Sep 5, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Change before you’re forced to change.” – Roger Goodell

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are in rally mode this morning ahead of the Non-Farm Payrolls report at 8:30, while treasury yields are at their lows for the week. The rally in US stocks follows what has been a strong morning in Europe, as well as some solid gains in Asia.

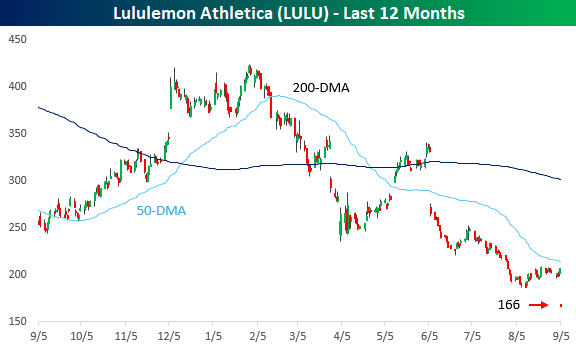

Earnings season may be mostly in the rearview mirror, but some reports are still trickling in, and last night saw a very disappointing report from Lululemon (LULU). While the athletic apparel maker reported better-than-expected earnings on inline revenues, full-year earnings guidance was slashed by 10%. While the stock was only trading at 14 times earnings heading into the report, investors are not taking kindly to the lowered guidance. In pre-market trading, shares of LULU are down roughly 20% to their lowest level since March 2020. Earlier this year, the stock was trading as high as $420. It’s at $166 now!

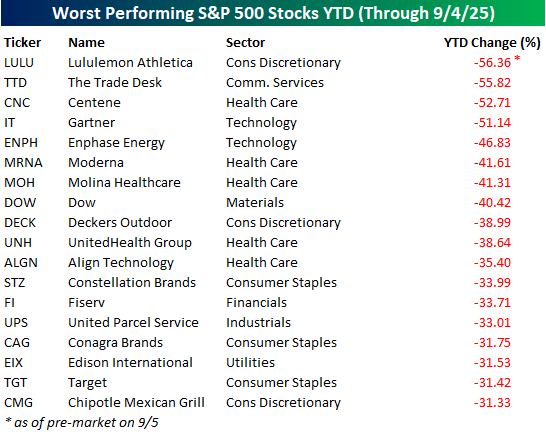

Taking into account this morning’s decline, LULU now ranks as the S&P 500’s worst-performing stock on a YTD basis and is one of just four stocks in the index that have lost more than half of their value. The other three are The Trade Desk (TTD), Centene (CNC), and Gartner (IT). Along with those four stocks, another 14 are down over 30%, including Deckers Outdoors (DECK), Align Technology (ALGN), and Chipotle (CMG). There was a time when these stocks were among the biggest highfliers, but nowhere is the phrase “what have you done for me lately” more applicable than in the stock market.

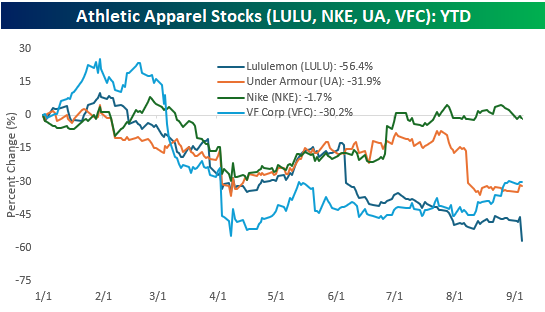

LULU’s decline has been painful, but it has also been part of a broader decline in athletic apparel companies. While none of them are down anywhere nearly as much as LULU, shares of Nike (NKE), Under Armour (UA), and VF Corp (VFC) are all in the red YTD. With a “workout” these days now involving nothing more than a jab in the thigh, you don’t need yoga pants and a pair of sneakers to do that!

Enough of the bad news. If we’re going to dwell on the worst-performing stocks in the market this year, we have to give equal time to the top performers, so the table below shows the 15 stocks in the S&P 500 that are up at least 50% YTD. You may think that the market is being led entirely by tech, but six sectors are represented on the list of the 15 biggest winners. Tech is tied for the lead in terms of representation, but four stocks from the Industrials sector are also represented, including GE Vernona (GEV) and General Electric (GE). As hard as it would have been to imagine a couple of years ago seeing LULU, DECK, ALGN, and CMG on the list of biggest losers, it would have been just as hard to think a stock with “GE” in its name would ever be on the biggest winners list, let alone two!

