Feb 22, 2019

Markets continue to rally as equity investors take an optimistic view of earnings results and look past weakening global economic data. Here in the US, along with a relatively solid earnings season, the Federal Reserve has stepped its foot off the brakes. Oil prices are rallying, despite very robust US production numbers, and other industrial commodities are getting in on the same game. Abroad, Chinese stocks have led the way higher even as data in a range of global economies has deteriorated.

Along with in-depth earnings season coverage, we review what’s been happening in markets around the world from equities to commodities to credit. We cover everything you need to know as an investor in this week’s Bespoke Report newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Feb 15, 2019

The big headline around financial circles this week was the fact that after facing resistance from a minority of politicians and public figures, Amazon decided to pull the plug on its planned expansion into New York City. Whatever your individual views towards the deal, the fact is that most people in the New York City area and Long Island City, where the project was to be based, were in favor of the expansion plan. In that regard, Amazon’s decision to pull out was viewed as a negative for the city and sets a bad precedent for the future when other firms weigh expansions in the region.

It’s always disheartening when a project runs into resistance and fails to clear the finish line, so thankfully for bulls, the market didn’t pull an Amazon and pack up and quit when it too faced resistance heading into the week. While Small and Mid Caps were finally able to take out one of the prior highs from before the December swoon (red arrows), the S&P 500 and Nasdaq haven’t quite been able to clear that hurdle. In the case of the S&P 500, though, the 200-DMA is now in the rearview mirror, so it’s a start.

We had lots to talk about in this week’s Bespoke report, so if you don’t have access yet, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Feb 8, 2019

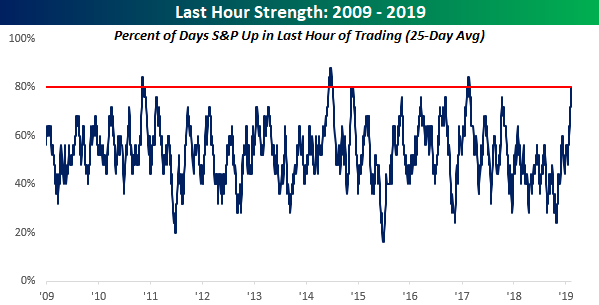

The S&P 500 finished the week with a slight gain after posting positive returns early in the week and declines late in the week. Friday saw declines early in the day, but investors really stepped up their buying in the afternoon to fully erase what had been a pretty sizable decline. Friday’s late-day strength was a microcosm of the intraday buying trend we’ve seen all year.

As shown in the chart below, the S&P 500 has rallied in the last hour of trading on 80% of trading days over the last five weeks going back to the start of 2019. Readings of 80% or higher have been rare over the last 10 years dating back to the start of the bull market in 2009.

We analyze the importance of late-day strength in this week’s Bespoke Report newsletter. We also cover a number of other technical, fundamental, and sentiment measures in this week’s report. To read the Bespoke Report and also gain access to our full suite of investor tools, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Feb 1, 2019

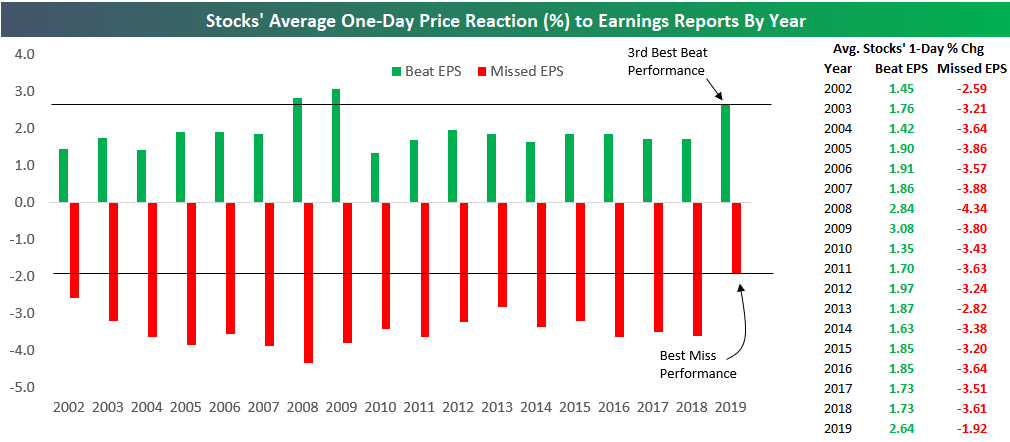

The S&P 500 gained 1.6% this week as stocks reporting earnings continued to get bid higher. Based on stock performance this earnings season, investors got way too bearish leading up to the start of the Q4 reporting period in early January. With reports not coming in as bad as expected, there has been a rush to buy stocks that beat estimates. At the same time, stocks that have missed estimates have not been getting hit that hard. So far this year, stocks that have beaten EPS estimates have gained 2.64% on their earnings reaction days, while stocks that have missed EPS estimates have only fallen 1.92%. Normally, stocks that beat EPS only gain 1.9% on their earnings reaction day, while stocks that miss EPS normally fall ~3.5%. This year has been a huge outlier so far, but eventually we’ll see mean reversion back towards the long-term averages. Enjoy the earnings strength while it lasts!

