Post-Iran Winners: Oil, Energy, and Israel

Equities around the world continue to take it on the chin this March, with month-to-date performance coinciding with the beginning of the start of the war in Iran over the last weekend of February.

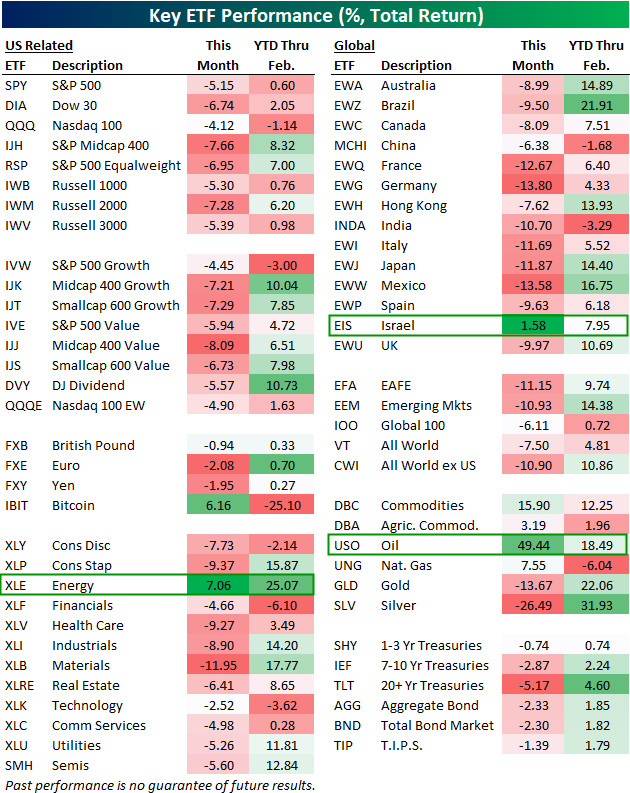

Below is a look at our asset class performance matrix featuring total returns for dozens of ETFs across domestic and international equities, sectors, currencies, commodities, and fixed income.

For each ETF, we show year-to-date performance through February along with performance so far in March.

ETFs across asset classes are bleeding red this month with the exception of a few: Bitcoin (IBIT), the Energy sector (XLE), oil (USO) and other energy/ag commodities, and Israel (EIS). Of these month-to-date winners, oil (USO), the agriculture commodities ETF (DBA), the Energy sector (XLE), and Israel (EIS) are the only ones that were also up year-to-date before the Iran war began.

On the downside, mid-caps and small-caps have been some of the hardest hit domestic index ETFs, with mid-cap value (IJJ) down the most at -8.1%.

Every sector ETF is down this month except Energy (XLE), with Materials (XLB) down the most at -12%.

Outside the US, country ETFs like France (EWQ), Germany (EWG), India (INDA), Italy (EWI), Japan (EWJ), and Mexico (EWW) are all down 10%+ since the war, while gold (GLD) and silver (SLV) have also gotten pummeled. Additionally, fixed income has not offered any safety due to inflation concerns brought about by the war. The 20+ Year Treasury ETF (TLT) is already down 5.2% since the bombings began.

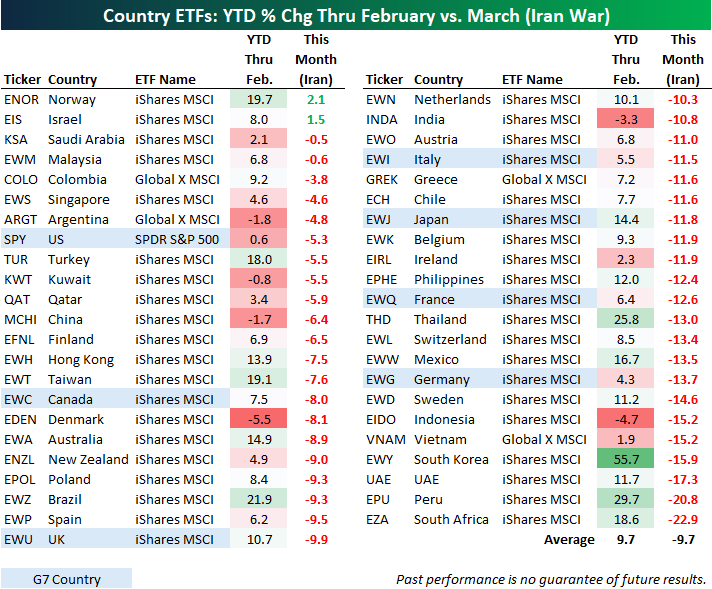

Below is a look at the recent performance of more than 40 country stock market ETFs traded on US exchanges.

