Mar 5, 2026

Log-in here if you’re a member with access to the Closer.

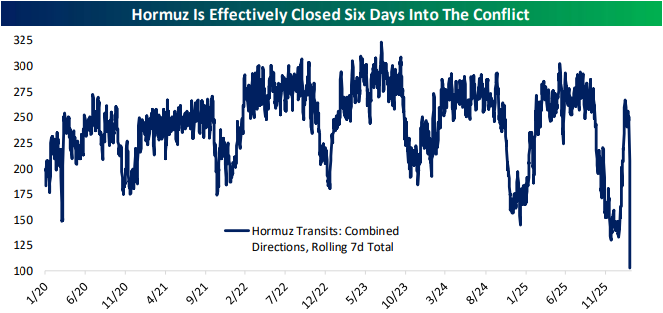

- Front month crude oil is setting up for a golden cross; a technical pattern that has historically played out to be less bullish than its reputation implies.

- The closure of Hormuz has resulted in extreme upside skew in options markets for crude oil.

- Labor productivity received material upward revisions for the past six quarters.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Mar 4, 2026

Log-in here if you’re a member with access to the Closer.

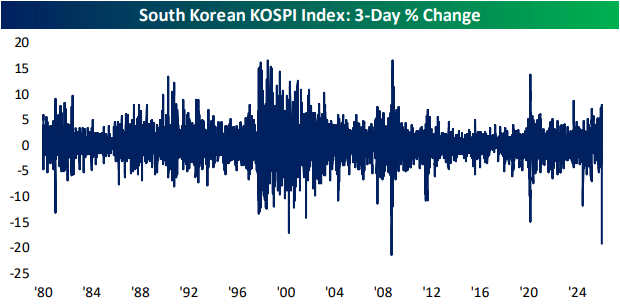

- Korean stocks have fallen close to 20% in the past three days; one of the largest declines on record.

- The Beige Book has seen a drop off in the number of mentions of tariffs, uncertainty, and layoffs.

- The situation in Iran has sent diesel prices exploding higher when trucking per mile prices are already rising rapidly.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Mar 3, 2026

Log-in here if you’re a member with access to the Closer.

- US equity leverage is currently modest at 0.8x, but bond markets are showing elevated leverage levels.

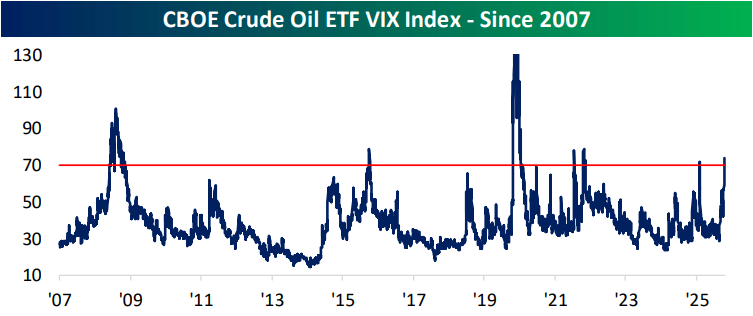

- Volatility is rising across assets with crude oil being the most pronounced example as the oil VIX is now at the highest level since the onset of the Russia-Ukraine war.

- The Logistics Managers Index showed significant expansion in transportation prices.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!