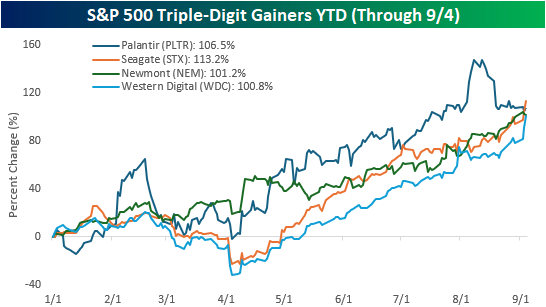

At the top of the list of biggest winners were four stocks that have already doubled this year – Palantir (PLTR), Seagate (STX), Newmont (NEM), and Western Digital (WDC). Seeing PLTR at the top of the list isn’t surprising, but STX, NEM, and WDC? Where did they come from? Goldminers aren’t exactly the sexiest stocks in the market, and when most investors think of tech stocks, STX and WDC are probably two of the last stocks that come to mind. It just goes to show that the biggest winners in the market often come from places seemingly out of the blue where the fewest investors are looking.

Sep 4, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you fail to prepare, you’re prepared to fail.” – Mark Spitz

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Equity futures are skewed to the upside as yields rise, but a weaker-than-expected ADP Employment report at 8:15 has put a modest damper on the tone in equities. The 8:30 batch of data showed that Unit Labor Costs were weaker than expected, while Non-Farm Productivity came in better than expected. Jobless claims were mixed, with initial claims rising slightly while continuing claims saw a modest decline.

In Asia, most equity indices in the region were higher, with Japan leading the way (+1.5%), but China bucked the trend and traded lower on reports that the government is considering restrictions on stock trading to reduce speculation. European equities are also higher this morning, with France being the exception, following a sharp decline in shares of Sanofi.

As concerns over an uptick in inflation continue to simmer (even as employment slows), raising questions about how much the Fed will realistically be able to cut rates, the yield on the 10-year US Treasury doesn’t seem overly worried. Since peaking early in the year at just over 4.8%, yields have been steadily trending lower with a series of lower highs since Spring. During this period, there has been a floor at the 4.20% level, but this morning that level is being tested again as the yield briefly moved below 4.2%.

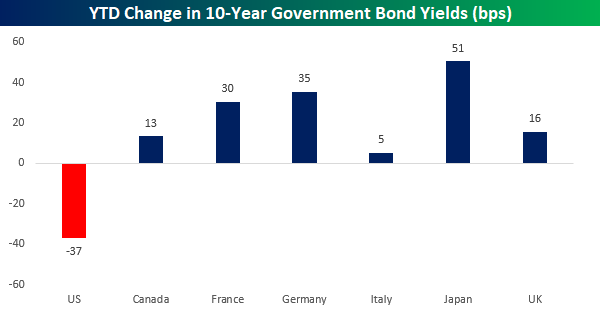

The drop in yields has also occurred against a backdrop of chatter over whether global investors were looking to exit US assets. In global fixed income markets, that doesn’t appear to be the case. While the 10-year yield has declined 37 basis points (bps) YTD, the sovereign 10-year yield of every other G7 country has increased anywhere from 5 bps in Italy to 51 bps in Japan.

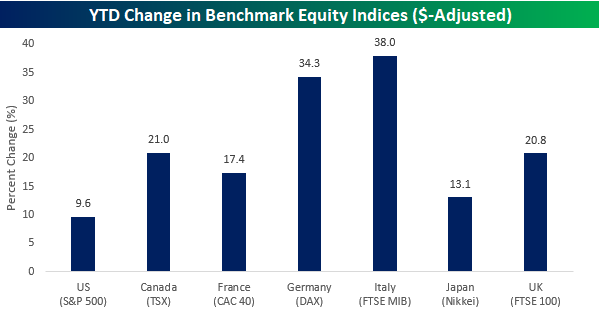

In global equity markets, US exceptionalism hasn’t been as evident. While the S&P 500 is up 9.6% YTD, the benchmark equity index of every other G7 country is up by a larger amount. Japan is the closest in terms of performance to the US (+13.1%) while Italy and Germany are both up over 30%!

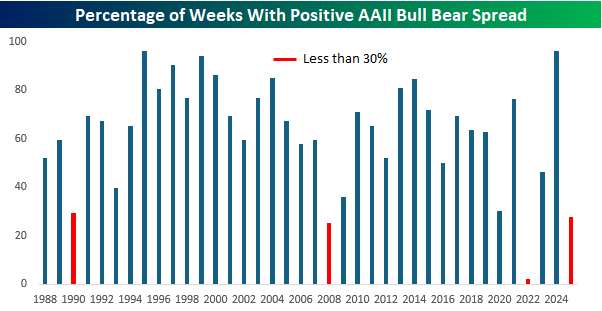

While US equities entered September right near all-time highs with healthy gains for the year, investor sentiment remains skeptical. The latest sentiment survey from the American Association of Individual Investors (AAII) showed a decline in bullish sentiment to 32.7% while bearish sentiment increased to 43.4%. The results pushed the bull-bear spread further into negative territory, marking the fifth straight week that bears outnumbered bulls in what has been a relatively consistent trend of negative sentiment this year.