On average, these country ETFs were up 9.7% through the first two months of 2026. Since the end of February, though, they’re down an average of 9.7%. Just a few weeks ago, it looked like 2026 was likely to be another year of outperformance for international markets. Now that there’s war in the Middle East and the Strait of Hormuz is unofficially closed for business, countries that heavily rely on energy imports are getting hit (with the exception of Israel). Along with Israel (EIS), Norway (ENOR) is the only other country ETF that’s positive this month. As a reminder, Norway is one of the few non-Middle Eastern countries that’s a net exporter of oil.

Six country ETFs are down 15%+ since the war began: Indonesia (EIDO), Vietnam (VNAM), South Korea (EWY), UAE (UAE), Peru (EPU), and South Africa (EZA).

Of the G7 countries, the US (SPY) is down the least with a decline of 5.3%, followed by Canada (EWC) — down 8%, and the UK (EWU) — down 9.9%.

Like this analysis? Become a Bespoke Premium member today using our March Madness special! Click below for details on how to sign up:

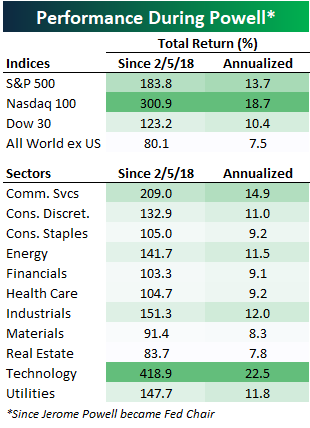

Powell Performance – Winners and Losers Since Fed Chair Began

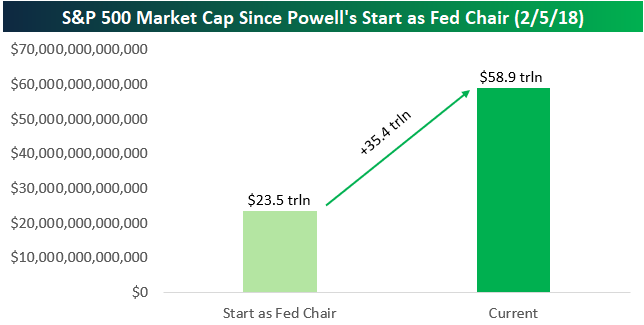

The S&P 500 fell 1.36% on Fed Chair Powell’s penultimate FOMC day on Wednesday (3/18/26). While a hallmark of Powell’s tenure as Chair has been the stock market’s tendency to trade sharply lower in afternoon trading on Fed Days, the market has also done very well over the entirety of his 8+ year term.

When Powell became Fed Chair in February 2018, the combined market cap of stocks in the S&P 500 was $23.5 trillion. That number has ballooned by $35.4 trillion up to $58.9 trillion today.

The S&P 500 has gained more than 180% since 2/5/18 when Powell became Chair, representing an annualized total return of 13.7%. The tech-heavy Nasdaq 100 has gained much more at 300.9% (18.7% ann.), while the Dow 30 is up 123%.

Compared to the rest of the world, Powell has kept US markets in a dominant position. The S&P has beaten the rest of the world by more than 100 percentage points since his time as Chair began.

Looking at sector performance, Technology has more than doubled the next-best sector (Communication Services) during Powell’s tenure. As shown above, Tech has returned 418% since Powell took over, while Materials and Real Estate are the only two sectors that haven’t at least doubled.

