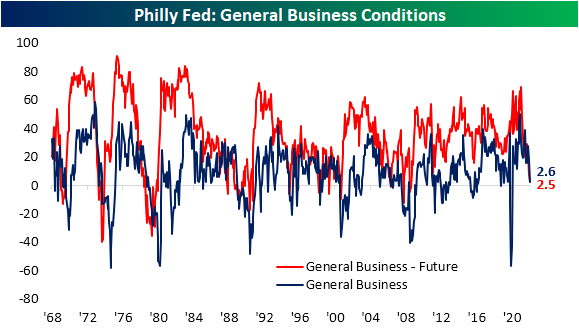

End in Sight For Philly Supply Chain Stress?

On the backs of a disappointing Empire Fed earlier this week, the neighboring Philadelphia Federal Reserve Bank’s own reading on its region’s manufacturing economy also came in well below expectations at the headline level. The index for General Business Conditions was anticipated to decline from a healthy reading of 17 to a more modest 15. Instead, it plummeted to a barely positive reading of 2.6. That would point to a significant moderation in activity in the month of May.

While the headline index fell sharply, the rest of the report was perhaps more mixed. Breadth was certainly weak with only three categories rising month over month (New Orders, Shipments, and Unfilled Orders). As for the indices that declined, on the one hand, some could be perceived as welcome drops with pullbacks in elevated readings of prices and delivery times. On the other hand, the moderation in Number of Employees or CapEx expectations could be taken as a less positive sign for the broader economy.

As shown in the table above, overall most current conditions indices remain historically elevated even after recent declines. Expectations indices meanwhile are generally more depressed with some readings even near record lows. As such, the average normalized distance between the current conditions and expectations categories throughout the report have broken out to the highest level since February 1988 and mid-1975 before that. Put differently, there have rarely been times in which the region’s manufacturers have reported such a dramatic difference between healthy current conditions while also holding a pessimistic outlook.

Taking a closer look at individual categories, New Orders remain well off-peak but ticked higher in May rising 4.3 points to 22.1. There was an even larger jump in expectations, although the level of that index is not nearly as elevated. The modest increase in demand was met with a huge jump in Shipments and Unfilled Orders. With a 16.2 point jump month over month, Shipments are reported to be growing at the fastest rate since the fall of 2020. Given the region’s firms are getting orders out the door at a faster clip, inventories are growing only modestly with that index falling to a barely expansionary 3.2. Additionally, that evidence of improved fulfillment also resulted in a huge drop in expectations for Unfilled Orders. In fact, that index dropped to the lowest level since March 1995. That means the region’s firms expect to work off unfilled orders at a historic rate in the coming months.

The likely reason as to why companies are anticipating such a huge improvement in fulfillment is massive expected declines in lead times. Delivery Times remain elevated but have moderated significantly in the past couple of months. Six-month expectations meanwhile have fallen all the way down to -29.1 which, like unfilled orders expectations, is the lowest level since March 1995.

Another expectations reading that has fallen precipitously in May is CapEx expectations. The reading fell to the worst reading since September 2016 indicating huge moderation in planned investment. Likewise, hiring is expected to slow as has already been observed by the current conditions index. We would note that these readings remain positive, meaning firms are still expecting to take on more hiring and spending on net, but at a more modest rate. Click here to learn more about Bespoke’s premium stock market research service.

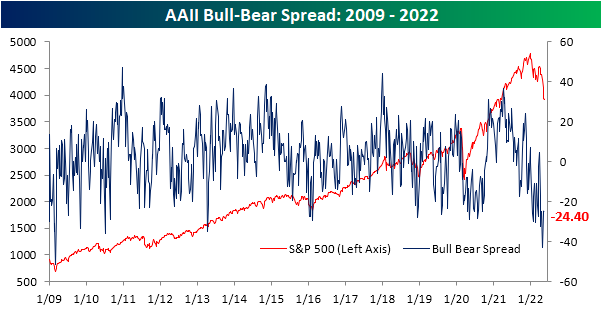

Sentiment Little Changed – Still Bearish

Depending on when a respondent reported their answers to the weekly AAII sentiment survey, they could have been justified in giving either bullish or bearish. From last Thursday’s close to Tuesday, the S&P 500 rallied a little more than 4% but anyone reporting yesterday would have reflected the index giving back all of those gains in a single session. Given that back and forth of equities, sentiment remains little changed. Around a quarter of respondents remain in the bullish camp as has now been the case for three weeks in a row. Albeit a historically low reading, it is a major improvement from readings in the mid-teens only one month ago.

