Aug 29, 2022

Log-in here if you’re a member with access to the Closer.

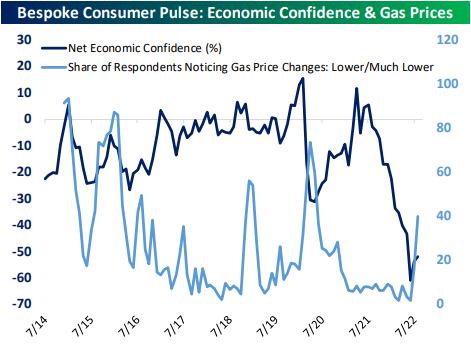

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out tonight with a look at how intraday performance today of the S&P 500 compared to the average since the high on August 16th. We also show the new high in high yield (page 1). We follow up with a preliminary look at some of our Consumer Pulse data (page 2) followed by a final update of our Five Fed Manufacturing Composite for the month of August (page 3). We also take a look at supplemental questions regarding supply chains from today’s Dallas Fed release (page 4). We finish with the latest update of the Commitments of Traders report (pages 5 -7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Aug 29, 2022

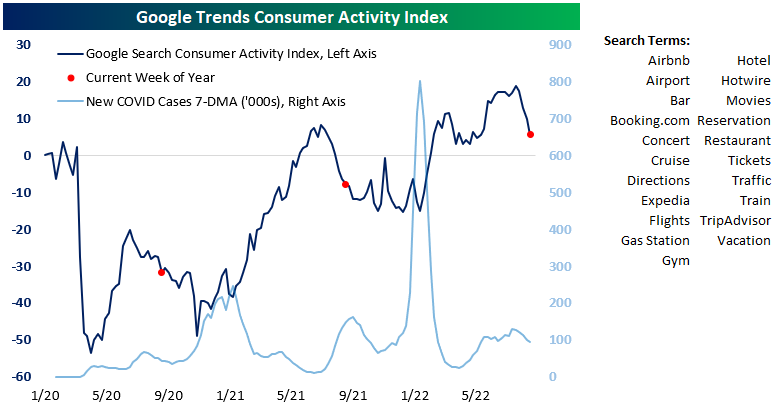

More than two years ago during the summer of 2020, we used Google search trend data to build a US consumer activity index to gauge the strength of the re-opening of society after COVID lockdowns. The index is an aggregation of Google search trend activity for various terms like hotel, cruises, flights, bars, and restaurants, to name a few. When we first started looking at trends in searches for activities that get people out of the house and doing things again, we were trying to see how long it would take to get back to pre-COVID levels. As shown in the chart of the index below, it took until the summer of 2021 to get back to pre-COVID levels, but then activity receded again as we went into the fall last year as Omicron began to spread rapidly.

This summer we saw our Google Trend consumer activity index surge past 2021 highs as people have really started to go out and travel again. Recently, however, we’ve seen a dip in activity. As shown, this appears to be seasonal as we saw the same thing happen last year at this time. Even still, the activity index remains above the level it was at prior to the first COVID cases on US soil, so it’s hard to argue that the consumer has pulled back much — if any — this year, even with inflation raging and some economic indicators flashing recession warnings signs. Click here to learn more about Bespoke’s premium stock market research service.

Aug 29, 2022

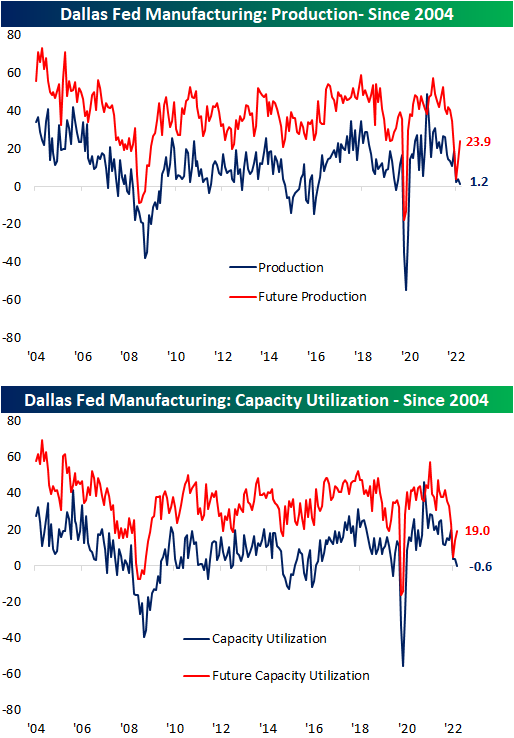

The Dallas Fed updated the final of the regional Fed manufacturing indices this morning. Business Activity remains in contraction but improved versus July. The headline index came in at -12.9, slightly worse than expectations of a reading of -12.7. Expectations saw a similar move with a large bounce off of the worst levels of the post-pandemic period.

Although the headline reading was higher, breadth was disappointing with only five other categories rising month over month. With broad declines across other categories, three indices—Unfilled Orders, Capacity Utilization, and Delivery Times—fell from expansion and into contraction. As has been the case with other regional Fed indices, expectations are generally far more pessimistic with ten of the sixteen indices in the bottom decile of their historical ranges and two others only half of one percentage point away. For comparison, there is not a single current conditions index at that low of a reading.

As demand has pulled back with New Orders seeing the third straight monthly contractionary reading, Production and Capacity Utilization are two of the most depressed indices of the report. These indices are in the 18th and 17th percentiles of their historical ranges, respectively. After this month’s declines, those two indices have reached the lowest levels since May 2020. In other words, consistently weak demand in recent months has resulted in production to go little changed. Ironically, the region’s firms reported much healthier expectations with significant increases in those indices. For Production, the 10.3 point month-over-month increase ranks in the top 7% of all monthly readings.

Likely another result of weakened demand, both Prices Paid and Received have continued their sharp declines across both current conditions and expectations. Prices Paid fell for the third month in a row and is now at the lowest level since October 2020 whereas Prices Received has fallen five months in a row and is down to the lowest level since February 2021. Not only are firms seeing a deceleration in price increases, but Delivery Times actually fell into contraction for the first time since June 2020. Paired with that, Inventories are also signaling improvements in supply chains as this month marked the fourth consecutive expansionary reading; the longest such streak since a six-month streak ending in January 2019. Expectations, however, are now calling for that dynamic to remain for much longer as the drop to -9.7 is the lowest reading since April 2020. Click here to learn more about Bespoke’s premium stock market research service.