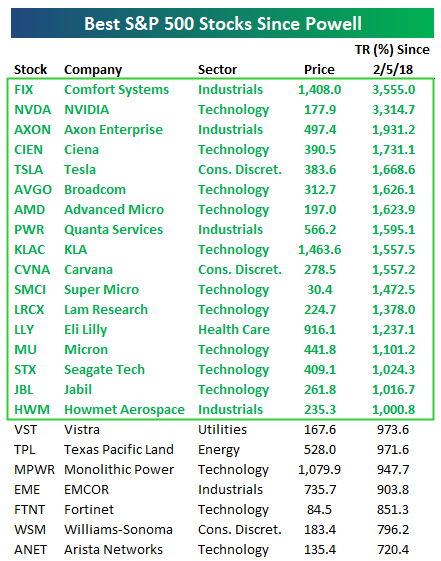

Of the current S&P 500 members that were trading back in early 2018 when Powell became Chair, 59% have gained at least 100% since then. There are nearly just as many S&P 500 stocks up 500%+ (39) since Powell’s tenure began as there are stocks that are down (45).

Below is a table showing the best-performing S&P 500 stocks since Powell became Chair, with the seventeen “10-baggers” highlighted in green.

You may have thought NVIDIA (NVDA) would be at the top of this list given its place as the largest company in the world right now, but a company that’s just over a tenth of NVDA’s size actually has it beat. Comfort Systems (FIX) — which builds out the mechanical, electrical, and plumbing systems for AI data centers and other infrastructure projects — is actually #1 when it comes to share-price performance under Powell. As shown, FIX is up 3,555% compared to a gain of 3,314% for NVDA.

Most of the names on the list of big winners since Powell became Chair are directly related to the AI Boom, but some that are not include Axon Enterprises (AXON) — which sells Tasers and police bodycam hardware and software, Carvana (CVNA) — which sells used cars, and Eli Lilly (LLY) — which sells weight-loss drugs and other pharmaceuticals.

Sign up for Bespoke’s Think BIG mailing list to receive an interesting market stat like this in your inbox a few times per week. Click here or on the image below to sign up. An email is all we need!

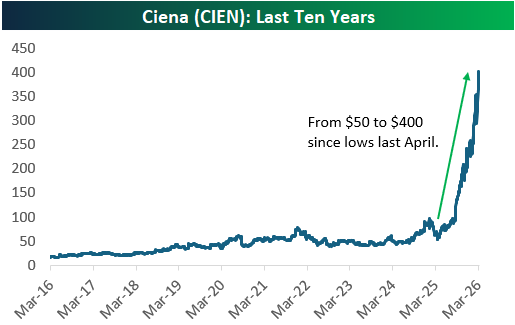

While there are seventeen “10-baggers” since Powell became Chair, not all of those stocks are in uptrends right now. Below are price charts for the six best performers in our table above. While Ciena (CIEN) and Comfort Systems (FIX) remain in strong uptrends, the other four have either traded sideways or lower over the last six months.

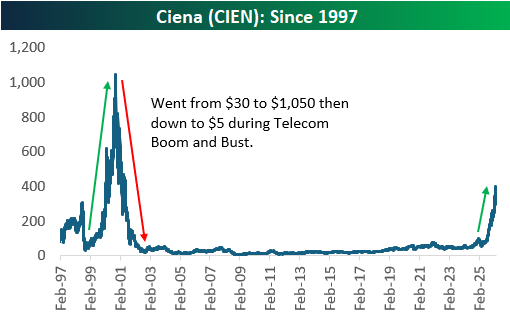

Of the six biggest winners under Powell, Ciena (CIEN) is the only one trading at record highs today. Its price action lately has been a sight to behold.

Last year at the tariff-tantrum lows, the stock was trading in the low-$50s. It’s currently trading above $400.

Ciena (CIEN) somewhat slid under the radar in the early years of the AI Boom, but over the last year or so, investors haven’t been able to get enough of it.

That’s because Ciena makes some of the most important networking gear for AI data centers (shown below). Every time a company makes a bigger, smarter LLM for consumption, they need more of Ciena’s gear to make that data work and move faster.

