Feb 26, 2026

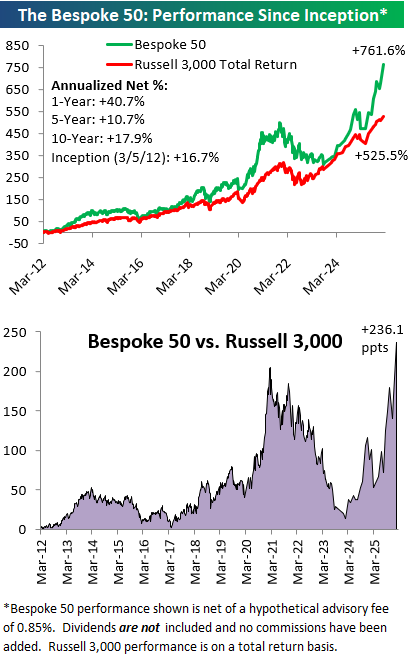

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. There were 8 changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. With Bespoke Premium, you’ll receive a number of daily market updates from us along with our weekly newsletter and a portion of our investor tools. With Bespoke Institutional, you’ll receive everything that’s included with Premium plus additional daily macro analysis and more stock-specific research.

To see all 50 stocks that currently make up the Bespoke 50, simply start a two-week trial to Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated monthly on Thursdays unless otherwise noted. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning after publication. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Feb 26, 2026

NVIDIA (NVDA) is down 5% today following yet another earnings triple play after the close yesterday. Barring a massive turnaround in the last hour of trading, this will be the seventh straight quarter where NVDA shares fell from the open to the close of trading on the day after it reports earnings.

Below is a snapshot of NVDA quarterly earnings versus estimates since ChatGPT’s release at the end of 2022. Out of 13 total quarterly reports, NVDA has reported ten triple plays (beat EPS, beat sales, raised guidance).

In its first six earnings reports following the release of ChatGPT, NVDA shares averaged a one-day gain of 10% on its earnings reaction day. Following its last seven reports, though, shares have averaged a decline of 3% for an overall average of 3.2%.

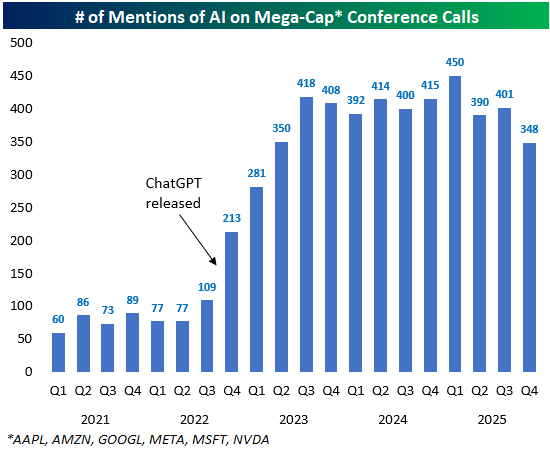

Now that NVDA has reported and completed its conference call, we can update our chart of “AI” mentions from the mega-cap hyperscalers this earnings season. Across the conference calls of Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL), Meta (META), Microsoft (MSFT), and NVIDIA (NVDA), “AI” was mentioned 348 times this quarter. As shown below, that’s down quite a bit from the 401 “AI” mentions last quarter, and it’s 102 fewer than the peak “AI” reached during the Q1 2025 earnings season.

Below is a breakdown of “AI” mentions by stock going back to 2001.

This quarter, Amazon (AMZN) and Apple (AAPL) were the only two that mentioned “AI” more on conference calls, with AMZN mentioning it a record 61 times.

META mentioned AI just 45 times, the lowest since Q4 2023, while NVDA’s 82 mentions was the lowest since the last earnings season before ChatGPT’s release!

Feb 24, 2026

Large-cap US equity indices made their last all-time highs at the end of January on 1/28, which was also the last Fed Day. As of 2/23, the S&P 500 was down about 2% since 1/28, while the mega-cap heavy Nasdaq 100 was down 5%.