Bearish sentiment meanwhile ticked higher and back above 50% this week. As with bullish sentiment, that is an overwhelmingly pessimistic reading even if it is less extreme than last month when it closed in on a 60% reading.

The bull-bear spread in turn was marginally improved rising from -24.7 to -24.4 indicating sentiment stays heavily slated toward pessimism.

With both bearish and bullish sentiment gaining share this week, the percentage of respondents reporting neutral sentiment fell back below 25% to 23.6%. Click here to learn more about Bespoke’s premium stock market research service.

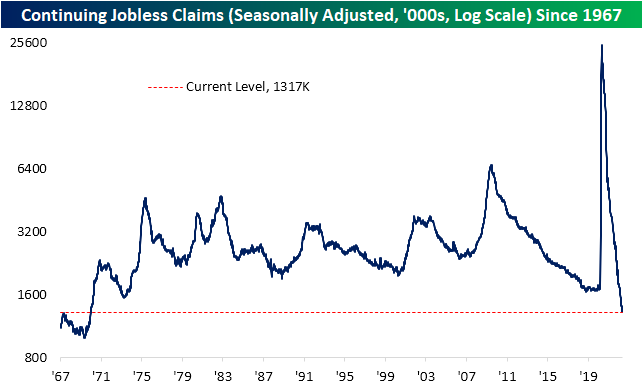

Continuing Claims Keep Falling

Jobless claims have continued to tick higher with this week’s reading rising to 218K. That is an increase of 21K versus last week’s print which was revised back below 200K to 197K. That leaves the seasonally adjusted number at the highest level since January. While there has not been any further improvements, the actual level of claims remains well below the standard historical range near similar levels to the couple of years prior to the pandemic.

Historically, unadjusted claims have fallen week over week more than three-quarters of the time in the current week of the year. However, this year was not one of those occasions as claims rose to 198.7K. While that is not any sort of dramatic increase, it is a somewhat unusual rise a little ahead of when claims have tended to experience a seasonal bottoming out. Looking ahead to the next couple of weeks, claims could see further marginal improvements before resuming a move higher through the early summer.

Continuing claims—which are delayed an additional week to the initial claims number—have been healthier than initial claims as the reading has made yet another multi-decade low per the latest release. Continuing claims are now down to 1.317 million. As low of a reading has not been observed since the last week of 1969. Combined with the uptick in the initial claims number, claims data points to moderating, albeit historically impressive, readings on the number of people filing for unemployment. Click here to learn more about Bespoke’s premium stock market research service.

The Closer – Retailer Wreckage, Slow Building, EIA Update – 5/18/22

Log-in here if you’re a member with access to the Closer.

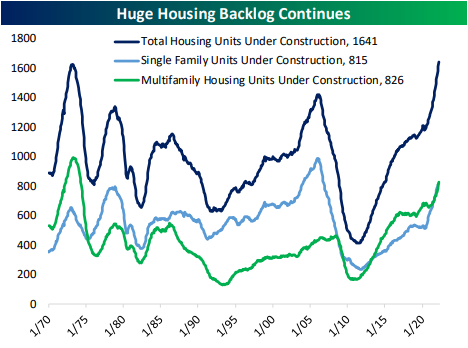

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out tonight with a look at the increase in inventories for major retailers (page 1) followed by an update on energy inventories per the latest EIA data (page 2). We then show how dramatic of a drop certain areas of the market saw today and the ratios of Consumer Discretionary and Energy to Consumer Staples and their predictive power of recessions (page 3). Pivoting over to housing data, we review today’s residential construction figures (pages 4-6) before finishing with a recap of today’s 20 year bond auction (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!