What’s even crazier about Ciena (CIEN) is that even though the stock is up nearly 1,000% in the last few years and 1,700% since Powell became Fed Chair, it still hasn’t gotten back to half of what it peaked at during the Dot Com Bubble of the late 1990s.

Just as Ciena is a key player in the AI infrastructure build-out right now, it was also a key player in the Internet/Telecom buildout of the late 1990s. After rallying from $30 to north of $1,000/share at its peak, shares plummeted to as low as $5 after the bubble burst in the early 2000s.

This should be a key reminder of how carried away investors can get during market manias, but it also shows that while the AI Boom indeed has a lot of hype, things were even crazier back in the late 90s.

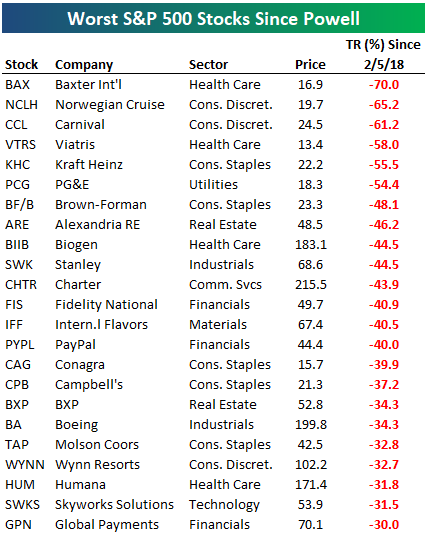

So far we’ve only discussed winners since Powell became Fed Chair, but below is a list of the S&P 500 stocks that have done the worst over his tenure. The names shown are the 23 stocks down at least 30% since 2/5/18, led by Baxter International (BAX) with a 70% drop.

Two cruise-lines rank 2nd and 3rd worst (Norwegian and Carnival) with declines of more than 60%, and another three stocks have been more than cut in half: Viatris (VTRS), Kraft Heinz (KHC), and PG&E (PCG). Other well-known names on this list of losers include Biogen (BIIB), PayPal (PYPL), Campbell’s (CPB), Boeing (BA), Molson Coors (TAP), and Wynn Resorts (WYNN).

Like this analysis? Become a Bespoke Premium member today using our March Madness special! Click below for details on how to sign up:

Bespoke Baskets Update – March 2026

This content is for members onlyPast the Ides of March

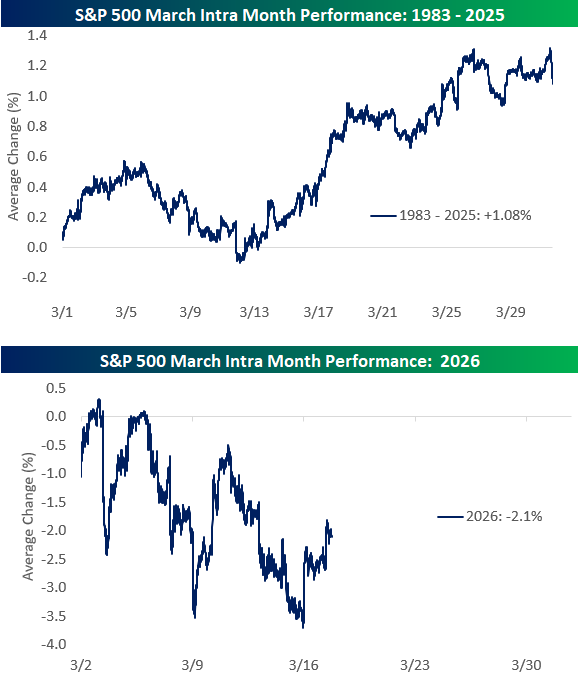

The S&P 500 fell more than 3% in the first half of March, but there’s reason to be more optimistic from a seasonal perspective. As we highlighted in this Chart of the Day for members at the start of the month, March gains have historically been back-end loaded.

The top chart below shows the S&P 500’s average path during the month of March since 1983. The second chart shows the S&P’s price action so far this March.

Historically, the market has traded relatively flat through the Ides of March and then picks up steam with gains in the back half of the month.

