Daily Sector Snapshot — 6/2/23

This content is for members onlyThe Closer – Small Caps Left in the Dust, PMI Update, Construction Boom – 6/1/23

Log-in here if you’re a member with access to the Closer.

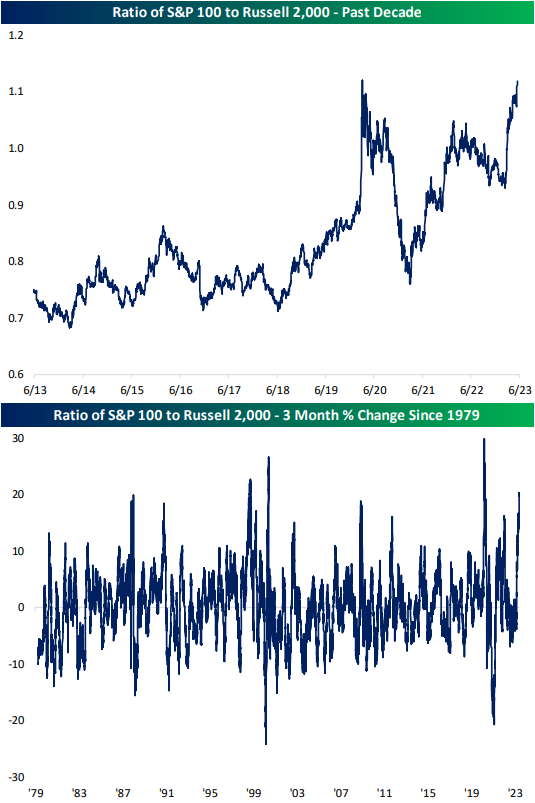

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at surge in the ratio of large cap to small cap stocks (page 1) followed by a dive into the latest macro data including nonfarm productivity & costs (page 2), construction spending (page 3), PMIs (page 4), and oil inventories (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!