Feb 9, 2026

Log-in here if you’re a member with access to the Closer.

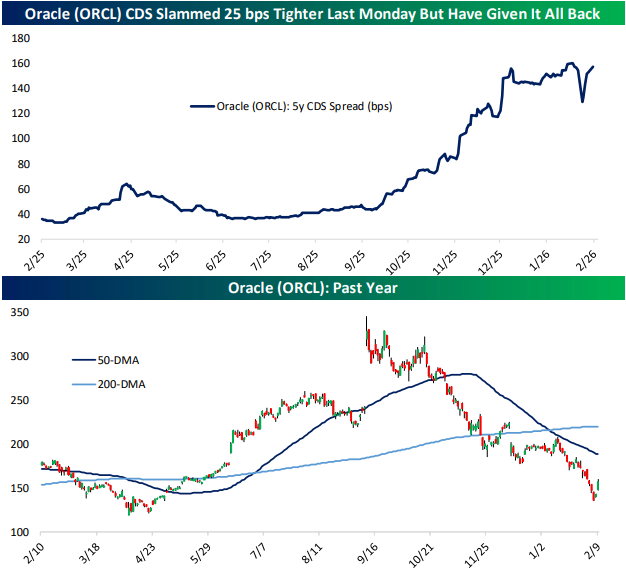

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a look at the sale of $20bn of debt from Alphabet (GOOGL) in addition to an update on Oracle (ORCL) credit spreads (page 1). Next up, we show the bounce in AI driven names (page 2). We then recap the latest findings of the New York Fed’s Survey of Consumer Expectations (pages 3 and 4) before capping off with a review of the latest positioning data (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Feb 9, 2026

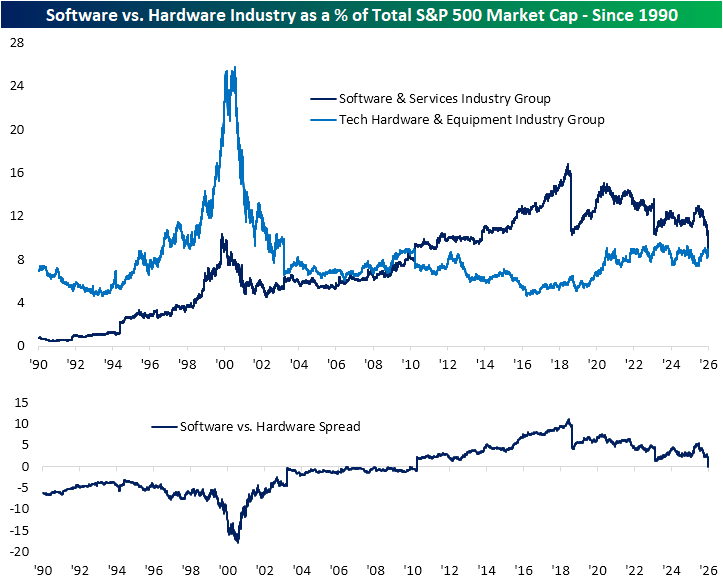

In the past couple of weeks, we have repeatedly highlighted the weakness in the software stocks. Fears that AI will pose a significant threat to the sector have caused large losses in terms of both price and weighting. In the charts below, we show the industry’s weighting in the S&P 500 versus other industries within the Tech sector. Last Thursday, the Software and Services industry saw its market cap as a share of total S&P 500 market cap fall below 9% for the first time since July 24, 2011. A significant portion of that drop has come from a dramatic move over the past several months; however, that is also in the context of a longer-term drawdown since the peak weighting in the summer of 2018, shortly before a reclassification that shifted several large-cap Tech names into other sectors.

The recent declines also put the software industry’s weighting on par with one of its peers in the Tech sector: the Tech Hardware and Equipment industry. In fact, at the low last Thursday, Software saw its weighting in the S&P 500 fall below that of Tech Hardware and Equipment for the first time since April 30, 2010. Whereas there have been steadier trends in software weighting over the long run, Hardware and Equipment has seen a relatively stable range of readings in the mid to high single digits since the early 2000s. That followed extremely elevated weights that crossed into the mid-20% range during the height of the Dot Com era. Fast forward back to today, even with the lower weighting in Software recently, Tech hardware hasn’t been picking up much.