So far this week, we’ve seen the bulls get back to work with the S&P up more than 1% as of noon on Tuesday. We’ll see if the gains can hold and continue following the historical script with a strong finish to the month.

Sign up for Bespoke’s Think BIG mailing list to receive an interesting market stat like this in your inbox a few times per week. Click here or on the image below to sign up. An email is all we need!

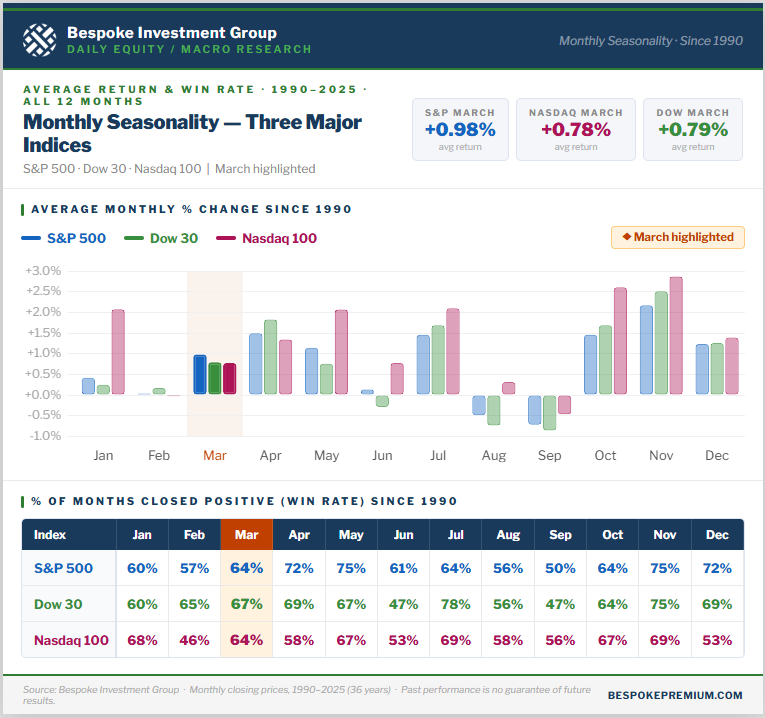

For more context on market seasonality, the graphic below was featured in our Chart of the Day for members back on March 2nd. It shows the average monthly percentage change for the S&P 500, Nasdaq 100, and Dow 30 since 1990.

While March has typically seen gains of just under 1% for all three indices, April has been an even better month over the years!

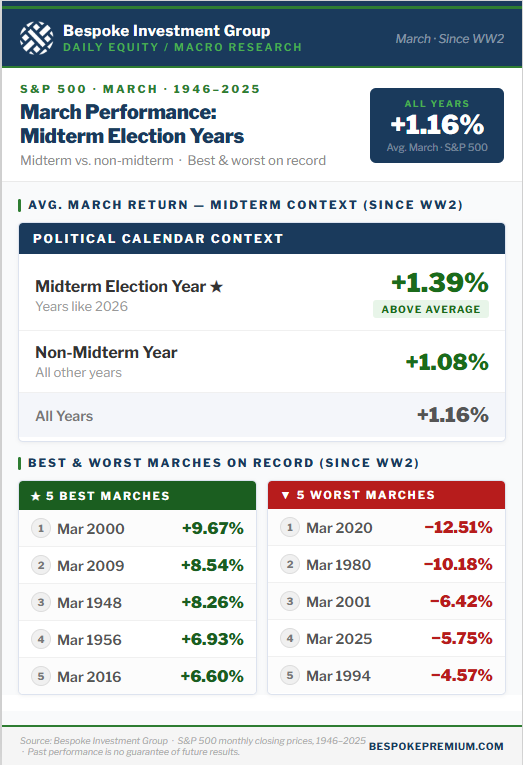

In addition to the graphic above, the one below shows how the market has performed in March during midterm election years like 2026 versus all other years. As shown, the market has historically done slightly better in March during midterm years with an average gain of 1.39% since WW2.

Like this analysis? Receive our Chart of the Day in your inbox each day by starting a Bespoke trial! Click below for details on how to sign up: