Jul 15, 2025

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with some commentary regarding risks that could drive up yields which includes inflation data (pages 1 – 3). We then turn to a look at JB Hunt (JBHT) earnings and how today’s performance shaped up in spite of very weak breadth (page 4). Next, we check in on loan growth (page 5) before finishing with a look at some impressive earnings streaks ahead of earnings season (pages 6 & 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Jul 15, 2025

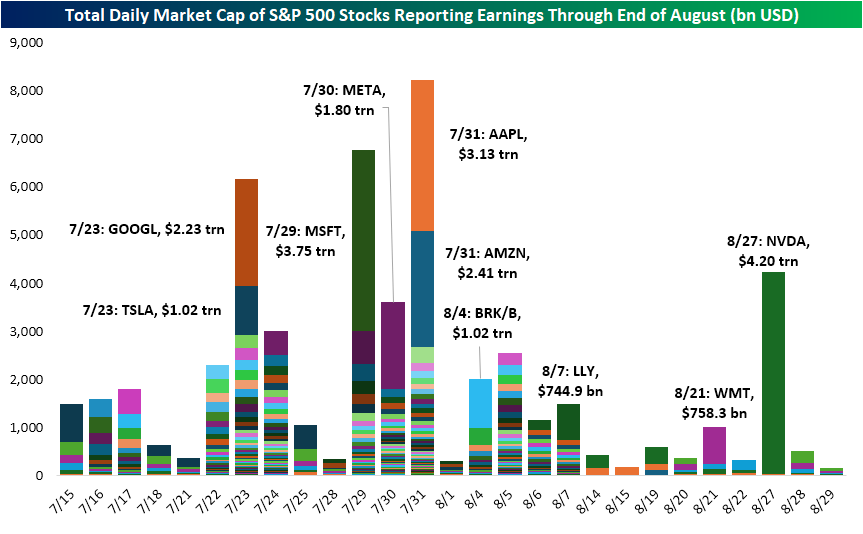

The first of the big banks have reported this morning which means that earnings season is off to the races. For S&P 500 members, Thursday will be the busiest day this week with 17 stocks reporting, and early next week is when the earnings slate really takes off with a total of 44 stocks reporting Tuesday and 47 on Wednesday. As shown below, in addition to having a higher number of stocks reporting, part-way through next week will also account for a significant portion of S&P 500 market cap reporting. On Wednesday (7/23), the first of the mega-caps are up as Alphabet (GOOGL) and Tesla (TSLA) account for nearly half of the over $6 trillion in market cap reporting that day. Most of the rest of the mega-caps will report in the following week with Microsoft (MSFT) starting things off on Tuesday, July 29, with Meta Platforms (META) the next day (7/30), and Apple (AAPL) and Amazon (AMZN) out the day after that (7/31). While Wal-Mart (WMT) has historically marked the unofficial end of earnings season, nowadays it’s NVIDIA (NVDA) that caps things off. WMT is set to report on 8/21, while NVDA is six days later on 8/27.

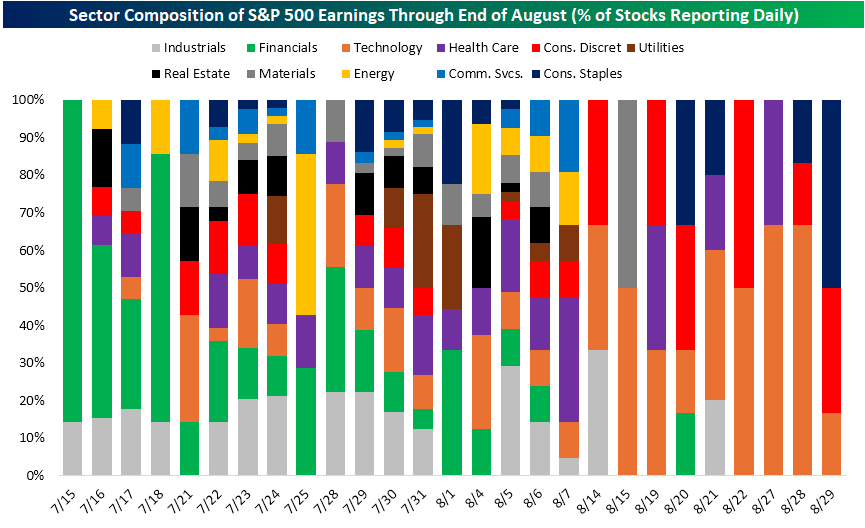

As noted previously, this week’s earnings are dominated by big banks and financial centers. In the chart below, we show the share of stocks from each sector that are reporting each day through the end of August. As shown, the next few days are predominately Financials with Industrials also accounting for a steady share of results (hovering around low double digits). The following few weeks until mid-August (which is the peak of earnings season) has a much greater variety in sectors reporting results whereas the tail end of August is predominately Tech names.

Jul 14, 2025

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with commentary surrounding the prospects of administration officials ousting Fed Chair Powell (page 1) followed by a dive into price action in breakevens (page 2). next, we recap the latest freight activity data from Cass (page 3) before closing with a look at aggregated positioning figures (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Jul 10, 2025

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look into the Fed’s balance sheet (page 1). Next, we check up on jobless claims and the moves in volatility (page 2). We then review performance of stocks based on the estimated tariff rate they face (page 3) and close out with a look into Industrials huge outperformance in 2025 (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!