Mar 13, 2023

Log-in here if you’re a member with access to the Closer.

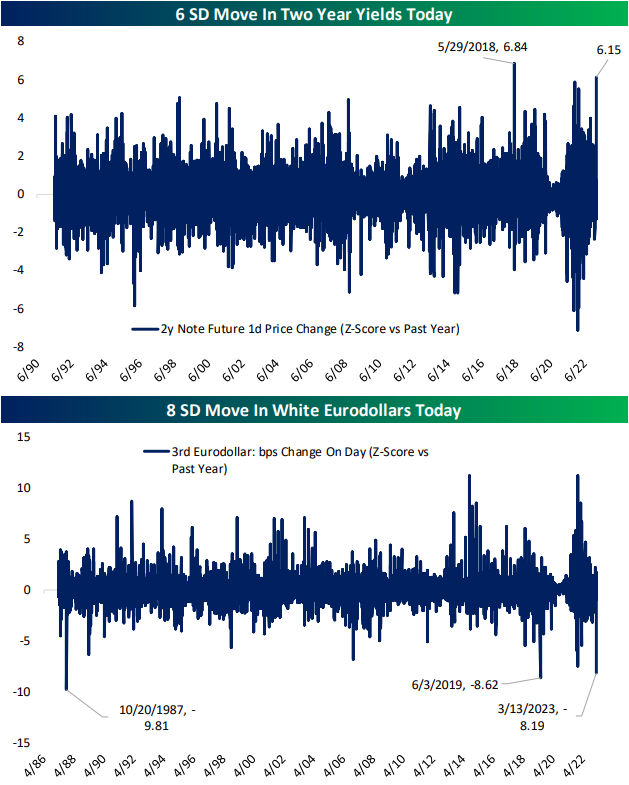

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a quick update on the banking situation (page 1) followed by a rundown of the historical superlatives for the moves in rates today (pages 2 and 3). Afterward, we dive into the NY Fed’s Consumer Expectations Survey (pages 4 and 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Mar 13, 2023

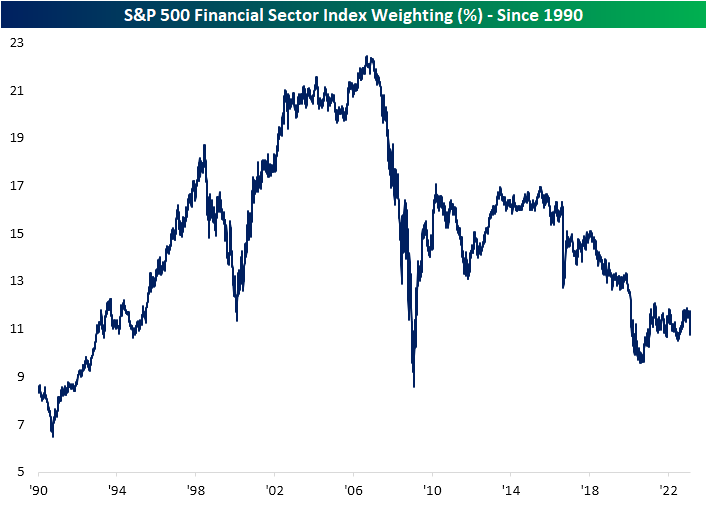

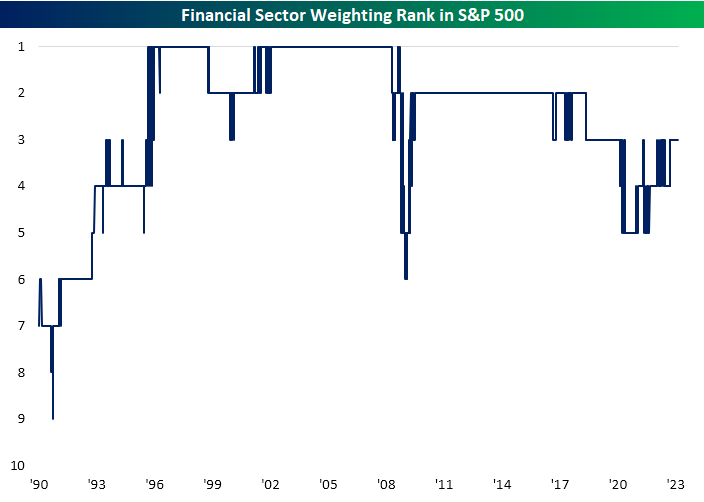

At its YTD high back on February 7th, the S&P Financial sector ETF (XLF) was up more than 8% on the year. Since that high, the sector has fallen more than 13% and is now down more than 6% YTD.

With systemic risk in the Financial system making front-page headlines again, we checked in on the sector’s weighting in the S&P 500 to see how it compares to where things stood back in the mid-2000s ahead of the Financial Crisis. Below is a look at the Financial sector’s weighting in the S&P going back to 1990. As of this writing, the Financial sector has a weighting of 10.73% in the S&P. That’s down a full percentage point from where it was at the end of February.

What’s interesting to note is how much smaller the sector is today compared to its weighting back in early 2006 when we were on the cusp of the Financial Crisis. At its peak in early 2006, the sector’s weight in the S&P had ballooned to 22.4%, which made it the largest sector of the S&P at the time. When the Financial sector, which is a sector meant to service the rest of the economy becomes the largest sector, something’s off! Of course, the Financial Crisis following the bursting of the housing bubble of the mid-2000s corrected this problem, as the Financial sector’s weighting fell from north of 22% down to south of 9% when the bottom was finally put in back in early 2009. During this latest bout of issues for Financials, the sector is still big enough to be the third largest sector in the S&P behind Tech and Health Care, but it’s not nearly as “weighty” as it was before the Financial Crisis, and its weighting has actually been trending lower for the last 7-8 years. Click here to learn more about Bespoke’s premium stock market research service.

Mar 13, 2023

The month of March is nearly halfway through and volatility has begun to pick up. Whereas the S&P 500 was up around 2% month to date as of this time last week, currently the index is down over 2.5%. As shown below, since the end of WWII March ranks in the middle of the pack with regards to the average spread between its Intra month high and low (on a closing basis). That compares with months like October—the most volatile of the year—which has averaged an Intra month range of just under 8%.

Although historically March might not be the most volatile month, in recent years that Intra month volatility has kicked up. In the chart below we show the spread between March’s Intra month highs and lows for each year since the end of WWII. Over time, there has consistently been some ebb and flow in this reading with some outlier years in particularly volatile times like the late 1990s and early 2000s and then of course 2020. October has historically been known as a month for market turnarounds, but March has become increasingly active on that front as well. Click here to learn more about Bespoke’s premium stock market research service.