Nov 28, 2022

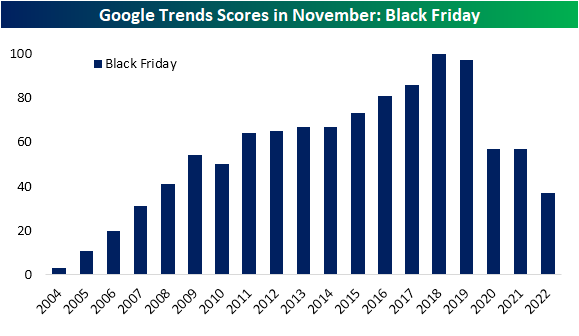

Black Friday and Small Business Saturday are now in the rearview and Cyber Monday is underway as the holiday shopping season is off to the races. There has been a secular shift to online shopping over the past decade meaning Black Friday has a larger online element than the early bird in-store sales of yesteryear. Cyber Monday, meanwhile, may not be the main e-commerce-focused shopping day of the post-Thanksgiving week. Regardless, data from Adobe showed record online sales this year on Black Friday. While those actual sales figures are perhaps a more concrete and noteworthy data point to gauge the success of the day in generating sales, we would note that Google Search activity for the shopping day has been on the decline in the month of November (when it peaks) for the past few years now. The pandemic in particular has resulted in a sharp downward move in searches for the term. In fact, this year is on pace to have seen the lowest search interest for “Black Friday” since 2007, though with the month not quite over, data is still technically incomplete and can be revised higher.

Similarly, news story mentions of Black Friday and Cyber Monday have generally trended lower over the past few years. In the chart below, we show the number of monthly news story mentions as tracked by Bloomberg in November of the terms throughout the past decade. To make it read similar to the chart above, we have indexed these readings to their peaks at 100.

Cyber Monday mentions peaked all the way back in 2018 and are currently around the low end of readings of the past several years. Black Friday, meanwhile, peaked last year, but that appears to have been a bit of an outlier as readings have generally been trending lower since 2019. All of this is not necessarily to say Cyber Monday and Black Friday are less important than in the past, but instead have likely become more ingrained into the holiday season and thus less talked about/researched.

As for how that translates to retail stocks, like consumers, investors appear to get lower prices from retailers during the busiest shopping days of the year! On average, the SPDR S&P Retail ETF (XRT) has declined 0.22% on Black Friday during its history and 1.3% on Cyber Monday. That compares to an average gain of 5 bps on all days. Additionally, there has been little consistency in positive price action. XRT has only risen a little better than a third of the time on Black Friday and just 17.65% of the time on Cyber Monday. In other words, today’s 0.66% drop in the ETF is by no means unusual. Click here to learn more about Bespoke’s premium stock market research service.

Nov 28, 2022

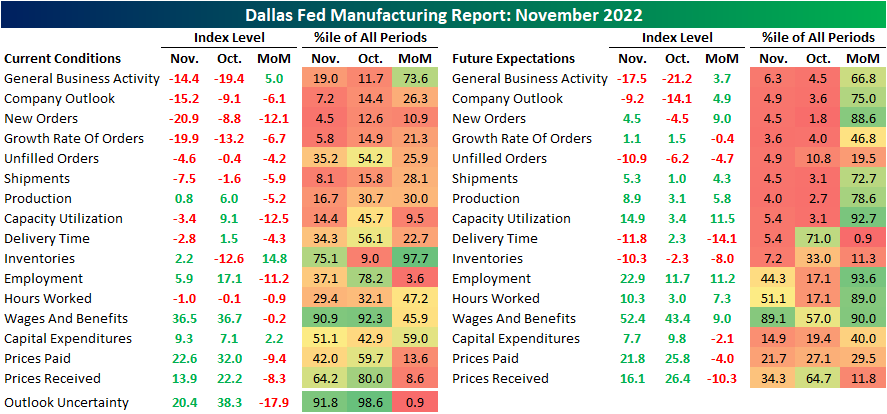

At face value, today’s release of the Dallas Fed’s manufacturing report put up a decent number with the General Business Activity index coming in at -14.4. That was up 5 points month over month and was handily better than expectations which were pointing to a further decline down to -21. Regardless of the better-than-expected reading, the negative number indicates the region’s manufacturing activity continues to decline at a steady pace (the index is still in the bottom quintile of readings in spite of this month’s rebound), and the other components only tainted the picture.

Outside of the headline number, there were only two other components with higher month-over-month readings: Inventories and Capital Expenditures. A slightly higher number of indices are in contraction than expansion with some of the more important readings like New Orders appearing to have cratered the most. Although there were more positive month-over-month moves, expectations indices are broadly sitting at far weaker levels relative to their histories than the current conditions indices. Of the 16 indices, 10 are in the bottom decile of all periods.

