Bespoke’s Morning Lineup – 12/2/25 – Code Red

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Colonel Jessup! Did you order the Code Red?!” – Lieutenant Daniel Kaffee, A Few Good Men

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Silicon Valley is abuzz this morning following reports that OpenAI CEO Sam Altman declared a ‘code red’ on Monday as competition from Google and Anthropic intensifies. To fight the threats, initiatives like an advertising model, AI agents, and a personalized “Pulse” service for individual users have been temporarily put on hold. This latest story is just another example of how quickly the currents can change in the AI space, and that no one’s lead is safe.

Going back to the internet era, remember the ‘browser wars’? Google Chrome now dominates the browser space with about 70% market share, but you may find it hard to believe that it wasn’t released until 2008, more than eight years after the Internet bubble burst! There’s still a lot of runway left in the battle for AI supremacy.

US stocks started off December with broad-based declines as the S&P 500 fell 0.5%, but the Dow fared worse, falling nearly 1% as the Nasdaq outperformed, falling just 0.38 as Nvidia’s 2% gain propped that index up. The real area of weakness, though, was in the small-cap Russell 2000, which fell 1.25%. So much for the broadening trade.

Bulls started off the overnight session looking to put up a fight as S&P 500 futures rally 0.25% while the Nasdaq looks to open 0.38% higher. Crude oil is down fractionally as it wasn’t able to trade back above $60 in yesterday’s rally, while gold falls 1%, silver plunges 2%, and platinum falls even more (-2.38%). Crypto had a rough start to December, but has bounced back over 2% this morning, trading back above $87K.

Asian stocks saw mostly muted moves overnight. The one exception was South Korea, as the Kospi rallied nearly 2% following confirmation from US officials that tariffs on exports to the US would be cut to 15%. In Europe, the tone is also positive as the STOXX 600 bounces 0.3% with Germany rallying 0.60%.

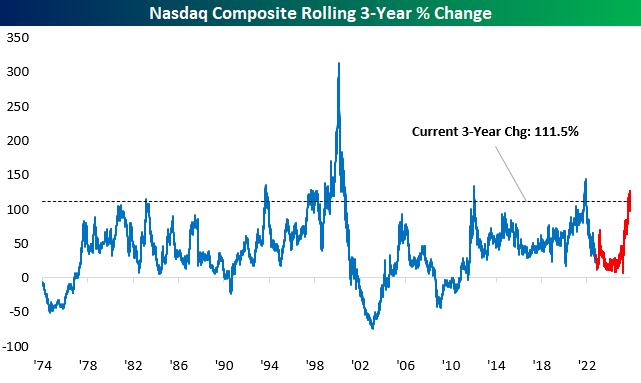

In last night’s Closer, we looked at the performance of the Nasdaq over the three years since the release of ChatGPT and compared that performance to other major tech releases of the last 50 years. Since the launch of ChatGPT in late 2022, the Nasdaq has rallied more than 100% ranking as the strongest three-year return since the period coming out of Covid and the massive tech investment to facilitate the work-from-home era. Outside of that period, the only other three-year period that was stronger was the one coming out of the Financial Crisis.

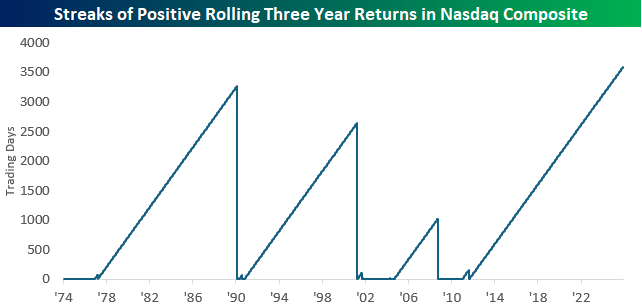

In addition to the massive rally of the last three years, what stood out in the chart was how long it has been since the Nasdaq had a negative rolling three-year return. The last time it was negative was in August 2011, just after S&P downgraded the AAA sovereign US credit rating more than 14 years ago! The chart below shows streaks of positive readings in the Nasdaq’s rolling three-year return, and at a length of 3,590 trading days, the current streak easily ranks as the longest. Besides that, three years ago the Nasdaq was under 11,500, or more than 50% below current levels. In other words, barring a large decline, the current streak of positive three-year returns isn’t going away soon.

