Jul 26, 2019

This week we’re outlining how we see the global economy at present, along with its influence on US interest rates, credit, commodities, and equity markets. One of the topics we discuss in detail is the strong performance of US GDP in Q2, which in addition to upward revisions from 2014-2018 also showed newly-reported Q2 growth that was far stronger than analyst estimates. Smaller-than-expected headwinds from trade and inventory and a massive surge in consumer spending helped push growth above expectations despite weak investment. With the Fed set to join the global central bank easing party at its July meeting, it’s part of the reason to expect that the global backdrop is set to improve. Read more after signing up for a free trial below!

We cover everything you need to know as an investor in this week’s Bespoke Report newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Jul 19, 2019

This week’s Bespoke Report newsletter is now available for members.

In this week’s newsletter, we try and digest market expectations for rate cuts amid strengthening economic data. We also provide a full rundown of this week’s earnings reports and what’s on tap for next week. Three of the four FANG stocks (FB, AMZN, GOOGL) report next week. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Jul 12, 2019

This week’s Bespoke Report newsletter is now available for members.

With little in the way of major economic data and earnings season still a week away, the only major item of this past week was the deluge of Fed officials hitting the tape, including Chairman Powell’s testimony to the House and Senate on Wednesday and Thursday.

With the overall calm and Powell’s soothing words, bulls were in charge and took charge sending the major US large-cap indices to record highs. After numerous attempts to get through the 2,950 level, the S&P 500 finally broke out and hasn’t looked back since. With the S&P 500 up 20% on the year and earnings season coming up on the horizon where does the market stand and have we moved too far to fast?

In this week’s report, we’ll try to shed some light on that question by looking at the recent moves from a variety of angles including market internals, the setup for earnings season, how the economy is faring, and a look at sentiment and prior strong rallies. We cover everything you need to know as an investor in our weekly newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Jun 28, 2019

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition as we close out the first half of 2019.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking!

On page three of the report, you’ll see a full list of the pros and cons that we lay out. Page two includes our popular decile analysis for the first half of the year.

To read this report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Jun 21, 2019

This week’s Bespoke Report newsletter is now available for members. In this week’s report, we cover the Fed’s dovish tilt that was met with new all-time highs for the stock market.

We cover everything you need to know as an investor in our weekly newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Jun 14, 2019

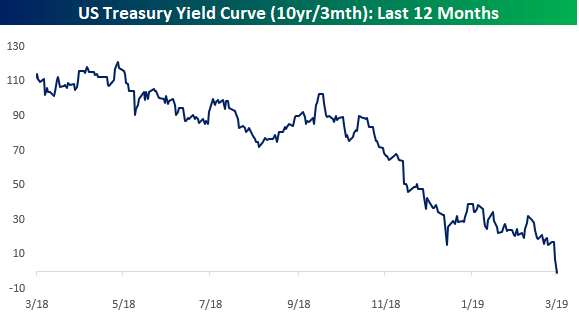

We’ve just published our weekly Bespoke Report newsletter, which covers all of the topics you need to be aware of as an investor. After a sharp bounce off the lows on 6/3, the S&P 500 stopped to refuel this week as it readies itself for some key events in the coming weeks that will likely help to steer the market’s direction into the end of the second quarter. The first of those events (barring any surprising tweets from the President) is next week’s FOMC meeting where Jay Powell will be forced to reconcile the differences between what members of his committee have been saying and what the market is expecting for the July meeting.

On the one hand, economic data doesn’t seem anywhere close to warranting a cut in rates, but economic data is obviously backward looking. Members of the FOMC will be forced to weigh the data with other factors like the message of the yield curve, falling inflation, and even more importantly, plummeting inflation expectations. In addition to those factors, Fed officials must also weigh what’s going on with trade. For starters, can rate cuts even do anything to offset the potential drag that comes from tariffs and a potential trade war? In addition to that, a lot of the trade tensions can easily be undone just as easily as they were put into place. What happens if the FOMC cuts rates and trade issues are worked out shortly thereafter? Confused? Just be thankful you don’t have to make the decisions!

To read our full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!