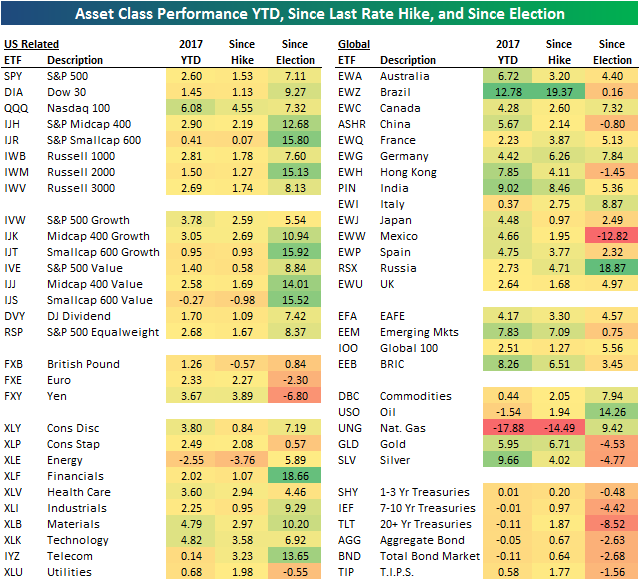

The screen below is one of many graphics included in our just-published Bespoke Report newsletter (included weekly with all of our membership packages). It shows the recent performance of various asset classes using our key ETF matrix.

If you’d like to read our thoughts on recent performance plus the rest of this week’s Bespoke Report newsletter, take advantage of our one-month Bespoke Premium free trial offer that includes our 2017 Outlook Report. Sign up now at this page.

Have a great weekend!

Jan 27, 2017

If you’re not yet a Bespoke subscriber, you can still get Bespoke’s 2017 Outlook Report with a 30-day free trial to Bespoke’s premium research! Click here to learn more.

The screen below is one of many graphics included in our just-published Bespoke Report newsletter (included weekly with all of our membership packages). As shown, we closed out the final full week of January with nearly all country ETFs trading above their 50-day moving averages. All but 7 of the 30 country ETFs in the screen are overbought. The post-election rally continues.

If you’d like to see the rest of this week’s Bespoke Report newsletter, take advantage of our one-month Bespoke Premium free trial offer that includes our 2017 Outlook Report. Sign up now at this page.

Have a great weekend!

Jan 20, 2017

If you’re not yet a Bespoke subscriber, you can still get Bespoke’s 2017 Outlook Report with a 30-day free trial to Bespoke’s premium research! Click here to learn more.

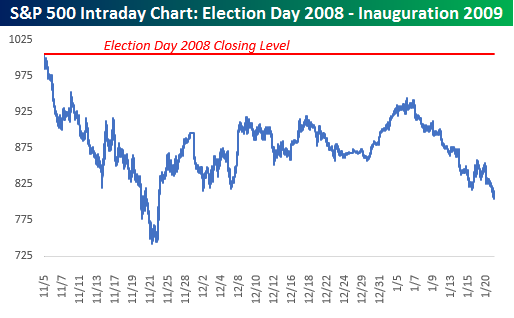

Eight years ago today, the presidency of what many called the most anti-business and anti-market candidate ever elected to the country’s highest office began. At the time of President Obama’s inauguration, for many, today couldn’t come soon enough. The consensus was that once his four years in office were done (because how could he ever be elected to a second term), the overall sentiment would be “good riddance.” As the saying goes, though, that’s why the play the game, because even when you think you have it all figured out, the outcome often looks different than what many expect.

Right out of the gate after the 2008 election, stocks reacted negatively. On the day after Obama’s election in 2008, the S&P 500 declined over 5%, and it kept going down from there. At the intraday low in November, the S&P 500 lost more than a quarter of its value, in what was one of the steepest sell-offs in reaction to a Presidential election in market history. The market recovered a bit from there, but remained extremely volatile throughout the transition, but at the end of the day on his inauguration, the S&P 500 was still down 20% since he was elected. We would be remiss not to mention the fact that the US economy was in the middle of a Financial Crisis during this period so that was a big contributor to the market weakness, but the general perception from the markets was still that Obama would be bad for stocks.

Right out of the gate after the 2008 election, stocks reacted negatively. On the day after Obama’s election in 2008, the S&P 500 declined over 5%, and it kept going down from there. At the intraday low in November, the S&P 500 lost more than a quarter of its value, in what was one of the steepest sell-offs in reaction to a Presidential election in market history. The market recovered a bit from there, but remained extremely volatile throughout the transition, but at the end of the day on his inauguration, the S&P 500 was still down 20% since he was elected. We would be remiss not to mention the fact that the US economy was in the middle of a Financial Crisis during this period so that was a big contributor to the market weakness, but the general perception from the markets was still that Obama would be bad for stocks.

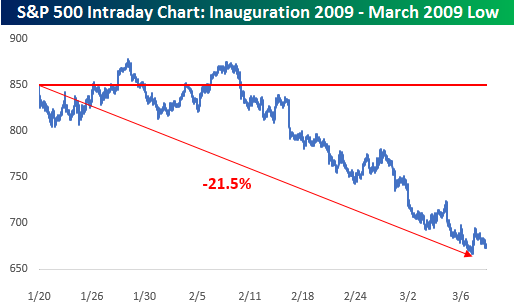

If Obama was hoping for a honeymoon once he came into office, he didn’t get it. While the first couple of weeks of his Presidency saw sideways trading, the bottom fell out of the market again in early February, falling over 21% through early March. At this point, investors were wondering how many bottoms there were to fall out of, while President Obama was probably watching the headlines pile up and wondering what he had gotten himself into!

If Obama was hoping for a honeymoon once he came into office, he didn’t get it. While the first couple of weeks of his Presidency saw sideways trading, the bottom fell out of the market again in early February, falling over 21% through early March. At this point, investors were wondering how many bottoms there were to fall out of, while President Obama was probably watching the headlines pile up and wondering what he had gotten himself into!

If you’d like to see the rest of this week’s Bespoke Report newsletter, take advantage of our one-month Bespoke Premium free trial offer that includes our 2017 Outlook Report. Sign up now at this page.

Have a great weekend!