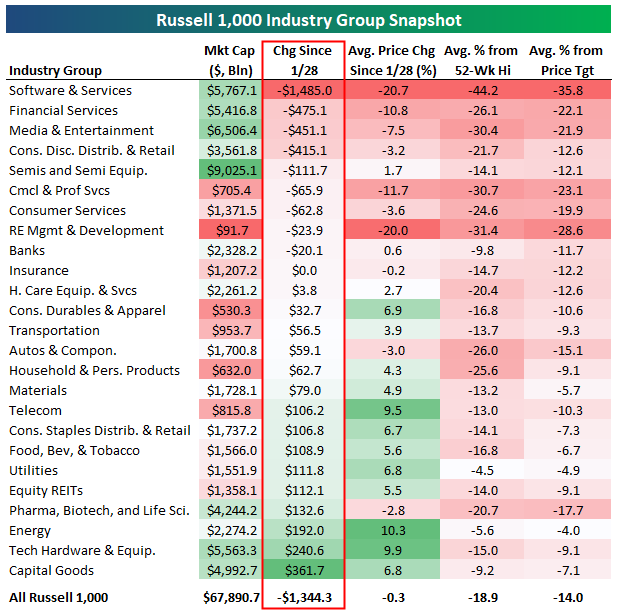

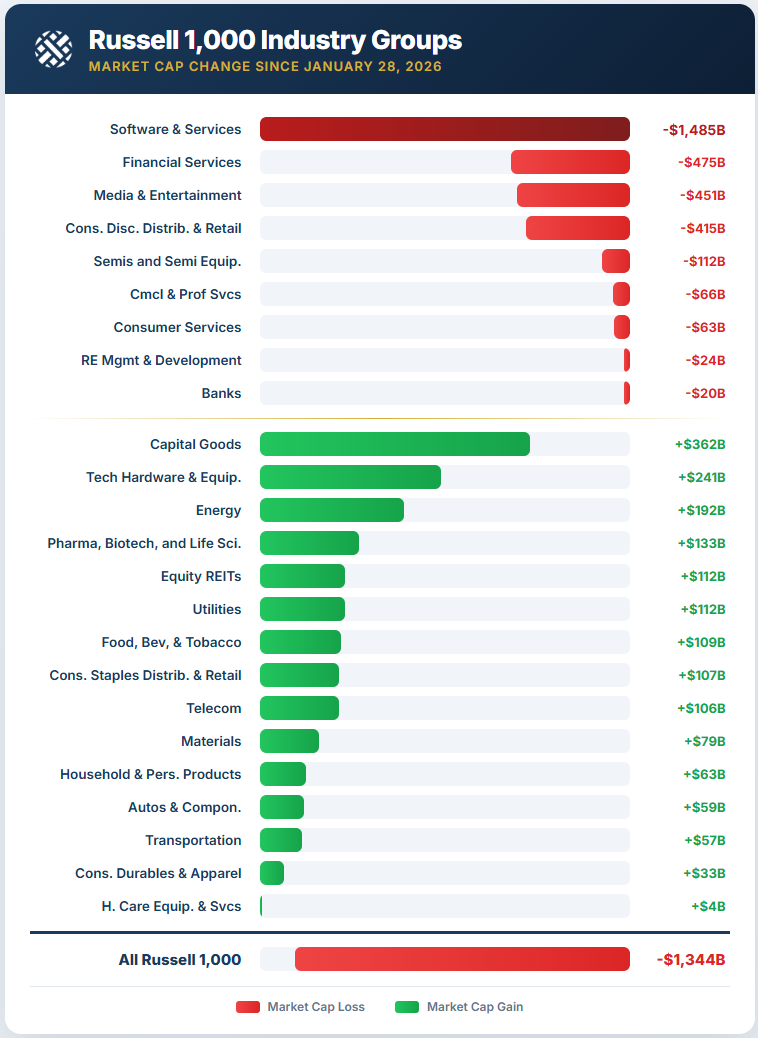

Within the broader large-cap Russell 1,000 (R1K), the average stock in the index is down just 0.3% since 1/28. But we’ve seen the market lose about $1.34 trillion in market cap over this time frame. Most of that can be chalked up to the “AI Doom” trade, where groups like Software & Services and Financial Services have been pummeled because of the threat that AI will make them obsolete.

