Nasdaq Leaves the S&P in the Dust

Looking at the major US index ETF screen of our Trend Analyzer shows just how disconnected the Nasdaq 100 (QQQ) has become from other major index ETFs recently. As shown below, as of Friday’s close, QQQ actually finished in overbought territory (over 1 standard above its 50-DMA) whereas many other major index ETFs were oversold, some of those to an extreme degree. On a year to date basis, the Nasdaq 100 (QQQ) has rallied more than 14% compared to low single digit gains or losses for the rest of the pack.

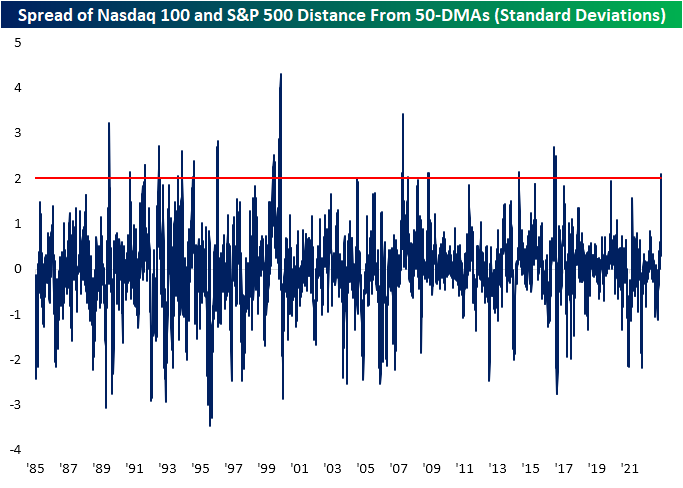

Historically, the major indices, namely the S&P 500 and Nasdaq, tend to trade at similar overbought and oversold levels. In the chart below we show the Nasdaq 100 and S&P 500’s distance from their 50-DMAs (expressed in standard deviations) over the past five years. As shown, typically the two large cap indices have seen similar albeit not identical readings. That is until the past few weeks in which the two have diverged more significantly.

On Friday there was more than 2 standard deviations between the Nasdaq’s overbought 50-DMA spread and the S&P 500’s oversold spread. As shown in the chart below, that surpassed recent highs in the spread like the spring of 2020 to set the highest reading since October 2016.

Going back to 1985, the spread between the Nasdaq and S&P 500 50-DMA spreads diverging to such a degree is not without precedent, but it is also not exactly common. Friday marked the 16th time that spread eclipsed 2 standard deviations for the first time in at least 3 months. Relative to those prior instances, the current overbought and oversold readings in both the S&P 500 and Nasdaq are relatively middling. However, only the instance in early 2000 similarly saw the Nasdaq technically overbought (trading at least a standard deviation above its 50-DMA) while the S&P 500 was simultaneously oversold (at least one standard deviation below its 50-DMA). Click here to learn more about Bespoke’s premium stock market research service.

Daily Sector Snapshot — 3/17/23

This content is for members onlyBespoke’s Crypto Report — 3/17/23

This content is for members onlyThe Closer – Hiking Anyways, Big Discount Window Borrowing – 3/16/23

Log-in here if you’re a member with access to the Closer.

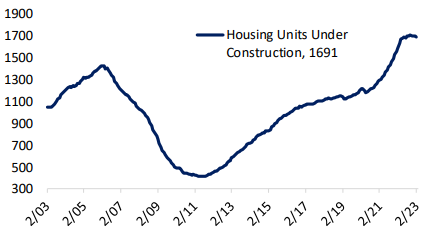

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with commentary on the ECB’s hike and the responding move in short term rates (page 1). We then dive into First Republic’s (FRC) balance sheet (page 2). Next, we show take note on the S&P 500’s big intraday reversal (page 3). Switching over to macro data, we then update our Five Fed Manufacturing Composite (page 4) followed by trade prices (page 5) and residential construction figures (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!