Jul 9, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A great wind is blowing, and that gives you either imagination or a headache.” – Catherine the Great

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Looking at the quote above from Catherine the Great, isn’t that just the way you feel when it comes to AI? While the possibilities are endless, the pace of change and trying to keep on top of everything going on can be exhausting!

The S&P 500 has declined for two straight sessions, but futures are looking modestly higher this morning on little in the way of news. Investors will continue to monitor Washington for any tariff-related headlines, but the letters and policies released and announced this week have, broadly speaking, had little impact. It’s another quiet day for data as there are no economic reports on the calendar, but minutes from the last FOMC meeting will be released at 2 PM.

Speaking of the FOMC, the Wall Street Journal is reporting this morning that the President is currently leaning towards Kevin Hassett over Kevin Warsh to replace Fed Chair Powell. Warsh is reportedly falling out of favor for some of his past criticism of the Fed’s zero-interest rate policy and asset purchase programs.

In international markets, Asian stocks were mostly lower overnight following Trump’s comments that he wouldn’t extend his August 1st tariff deadline. The only major index to buck the negative trend was Japan, where the Nikkei rallied 0.33%. In Europe, the tone is much more positive with the STOXX 600 up over 0.7% as defense stocks lead the charge.

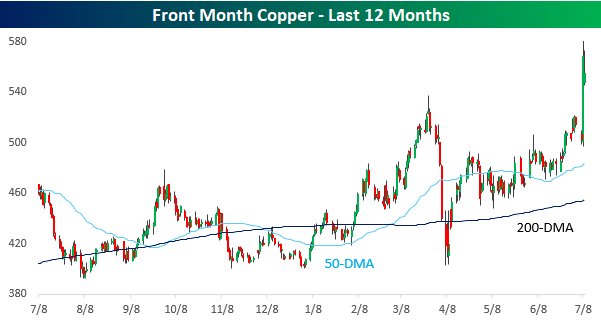

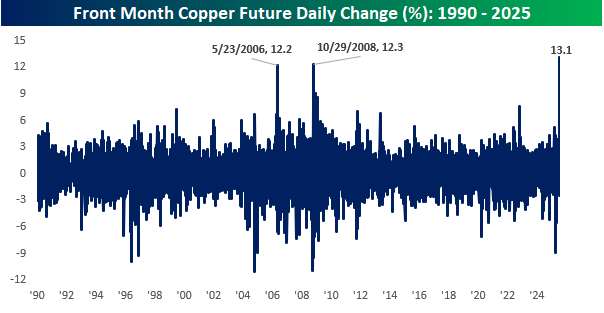

As mentioned above, the President’s various tariff policies announced this week haven’t had much impact on a macro basis, but for certain areas like copper, the impacts have been significant. After the year has already seen incredible rallies in the price of gold, platinum, and silver, yesterday, President Trump gave copper the boost it needed when he announced 50% tariffs on all copper imports. The news came just as copper was starting to pull back last week after testing its highs from earlier in the year. That resistance proved no match for the 50% tariff bazooka, and prices broke out to a record high, eclipsing $5.40 per pound, finishing up more than 13% on the day. Strength in copper is often considered a sign of economic strength, but we’re not sure a rally artificially propelled by trade policy would qualify.

Yesterday’s 13.1% rally in copper was a record one-day gain for the commodity, eclipsing the prior record of 12.3% from October 2008. Since 1990, it was also only the third time the commodity rallied more than 10% in a single day.

Jul 8, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If your only goal is to become rich, you will never achieve it.” – John D. Rockefeller

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Subdued is the tone once again this morning as equity futures are little changed on either side of the unchanged line. Nasdaq futures are showing the biggest move with a gain of 0.25%. Crude oil is fractionally lower, just below $68 per barrel, while the 10-year yield is up 2 bp,s taking the yield back above 4.4%. Gold is slightly lower, while Bitcoin and Ethereum both are trading up about 1%.

In Asia overnight, most major indices were little changed, except for China, which was up 0.70% while Hong Kong’s Hang Seng was up just over 1%. The modest gains came even as President Trump sent letters to many countries in the region, including Japan and South Korea, informing them that their exports to the US would face tariffs of at least 25%.

European stocks are little changed in the early going this morning, with the STOXX 600 up 0.10% while Germany and the UK are up fractionally, while France is lower. The EU was one region of the world not to receive a letter on tariffs, and that has raised hopes that a deal with the bloc could be near. Reports this morning suggest that the base rate will be 10% with some exceptions for aircraft and parts, medical equipment, and spirits.