As shown below, Software has seen its market cap fall by nearly $1.5 trillion since 1/28, while Financial Services has fallen nearly $500 billion. Media & Entertainment has also seen a $451 billion drop, followed by Consumer Discretionary Distribution & Retail with a decline of $415 billion.

Combined, these four groups have lost about $2.8 trillion in value.

Below are a series of graphics highlighting recent industry group performance.

Some of the groups that have seen the biggest gains in market cap over the same time frame include Capital Goods, Tech Hardware, Energy, and Pharma/Biotech.

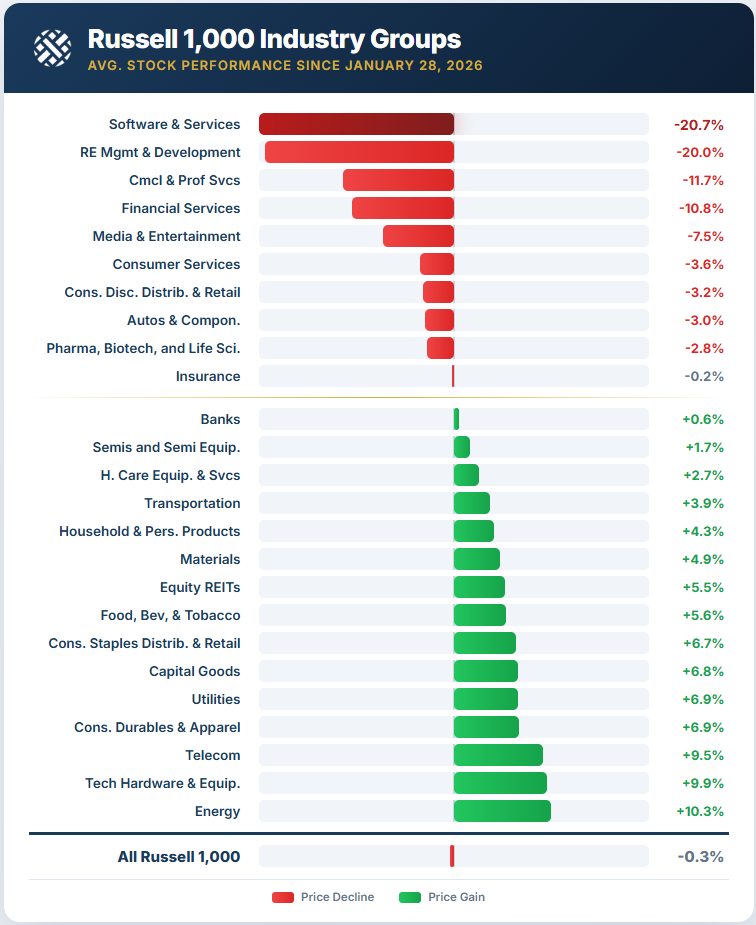

Below is a look at the average stock’s percentage change since 1/28 by industry group. Software and Real Estate Management & Development stocks have easily seen the biggest drops at -20%+.

Nine groups have averaged gains of more than 5%, however.

