Jun 7, 2019

This week’s Bespoke Report newsletter is now available for members. Equity markets surged despite short term interest rate markets pricing near-certainty of multiple Fed rate cuts this year. How can an economy so bad that the Fed needs to cut mean stocks go up? We take a look around for some answers. We also review just how dovish the Fed has been relative to what markets have been pricing of late. While the domestic economy has definitely slowed down from the torrid pace of 2018, even the disappointing nonfarm payrolls number today paints a different picture than assumptions of multiple cuts from the front end. The global economy is less constructive, but there’s a difference between weakness and a recession panic, as we show. Finally, we present an argument for why Fed rate cuts may not be necessary for the economy to stabilize and start to pick up again thanks to negative feedback loops.

We cover everything you need to know as an investor in this week’s Bespoke Report newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

May 31, 2019

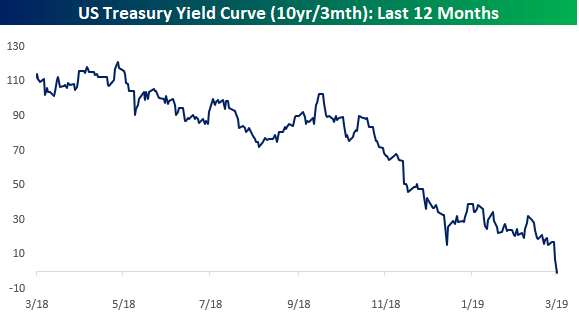

This week’s Bespoke Report newsletter is now available for members. In this week’s report, we cover the good, the bad, and the downright ugly when it comes to the action for equity markets lately. There’s plenty of ugly to go around like the yield curve and the technical backdrop, but there’s also some good that you may be surprised to see.

We cover everything you need to know as an investor in our weekly newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

May 24, 2019

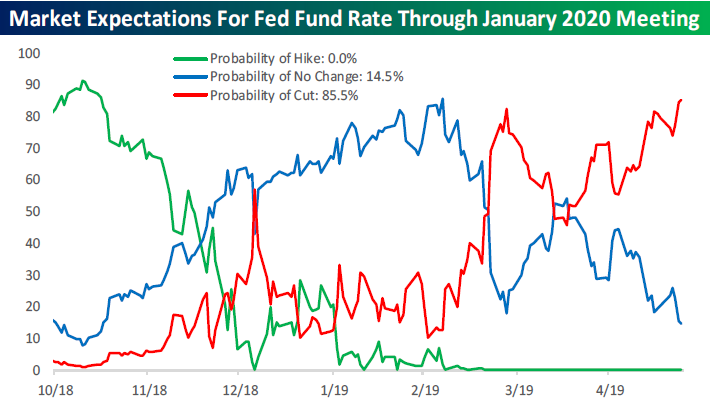

Hut, Hut, Cut! With weaker economic data to contend with this week on both a domestic and international basis, plus escalating tensions between the US and China, investors are increasingly pricing in a higher likelihood of rate cuts from the FOMC before the year is out. Through mid-day Friday, the Fed Fund futures market was pricing in over an 85% chance of a rate cut between now and the January 2020 meeting. Those are the kind of odds that would make James Holzhauer say “All in.”

This week’s Bespoke Report newsletter is now available for members. In this week’s report, we cover all the bases including the massive declines in semis, one of the shallowest five-week losing streaks for the DJIA on record, the shift to defensives, the disconnect between the market and the Fed, the widening gap between Internationals and Domestics, summer seasonality, sentiment updates, what the S&P 500’s flat 200-DMA means for equities, big gaps down on a daily basis, and more.

We cover everything you need to know as an investor in our weekly newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

May 17, 2019

This week’s Bespoke Report newsletter is now available for members. Stocks started the week poorly but found excuses to rally midweek, just not enough to get all the way up to breakeven since last Friday. Global economic data continued to look mostly soggy, though not across the board. There was a lot of US data this week, but also important releases from China, Japan, and the Eurozone that we discuss in detail. We also take a look at recent earnings in Europe which have exceeded expectations modestly.

One piece of positive economic data we focus on in the week’s report is the ratio of Leading to Coincident indicators published each month by the Conference Board. As shown below, the ratio is rising again after bottoming out in January. While not at a new high, its behavior is looking distinctly different from the typical pre-recession backdrop. Ahead of recessions, the ratio plunges very consistently, a marked difference to the current sideways range. We discuss further in this week’s full report.

We cover everything you need to know as an investor in this week’s Bespoke Report newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

May 10, 2019

The S&P 500 was down this week, but we were very happy with the action late in the trading day on Thursday and Friday. Buyers willingly stepped in after European markets closed on both days to end the week. We highlight this action in multiple charts in this week’s Bespoke Report, which you can access when you start a two-week free trial to one of our three membership levels. You won’t be disappointed!

May 3, 2019

In the market’s ceaseless determination to make a mountain out of every molehill, equities sold off sharply from record highs on Wednesday afternoon after Fed Chair Powell suggested that the FOMC had no plans to cut interest rates as futures markets were implying. Didn’t he have some nerve?

In the last month, Jobless Claims hit a 50-year low, Q1 GDP surprised to the upside and came in at 3.2%, the stock market was at record highs, and on Friday, Non-Farm Payrolls surprised to the upside with a reading of 263K. Are there some blemishes on the landscape? Do things always look brightest at the peak? Sure, but to say the Fed must cut rates in this environment was a bit much. By the end of the week, cooler heads prevailed, and the S&P 500 finished the week less than 20 cents off its record closing high and less than ten points below its intraday record high.

Even more encouraging was the rally in the small-cap Russell 2000, which finally broke above resistance to close at its highest level since October. Traders often look to small caps for confirmation of a rally, and while we think they are often given more importance than they deserve, their outperformance this week doesn’t hurt.

We have a lot more to cover this week, including updates on some of the key leadership groups/indicators, drivers of the market’s strength in April, how earnings season is progressing so far, how the economy is faring, and the state of consumer sentiment, among other things. To read our full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!