The Closer – Recession Pricing On Recessionary Data, JOLTS, LMI – 5/2/23

Log-in here if you’re a member with access to the Closer.

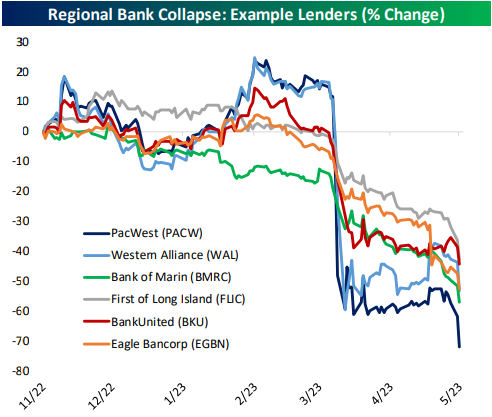

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, after earnings recaps (page 1), we check on the collapse in regional banks, the rise in credit spreads, and drop in yields and energy prices (page 2). Turning to macro data, we recap today’s JOLTS figures (pages 3 and 4) and finish with a look at the latest logistics data (pages 5 – 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!