Today in the US, it’s another quiet day on the calendar. NFIB Small Business Optimism came in right in line with expectations at 98.6, which was down very slightly from last month’s reading of 98.8. The only other report on the calendar is the New York Fed’s Survey of Consumer Expectations, where 1-year inflation expectations are expected to come in at 3.2%.

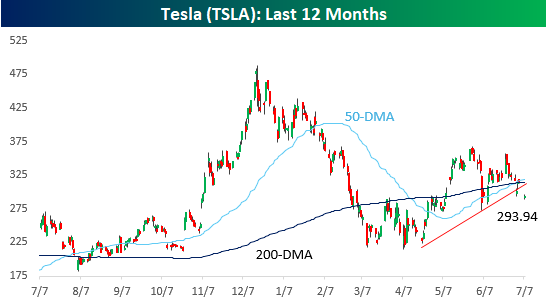

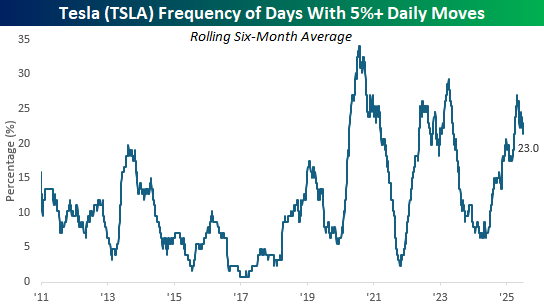

With Elon Musk announcing the creation of the America Party over the weekend and the potential of a third party to hurt Republican majorities in the mid-term elections, investors headed into the new week with concerns that potential retribution from President Trump would hurt Tesla’s business. In response, the stock opened down over 6% yesterday and basically stayed there, finishing the day with a decline of nearly 7%.

Yesterday’s decline broke TSLA’s uptrend off the April lows, and that came after making a lower high in late June. All this came after the stock made a golden cross (50-day moving average cross above the 200-day moving average as both are rising) last week, which technicians consider a positive technical formation. Fitting for a stock like TSLA, the stock’s trading pattern has been sending mixed signals.

Normally, as companies become larger in terms of market cap, their share prices become less volatile, but that’s not the case with TSLA. Yesterday was the 29th daily gain or loss of 5%+ in TSLA over the last six months, which works out to 23% of all trading days. While the company went public in 2010, it wasn’t until 2020 that TSLA routinely started to see 5%+ daily moves on 20% or more of trading days over a rolling six-month period.

Jul 7, 2025

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!

Jul 7, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“History is a guide to navigation in perilous times. History is who we are and why we are the way we are.” – David McCullough

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Investors are being eased back into the market this morning, with futures showing modest losses after a more significant decline overnight. The market may be open, but with no economic or earnings reports on the calendar, things are relatively quiet to kick off the new week. That’s generally the case for the rest of the week too, with very few reports on the calendar in the next four trading days. That will leave plenty of time for investors to focus on trade, and Treasury Secretary Scott Bessent says to expect several announcements in the next two days, and for those that don’t make a deal by August 1st, tariffs on their exports to the US will go back to the levels announced on April 2nd

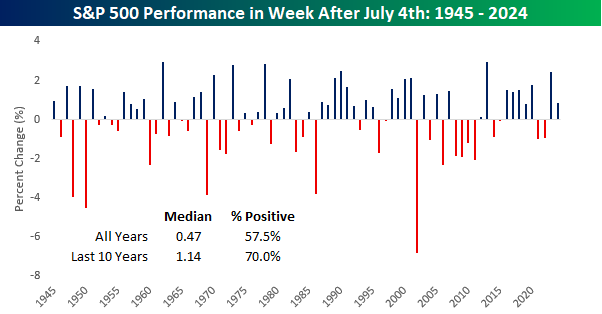

The long holiday weekend is over, and it’s time for investors to get back to business as Q2 earnings season is right around the corner, and the tariff situation is likely to become more concrete. One thing bulls have going for them heading into this week is the seasonal calendar. Since WWII, the S&P 500’s median performance during the week after the July 4th holiday week has been a gain of 0.47% with positive returns 57.5% of the time. More recently, performance has been even stronger with a median gain of 1.14% and positive returns 70% of the time.