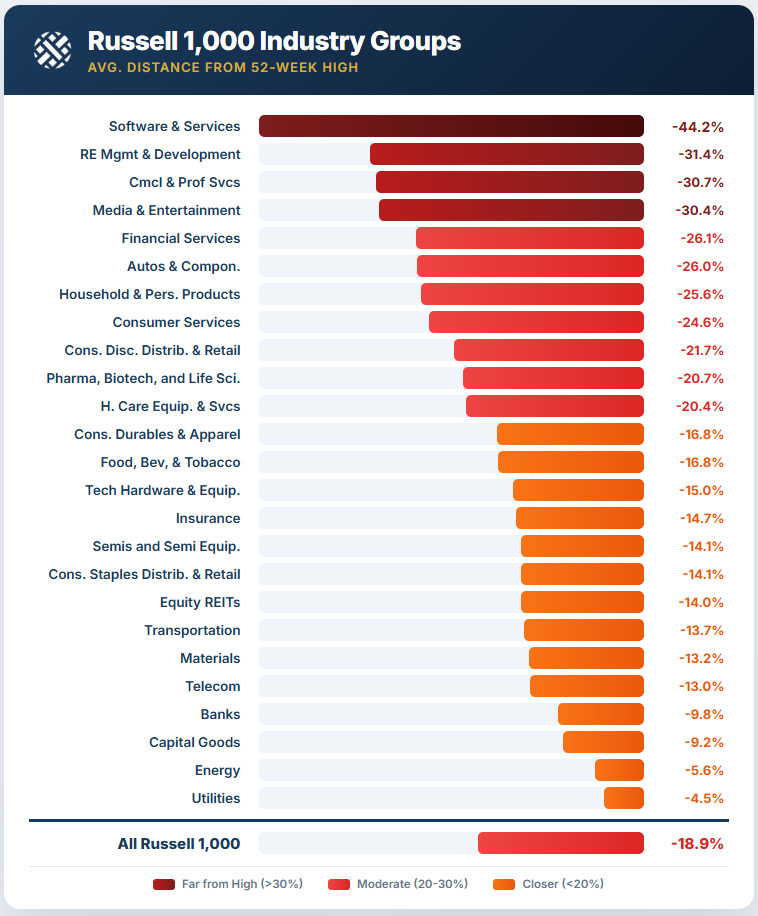

The average Russell 1,000 stock is currently about 19% below its 52-week high. Four groups are at -30%: Software, Real Estate Management & Development, Commercial & Professional Services, and Media & Entertainment. On the flip side, the average Utilities stock is less than 5% from its 52-week high.

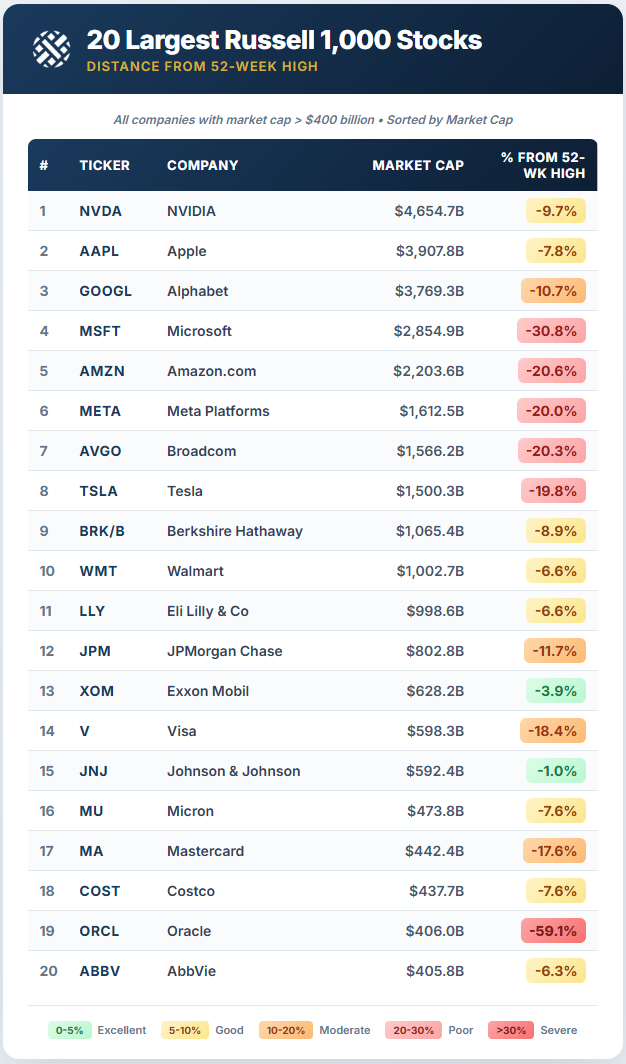

If you’re interested, below is a look at the twenty largest stocks in the Russell 1,000, along with each one’s current distance fromits 52-week high. Of the $1+ trillion companies, Microsoft (MSFT) is in the biggest drawdown at -30.8%, followed by Amazon (AMZN), Meta (META), Broadcom (AVGO), and Tesla (TSLA) – all around -20%. Oracle (ORCL) is the farthest from 52-week highs of the names listed at -59%, while Johnson & Johnson (JNJ) is the closest at just -1%.