Bespoke’s Morning Lineup – 12/1/25 – Back to Gravity

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Many people are busy trying to find better ways of doing things that should not have to be done at all. There is no progress in merely finding a better way to do a useless thing.” – Henry Ford

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a zero-gravity rally on Friday that pushed the S&P 500 into positive territory for the month and extended the S&P 500’s monthly winning streak to seven, equities are rediscovering gravity to start December as futures on the major averages all trade lower. The Nasdaq is poised to open down nearly 1% while the S&P 500 faces a 0.7% decline. Even with equities falling, treasury yields are also higher as the 10-year ticks up 3 bps to 4.05%. Crude oil is up just over 1% as OPEC+ announced plans to maintain output levels rather than raise them, and gold is back near $4,300, gaining about 0.8%. The big loser on the day, though, is Bitcoin. With a decline of over 6%, the largest crypto is on pace for its worst day since March, and part of the weakness could be related to reports that Strategy (MSTR) could potentially be forced to sell some of its holdings to fund its dividend.

The weakness started in Asia as the Nikkei fell close to 2% as JGB yields continue hitting levels not seen since before the Financial Crisis, as expectations for a rate hike later this month solidify. In China, stocks went the other way with the Shanghai Composite rallying 0.7%, even as November Manufacturing and Non-Manufacturing PMIs remained in contraction territory.

In Europe, the losses have been more uniform as the STOXX 600 falls 0.5% as Manufacturing PMIs for the economic bloc and individual countries missed expectations. The biggest loser on a country basis is Germany, as the DAX declines more than 1.5% as defense contractors have been especially weak on reports of progress in the Russia-Ukraine war talks.

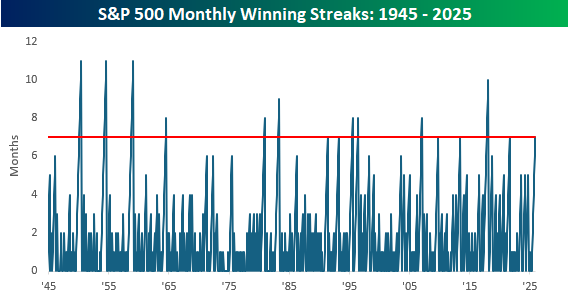

As mentioned above, the S&P 500’s winning streak extended to seven in November, and that’s the longest streak of gains for the index in more than four years (August 2021). Since the end of WWII, there have been 15 other seven-month winning streaks, with the longest being eleven. Believe it or not, that happened three times, all of which were all in the 1950s. So, while history always talks about the roaring twenties, don’t forget about the fantastic fifties.

Outside of those three eleven-month winning streaks in the 1950s, the only other streak that extended into the double-digits was the 10-month streak that kicked off President Trump’s first term in office, ending in January 2018 (seventh month was October 2017). Getting back to the most recent streak, the seven months ending in August 2021 were followed by a sharp decline of 4.8% the following month, and weak returns thereafter.