Along with in-depth earnings season coverage, there’s a lot more to discuss this week after the Fed’s rate decision on Wednesday and Friday’s blockbuster non-farm payrolls number. We cover everything you need to know as an investor in this week’s Bespoke Report newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed! Have a great Super Bowl weekend.

Jan 25, 2019

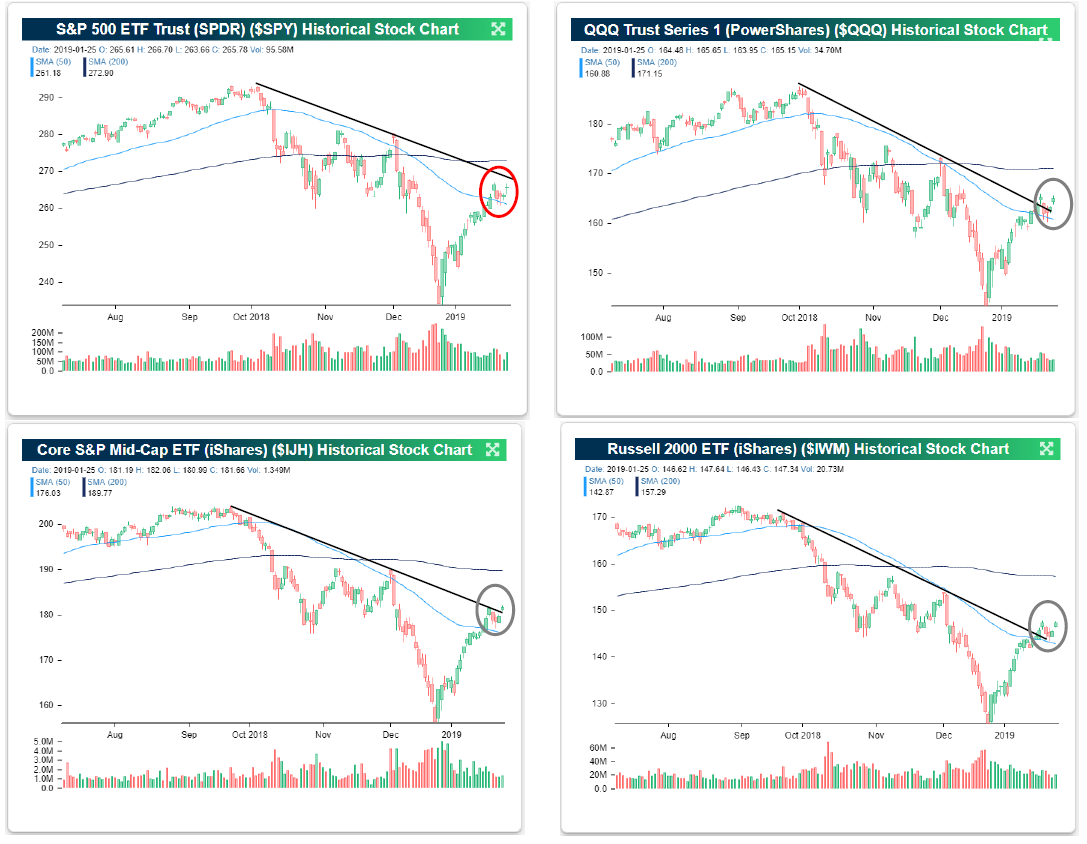

US equities took a bit of a breather this week from their torrid rally off the Christmas Eve lows. While anyone long equities would like to see the market trade consistently higher, nothing moves in a straight line. At this point, the sideways trading this week can still be considered nothing more than a pause as the market looks to catch its breath. Next week, though, we should get a lot more clarity on which way this market wants to move as the FOMC will announce its latest views on monetary policy Wednesday, followed by a Jerome Powell Press conference. Just as important, the pace of earnings reports for Q4 will pick up even more steam as nearly a quarter of the S&P 500 (122 companies) will report numbers.

Looking at where some of the major US averages closed out the week, one of these pictures doesn’t look like the others. As shown in the four charts below, in this week’s trading, the Nasdaq 100, the S&P 400 Mid Cap Index, and the Russell 2000 all appear to have broken their downtrends from the October highs. The lone holdout at this point is the S&P 500, which finished the week just shy. Breadth for the S&P 500 has been very strong lately (page 30), so now all we need is price to confirm it. Something tells us that next week we’ll have a good idea either way!

For in-depth analysis of recent price action, sector technicals, earnings season, the economy, and more, start a two-week free trial to one of our three membership levels and read this week’s Bespoke Report newsletter. You won’t be disappointed!

Jan 18, 2019

2019 continues to track the complete opposite of what we saw in Q4 2018, with the hardest hit areas during Q4 bouncing the most off of their lows this year. Smallcaps are leading the way with gains of nearly 10% on the year, while Energy (XLE) leads all sectors at +11.32% on the back of oil’s (USO) 17% surge. Brazil (EWZ) leads all countries in our ETF matrix with a YTD gain of 13%, which is a rare continuation of what we saw for Brazil to end 2018. Canada (EWC) is also posting a solid showing in 2019 with a double-digit percentage gain already. The only areas of weakness are India (PIN), precious metals, and Treasuries.

For in-depth analysis of recent price action, sector technicals, earnings season, the economy, and more, start a two-week free trial to one of our three membership levels and read this week’s Bespoke Report newsletter. You won’t be disappointed!