B.I.G. Tips – Fed Day Looms

This content is for members onlyBespoke Stock Scores — 12/13/22

This content is for members onlyInflation Concerns Give Way to Interest Rate Worries

In an earlier post, we detailed the latest NFIB survey of small business optimism. Included in that report are survey results of what small businesses are reporting to be their most important problems to their business. As could be expected with CPI continuing to run in the 7% YoY range, inflation remains top of mind. 32% of respondents to the November survey reported inflation as their biggest concern, slightly outnumbering those reporting cost or quality of labor as the biggest issue. While that continues to be a historically large share of responses, the reading did fall one percentage point month over month as it remains off the peak of 37% in July.

As previously mentioned, behind inflation, the cost or quality of labor (combined) is the next biggest issue for small business, accounting for 30% of responses. That matches the readings from this past July and March for the lowest readings since January 2021. Paired with the other labor related indices of the report, these figures point to some softening of the labor market.

The November report of course coincided with the midterm election. Historically, the NFIB survey has been fairly sensitive to political happenings and the reading on the percentage of respondents reporting government red tape or taxes as their biggest issues has been a good proxy for this. In the past, the reading has tended to be higher during Democrat administrations and lower during Republican administrations. However, during President Biden’s time in office, high inflation has resulted in few respondents seeing political related problems as their biggest issue. That was re-emphasized in November as the reading returned to tie July’s record low of only 16%. We would note that this reading has the potential to turn higher given that past midterm months like 1990, 2002, and 2018 have marked short term spikes lower and higher.

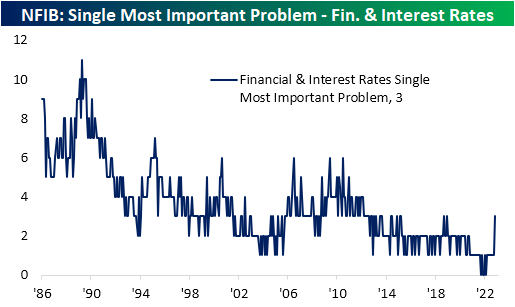

With those biggest issues all seeing a lower share in November, it begs the question of what problems replaced them? Poor sales (+1 ppt), Cost/Availability of Insurance (+2 ppt), Competition from Small Businesses (+2 ppt), and Financial & Interest Rates (+2 ppts) all saw higher readings last month. Of those problems, the latter two are perhaps the most interesting. Historically, neither of these two issues have tended to rank particularly high up among the ten choices given in the survey, but in the past year their share has been decimated without anyone reporting them to be the biggest problems at certain points. That is less so the case today. Competition from big businesses has risen back up to 5% of responses; a reading that would have been similar to much of the first half of the 2010s previously.

Meanwhile, as interest rates have risen rapidly, 3% of responses saw problems with financials and interest rates. Although that is not a large share of total responses, it was the highest share in nearly four years. The NFIB survey is a relatively minor data point and this issue accounts for an overall small share of responses meaning it is highly unlikely this would so much as be considered in regards to monetary policy, however, one potential takeaway of these responses is that small businesses are at least beginning to see some negative impacts of a higher rate environment. Click here to learn more about Bespoke’s premium stock market research service.

Inflation Subsiding For Small Business

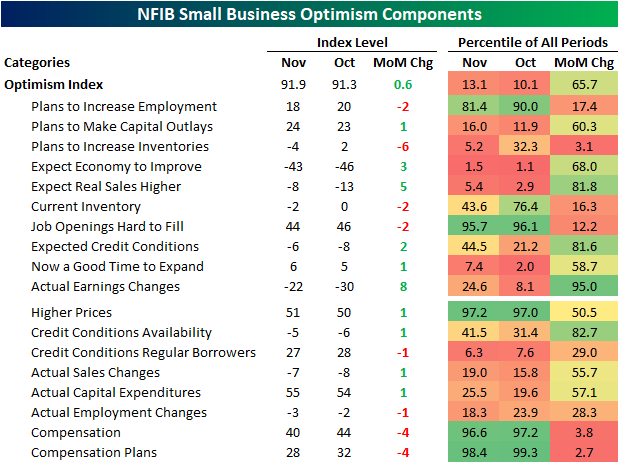

The National Federation of Independent Business (NFIB) released its November read on small business sentiment this morning with the report showing a modest uptick in optimism. The headline index rose from 91.3 to 91.9, but as shown below, that remains at historically low levels.

Across the individual categories of the survey, breadth was mixed with six of the ten inputs to the optimism index moving higher month over month. Multiple sub-indices sit in the bottom decile of their historical ranges, while a handful of others, namely those centered around employment and inflation, are more elevated.

One index that has been well below historical norms has been the outlook for general business conditions (top left chart below). That index plummeted since the fall of 2020 (likely in large part thanks to political sensitivities of this survey), and the rebound over the past few months hasn’t been enough to bring it back up to pre-pandemic record lows. Alongside that rebound, there has been only a very minor jump higher in the share of respondents reporting now as a good time to expand.

As we noted in today’s Morning Lineup, employment metrics in aggregate significantly slowed last month. Hiring plans fell 2 points down to 18; the weakest reading since February 2021. On net, there have also been more firms reporting declines than increases in employment. Given companies appear to be pulling back on hiring, the lowest share reported job openings are hard to fill since April 2021. Not only does it appear that firms are hiring less, but they are also raising compensation less. Both indices for compensation and compensation plans fell sharply in November.

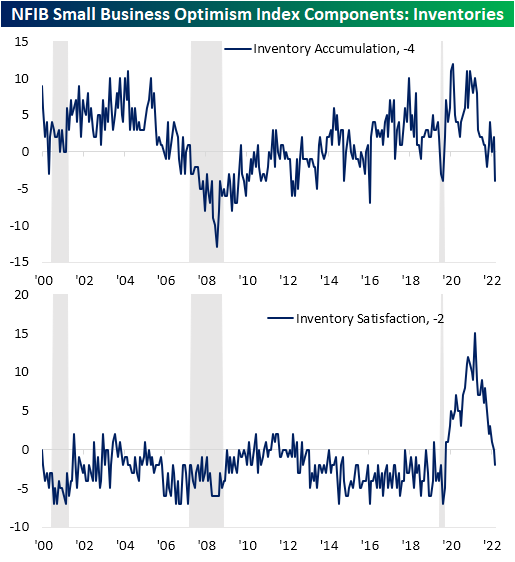

Inventories are yet another area of jarring declines last month. On net 4% more companies reported plans to decrease inventories in the next three to six months making for the lowest reading on inventory accumulation since the depths of the pandemic: April 2020. While there is the potential silver lining that the decline in the reading is a result of improvements in supply chain pressures, it is paired with obvious deterioration in demand. Given this, for the first time since the spring of 2020, a higher share of respondents are reporting their current inventory levels are too high versus too low. Click here to learn more about Bespoke’s premium stock market research service.