Of the current conditions indices, one of the largest declines has been for capacity utilization. That index fell from expansion into contraction in November plummeting 12.5 points (a bottom decile monthly move). Paired with a barely expansionary reading of 0.8 for production, these readings point to the region’s manufacturers cutting down on their output.

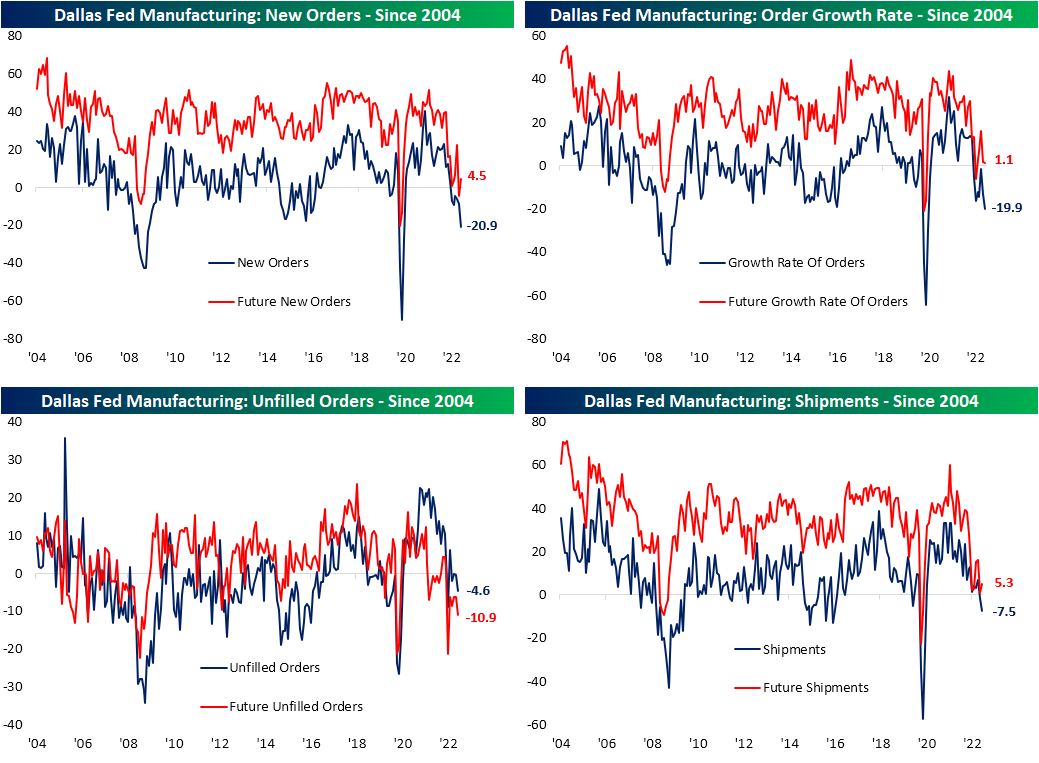

The reason for the decline is that demand has been crushed. New Orders fell another 12.1 points month over month to hit a fresh low of -20.9. That is the weakest reading since May 2020 and the only other sub-20 readings came in the first half of 2009. Unfilled Orders and Shipments are contracting in turn. While those two indices are likewise at post-pandemic lows, they are not quite as historically depressed as New Orders.

While it might not exactly net out the negatives of demand and production weakening dramatically, if there is a silver lining in this month’s report, it is the relief in price pressures. Both indices for Prices Paid and Received have plummeted reversing large portions of the post-pandemic increase. That is not to say prices themselves are turning lower, but they are increasing at a much less dramatic clip. Delivery times, on the other hand, are contracting with expectations predicting far larger declines down the road. Additionally, on the supply chain front, Inventories have begun to rise likely as a result of crimped demand.