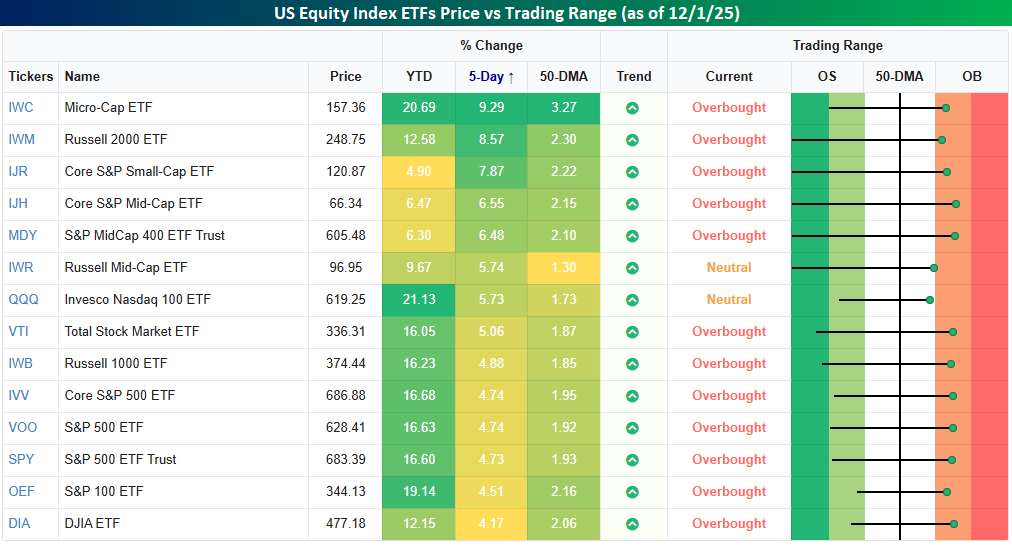

Last week, right before Thanksgiving, we pointed out that the S&P 500 and other major US equity indices had quickly gone from oversold to neutral. In the two trading days since then, the rally kicked into another gear with little selling resistance (as evidenced by Friday’s rally), and all but two of the major equity index ETFs in our Trend Analyzer snapshot have moved into overbought territory. The only exceptions are the Russell Mic-Cap ETF (IWR) and the Nasdaq 100 (QQQ), and while they may not be overbought, they still rallied over 5% in the five trading days through last Friday’s close (from close on 11/20).

Of all the ETFs shown, every one of them was up at least 4% in the trailing five trading days. While large-cap ETFs lagged with gains of less than 5%, small caps had a day in the sun with the Russell Micro Cap ETF (IWC) surging 9% while the Russell 2000 ETF rallied over 8.5%. While usually not the case in recent months, this rally has been one where big gains came in small packages.

Bespoke’s Morning Lineup – 11/28/25 – Going Down to the Wire

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Scientific knowledge advances haltingly and is stimulated by contention and doubt.” – Claude Lévi-Strauss

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Hope everyone in the States had a great Thanksgiving! Futures are halted this morning following a technical glitch on the CME, but equity ETFs tracking the S&P 500 and Nasdaq are indicated to open up 0.34% and 0.51% respectively, on this holiday-shortened day. Small caps are also higher with the Russell 2000 poised to open up 0.33%, although that won’t even be enough to erase the declines seen in the final half hour of trading on Wednesday. Treasury yields are little changed relative to Wednesday’s close, while crude oil and gold are both up about 0.60%. Even Bitcoin isn’t doing much this morning as it hovers just above $91K, although that’s a big improvement from the $86K level it was at on Wednesday afternoon.

Today may not seem like an important day, with many people taking the day off and the market open for only 3.5 hours, but it is coming down to the wire on the S&P 500’s six-month winning streak. Heading into today, the S&P 500 is down 0.40%, which is only slightly more than SPY’s current pre-market gain. So grab your popcorn, and don’t hit the mall just yet!

In most Asian markets, trading activity to close out the week was generally positive, adding to an already positive week. The one exception was South Korea, where the KOSPI fell 1.5%, taking its YTD gain down to just below 2% on the week. In Japan, CPI came in at 2.8% y/y, which was slightly higher than expected. Despite that increase, a BoJ policymaker contended that underlying inflation remains below their 2% target.

In Europe, trading is very quiet so far this morning, with the STOXX 600 up 0.1%, but the index and the individual country benchmarks that underly it are all firmly in positive territory for the week. French CPI data for November unexpectedly declined 0.1% versus expectations for an unchanged reading.

