Feb 16, 2023

The S&P 500 hasn’t moved decisively in any direction over the past week, and as a result, sentiment saw little change. 34.1% of respondents to the weekly AAII sentiment survey reported as bullish this week, down from a high of 37.5% last week.

Bearish sentiment took from those bullish losses as the reading rose up to 28.8% from 25%. Even though that is a higher reading, it is still the only other reading below 30% since last March.

Additionally, the pickup in bearish sentiment was not enough to make bears outnumber bulls. As such, the bull-bear spread saw its first back-to-back positive readings since November 2021.

Although over a third of respondents reported as bullish, this week’s predominant sentiment level was neutral. 37.1% reported as such this week. That reading has now been above its historical average of 31.4% for seven straight weeks; the longest streak since January 2021.

Other sentiment surveys have likewise taken more optimistic tones lately despite a modest pullback in bullish sentiment this week. Factoring in the Investors Intelligence and NAAIM sentiment readings, our sentiment composite remains positive but is off from its short-term peak last week. Click here to learn more about Bespoke’s premium stock market research service.

Feb 16, 2023

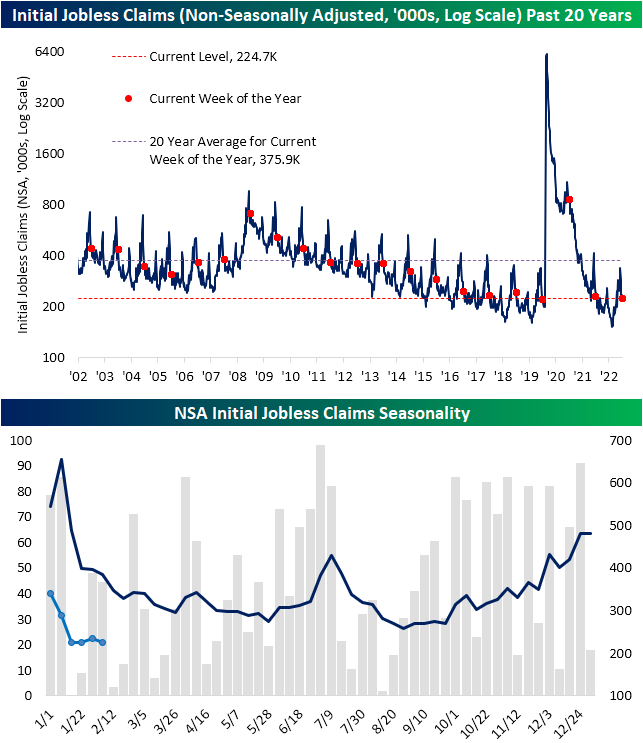

Jobless claims continue to impress in the new year. For the fifth week in a row, seasonally adjusted initial claims have come in with a sub-200K reading. That is the longest streak since a 10 week long stretch ending in April of last year. Although claims have remained at a healthy level, there hasn’t been much in the way of improvement over the last few weeks with claims yet to move below the 183K low at the end of January.

On a non-seasonally adjusted basis, the first few months of the year tends to see a sharp unwind in claims, albeit with some moderation during the current week of the year which is being observed currently with fairly flat readings in claims over the past few weeks. At current levels, this year’s reading was roughly in line with the comparable week of the past several years with the exception of the much more elevated reading in 2021.

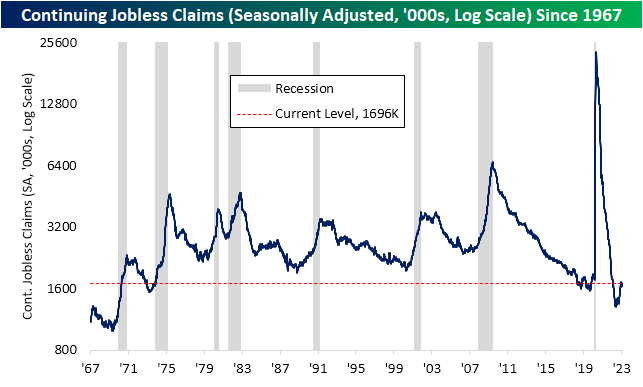

While not to say the reading is at unhealthy levels, continuing claims have not been as strong as initial claims. Claims have risen in each of the past two weeks, totaling 1.696 million in the most recent print. That is the highest level since the week of December 24th. Overall, both initial and continuing claims continue to show healthy readings without much in the way of rapid improvement or deterioration. Click here to learn more about Bespoke’s premium stock market research service.

Feb 15, 2023

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a look at the CBO’s update of fiscal policy forecasts (page 1) followed by a rundown of tonight’s earning reports (pages 2 and 3). We then dive into apparent seasonal adjustment issues in the retail sales report (page 4) before turning to the latest hard manufacturing data (page 5). After a recap of today’s 20 year bond auction (page 6) we dive into some of the oddities of the latest EIA data (pages 7 and 8). We finish with a look at homebuilder stocks after big jumps in homebuilder sentiment as we saw today (page 9).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Feb 15, 2023

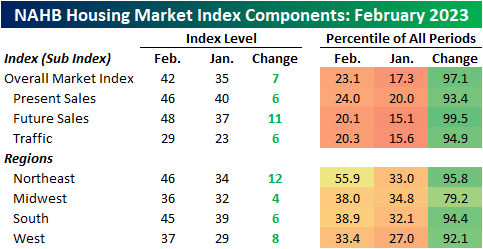

Wednesday’s release of homebuilder sentiment from the NAHB showed a significant rebound in sentiment as the headline reading has risen in back-to-back months from the low of 31 in December up to 42 this month. While that is not a screaming endorsement of strength from homebuilders (in the past decade, the only times the index was this low was the past few months and the start of the pandemic), it does mark an improvement in sentiment that is consistent with the recent turnaround in mortgage rates and the rise in weekly mortgage applications.

While sentiment has risen in back-to-back months, the moves from January to February were historic across the report. The only index to not experience a monthly move that ranks in the top decile of all periods was the Midwest. Future Sales was the most impressive with its 11-point jump tied with November 1988 for the second largest month-over-month increase on record.

As for the headline index, the 7-point increase was the largest increase since the months of May, June and July 2020 when sentiment began to recover from the pandemic plummet. Prior to 2020, June 2013 was the last time sentiment has risen by as much. Click here to learn more about Bespoke’s premium stock market research service.