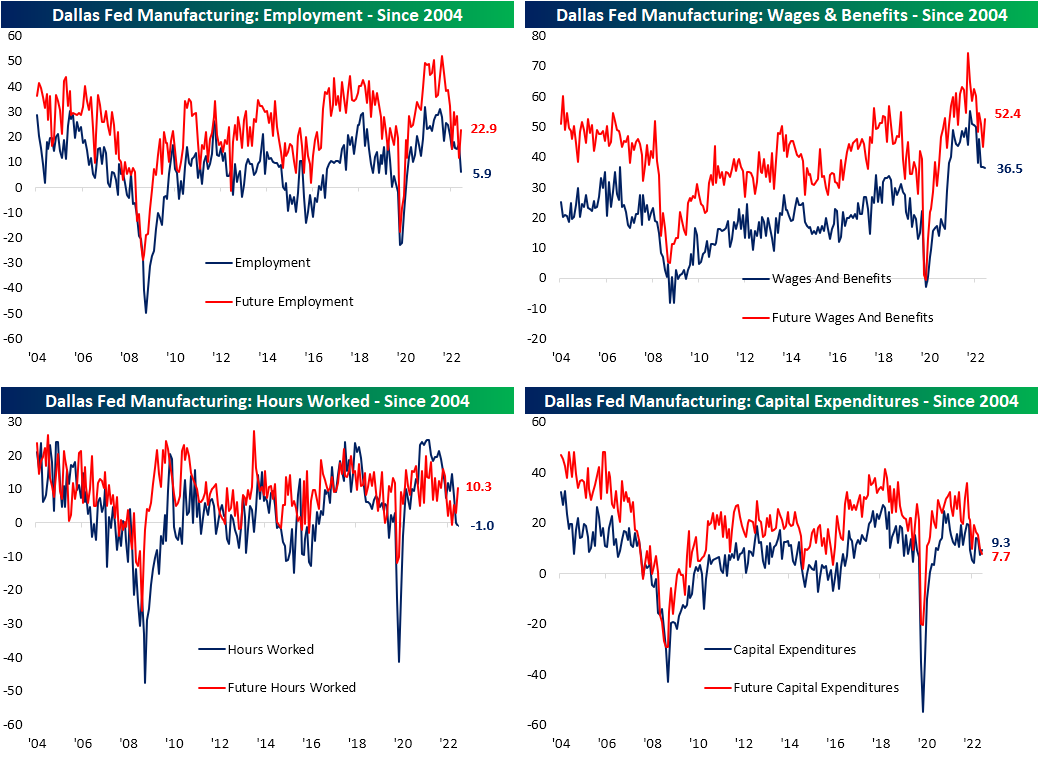

Employment metrics were another notable area of deterioration this month. While Wages and Benefits went little changed and are at the low end of the past year and a half’s range, Hours Worked are falling and hiring has slowed as the Employment index fell back into single digits to the lowest level since July 2020. Click here to learn more about Bespoke’s premium stock market research service.

Nov 25, 2022

Bespoke’s Crypto Report contains numerous technical, momentum, and sentiment charts for bitcoin, ethereum, and other key cryptos. Page 1 of the report includes our weekly commentary on the space and attempts to identify any new trends that are emerging. The remaining pages include important overbought/oversold levels to watch, charts on historical drawdowns and rallies, seasonality trends, futures positioning data, Google search trend shifts, and more. Our weekly Crypto Report is produced so that followers of the space can more easily stay on top of price action, technicals, seasonality, and sentiment.

Sign up for a monthly or annual subscription to Bespoke Crypto to receive our weekly Crypto Report and anything else we publish related to cryptos. Note: If you’re currently a Bespoke Premium, Bespoke Newsletter, or Bespoke Institutional subscriber, you’ll need to subscribe to Bespoke Crypto as an add-on to receive access. The weekly Crypto Report and any additional crypto analysis is not included with our Premium, Newsletter, or Institutional memberships. You can sign up for Bespoke Crypto and receive our Crypto Report in your inbox weekly using the monthly or annual checkout links below. If you sign up for the annual plan, the first year of access is 50% off!

Bespoke Crypto Access — Monthly Payment Plan ($49/mth)

Bespoke Crypto Access — Annual Payment Plan ($247.50 for the first 12 months, then $495/year in year 2 and beyond)

Bespoke Investment Group, LLC believes all information contained in this service to be accurate, but we do not guarantee its accuracy. None of the information in this service or any opinions expressed constitutes a solicitation of the purchase or sale of any securities, commodities, or cryptocurrencies. This service contains no buy or sell recommendations. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Nov 23, 2022

Log-in here if you’re a member with access to the Closer.

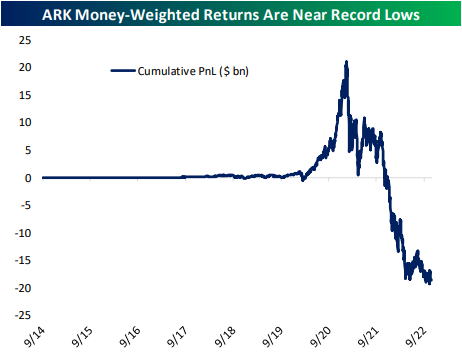

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin tonight with a look at what tones were present in today’s minutes. We also check in on flows for the ARK ETF complex (page 1). Next we recap today’s durable good orders numbers (page 2) followed by a rundown of new home sales (pages 3 and 4). We finish with a look at the latest EIA data (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!