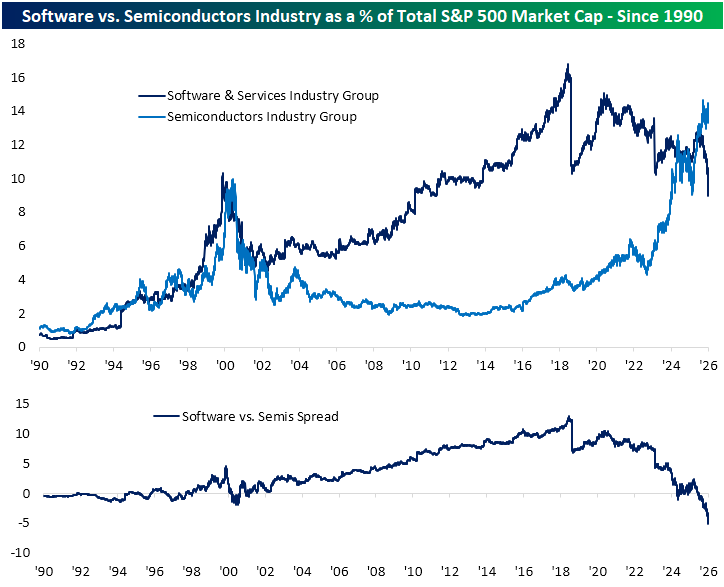

The third and final industry that comprises the Tech sector is Semiconductors, and its weight trend is the polar opposite. This is a group that has been an absolute star of the show since AI came to the mainstream in late 2022, and as a result, it is now hovering around a record share of the S&P 500’s market cap. Today, its weight is up to 14.3%, which is again still a far cry from the Tech Hardware and Equipment Industry over a quarter century ago. That also leaves software in the dust as there is now a record 5 percentage-point difference in the weightings of the two industry groups.

Feb 5, 2026

Log-in here if you’re a member with access to the Closer.

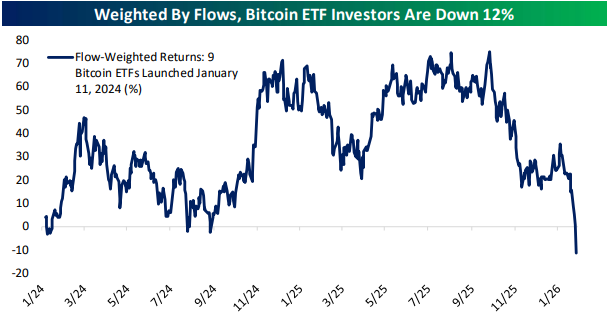

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a look into the crypto crash including some insights into how severe crypto ETF losses have gotten (pages 1 and 2). We also review the pain in the AI trade and massive outperformance of value versus growth (page 3). Afterward, we switch to economic data including the latest JOLTS release (pages 4 and 5) and jobless claims (page 6). Following a review of tonight’s earnings (page 7), we close out with an update on housing data (pages 8 and 9).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Feb 5, 2026

As we discussed in today’s Chart of the Day, the recent wave of selling hitting the market has been thematic. The AI trade has taken its lumps, and crypto stocks have sold off sharply in tow. For the latter group, that comes as crypto itself is plummeting. As shown below, Bitcoin rose to records in the $120K range throughout the summer and into this past fall. However, in the past several days, it has reached 52-week lows, collapsing into the $67K range today. For as volatile an instrument as Bitcoin is, 52-week lows have been relatively hard to come by. In the past decade, the only other examples of 52-week lows occurred in the fall of 2018, the spring of 2022, and November 2022.

As shown in the second chart below, those forays into 52-week lows have usually occurred closer to the end of major drawdowns rather than at the start of longer-term sell-offs. Further, this current sell-off is now right near the size of the historical average drawdown from all-time highs (46% today versus an average of 44.2% since 2011). Finally, we would note that although it’s an average-sized drawdown as of now, these latest 52-week lows have arrived when Bitcoin was in much less of a severe decline than previous examples.