The chart below shows the percentage of weeks by year when the weekly AAII survey had a positive bull-bear spread. So far this year, the spread has been positive just 28% of the time, which stands in stark contrast to last year, when the bull-bear spread was positive 96% of the time, tied only with 1995 for the most ever in a year. If the current pace of negative readings continues, it will be just the fourth year that the bull-bear spread was positive less than 30% of the time, with the only other years being 1990, 2008, and 2022. It’s understandable to see negative sentiment in bear market/recessionary environments like 1990, 2008, and 2022, but what’s the excuse this year?

Sep 3, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Not only strike while the iron is hot, but make it hot by striking.” – Oliver Cromwell

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

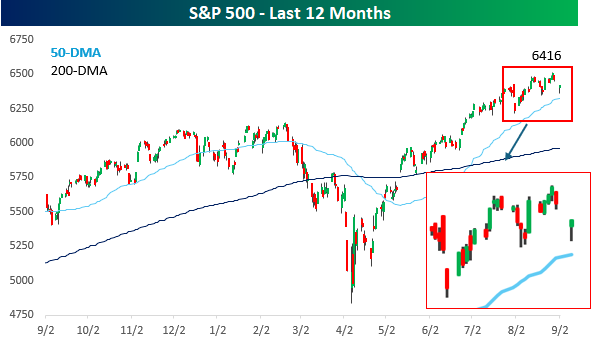

September may have started on a poor footing. Still, after a bounce yesterday afternoon, the positive tone carried over overnight and into this morning, following positive news for Alphabet (GOOGL) and, by extension, Apple (AAPL). Asian stocks were mostly lower overnight, with the Nikkei falling nearly 1% and China falling more than a percent. In Europe, though, there has been broad-based strength with the STOXX 600 trading up over 0.6%. On the economic calendar today, the only reports on the calendar are JOLTS and Factory Orders.

Yesterday was an unsurprising start to September, and the silver lining was that the ‘buy the dip’ mentality of investors that we discussed in Friday’s Bespoke Report remained intact. The S&P 500 sold off sharply early in the session, tested those lows right around midday, and then rallied throughout the session to finish right at the highs for the day. From a short-term perspective, the S&P 500 has now made two higher highs and two higher lows, reinforcing the overall upward trend.

Both the S&P 500 and Nasdaq are priced to continue yesterday afternoon’s bounce this morning, and the key driver is Alphabet (GOOGL) following last night’s ruling that it would not be required to sell its Chrome browser. In response, the stock is on pace to gap up nearly 6%. If these levels hold through the opening bell, it would be the largest upside non-earnings related gap higher since 2008.

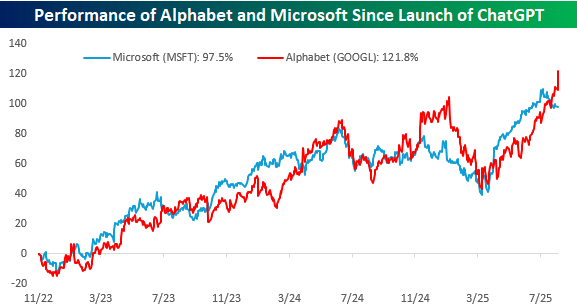

With today’s gain, we also wanted to provide an update on the comparison between GOOGL and Microsoft (MSFT) since the launch of ChatGPT. The overall consensus has been that MSFT’s quick action and investments into OpenAI helped it to win the AI race among the hyperscalers, but the market has a different opinion. While MSFT has nearly doubled since the launch of ChatGPT in November 2022, at the open today, GOOGL will be up over 121%. While MSFT has won in the court of public opinion, GOOGL has won in the wallet.

Sep 2, 2025

This content is for members only

Sep 2, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I was never part of the crowd.” – Jimmy Connors

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After four summer months when the S&P 500 gained at least 1.9%, September is starting on a characteristically weak note as futures are pointing to a decline of 0.7% to kick off the month. As detailed in this morning’s commentary, there’s nothing in the way of a major catalyst to speak of besides an uptick in treasury yields around the world. Gold and oil prices are also higher. The only economic reports on the calendar are the ISM Manufacturing for August and July Construction Spending. The ISM report is expected to come in below 50 again but show an uptick from last month’s weaker-than-expected reading of 48.0 to 48.9 this month. Construction spending is expected to show a modest uptick of 0.1% after declining 0.4% in June.