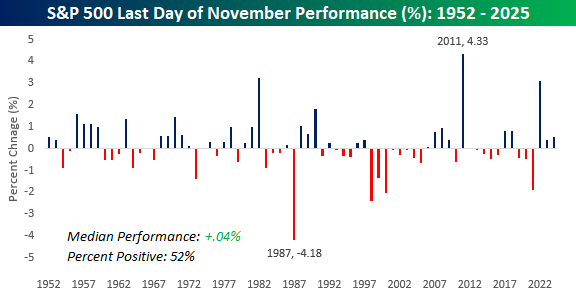

From a market perspective, there was a lot to be thankful for yesterday, especially given where it stood at various points in the year. As we head into the last day of the penultimate month of 2025, we wanted to take a quick look at how the S&P 500 has historically performed on the final trading day of November and the first trading day of December.

Earlier this week, we showed how Black Friday has historically been a positive day for stocks, with the S&P 500 averaging a one-day gain of 0.24%. However, Black Friday isn’t usually the last trading day of the month, and market performance hasn’t been particularly strong on that day. Since the five-trading-day week in its current form began in late 1952, the S&P 500’s median performance on the last trading day of the month has been a gain of 0.04% with positive returns 52% of the time.

The worst year was in 1987, when the market was still reeling from the October crash, and the S&P 500 fell 4.18% while the best day was in 2011 – another volatile year – when the S&P 500 rallied 4.33%. 2022 was the third-best performance for the last day of November when the S&P 500 saw a nice gain of 3.09% in the early weeks of the bull market. That also happened to be the exact day that ChatGPT came into our lives!

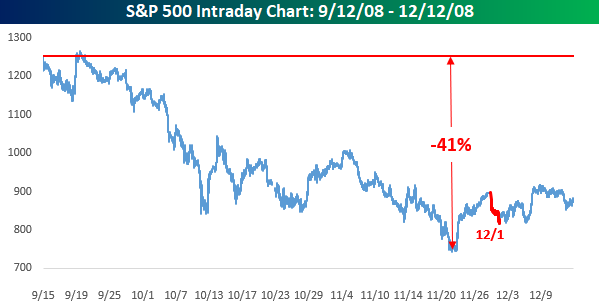

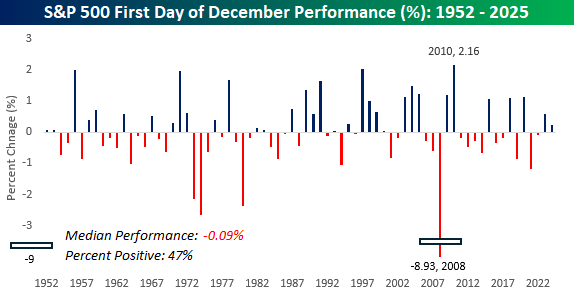

The first trading day of December has also been as bland as an overcooked turkey with no gravy. Since 1952, the S&P 500’s average performance on the first trading day of the month has been a decline of 0.09% with positive returns just 47% of the time. The best performance was a gain of 2.16% in 2010, while the worst was a year earlier in 2008, when the S&P 500 plunged 8.93%. 8.93%! Think about that for a second. We didn’t even fall that much in the latest market pullback (at least not yet), and some people were already acting like it was the end of the world, but in 2008, the S&P 500 fell that much in a single day!

If you’ve been around the block a few times, it may sound hard to believe, but there are now people with driver’s licenses and/or who are applying to college that were born after Lehman Brothers filed for bankruptcy in 2008. Time has a way of dulling memories, especially the bad ones, so for both people who weren’t around during the Financial Crisis and those who were (and just may not have been paying attention), it’s easy to forget how crazy that time was.

That 8.93% decline on the first trading day of December wasn’t just an outlier. In November 2008, the S&P 500 had a daily move of +/-5% on eight of the month’s 19 trading days, and in the three months after Lehman’s bankruptcy, there were 18. That’s more than once every four days!

A better way to show this, though, is to look at an intraday chart of the S&P 500 in the three months following Lehman’s bankruptcy. On the Friday before Lehman went belly up, the S&P 500 closed at 1,251.70. Besides a brief period in the following days, it didn’t reach that level again for a few years, and by Thanksgiving, just over two months later, more than 40% of the S&P 500’s market value was vaporized. Also, you almost need to squint to see it, but that red ‘scratch’ on the right of the November low represents the 8.93% one-day decline from 12/1/08. In the markets, just like life, everything is relative.