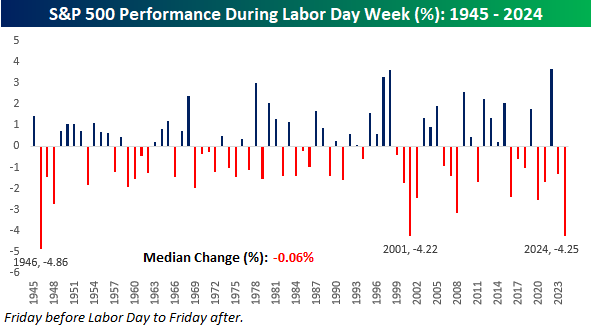

Historically, Labor Day week has been somewhat weak. Since 1945, the S&P 500’s median performance during Labor Day week has been a decline of 0.06% with gains just half of the time. Ironically, last year’s 4.25% decline was the weakest since 1946 and just the third time since 1945 that the index declined 4% or more during the week.

In terms of what that weakness means for the rest of the year, it doesn’t really mean anything. Last year, the S&P 500 rallied 4.13% through year-end after the 4.25% decline. In 2001, it rallied 1.28% for the rest of the year, and in 1946, it fell 8.11%. For all years since 1945, the S&P 500’s median performance from the end of Labor Day week through year-end has been a gain of 3.78% with gains 73% of the time.

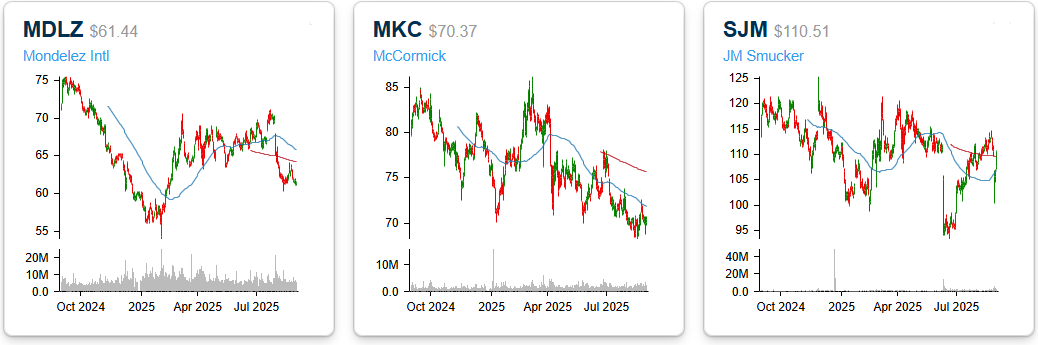

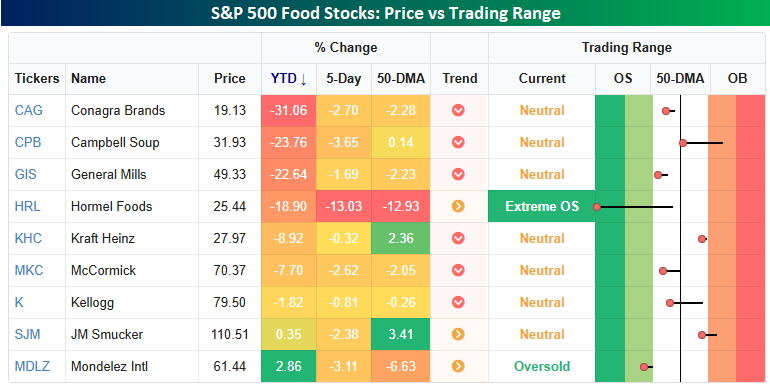

One of the bigger individual stock stories this morning is the announcement that Kraft Heinz (KHC) will split itself into two companies in an effort to boost growth. As the graphic below shows, KHC and its peers could use all the help they can get. The snapshot below from our Trend Analyzer shows where KHC and its peer stocks are trading relative to their trading ranges. On a YTD basis, just two of the nine stocks listed are up on the year, and four of them are down by double-digit percentages. KHC isn’t quite down 10%, but it was before Friday’s news of the breakup originally broke. Last week was particularly poor for the group as well, with all nine trading down anywhere between 13% for Hormel (HRL) to a fractional decline for KHC.

If you have a weak stomach, you may want to skip the section below, which shows one-year price charts of the nine stocks listed above. Practically every single one of them has the same pattern – top left to bottom right. These are the types of charts you would expect to see during a bear market rather than after one of the strongest 100-day market rallies in history!