The Closer – Discount Names, Construction Collapse – 6/16/26

Log-in here if you’re a member with access to the Closer.

- AI picks and shovels stocks have begun to rebound over the past few days, spiking 10% since the lows last Wednesday.

- As massive AI and space stocks have come into focus recently., 63 S&P 500 members trade with much more attractive valuations.

- May residential construction saw a massive miss with Housing Starts down 15% MoM, largely due to multifamily categories.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 6/16/26

The Triple Play Report: 6/16/26

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

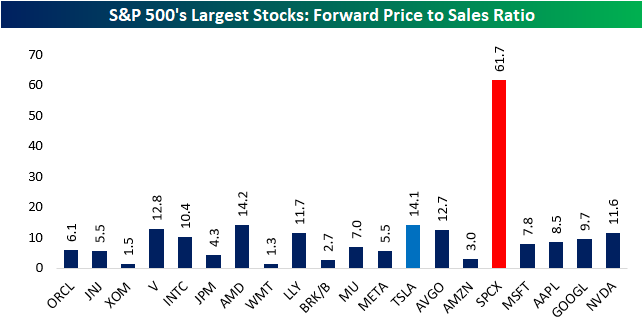

Mega-Cap Sales

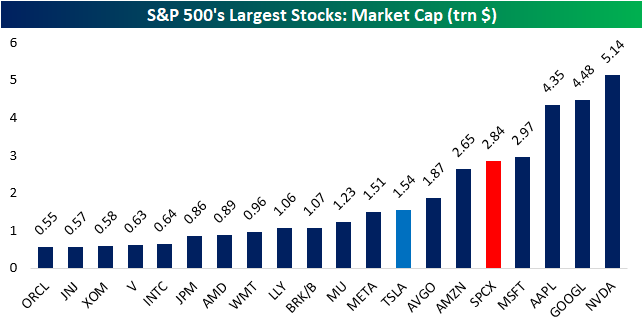

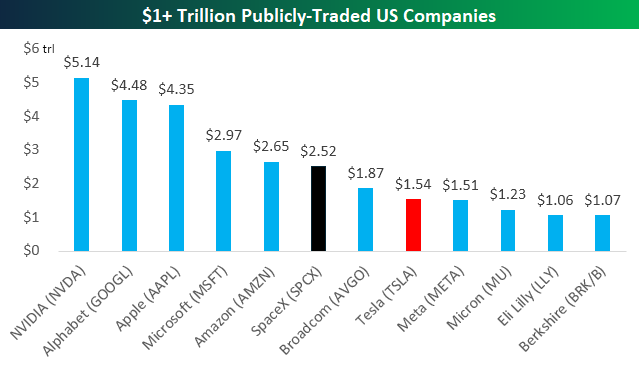

Since its record-breaking IPO last week, SpaceX (SPCX) has been the talk of the town, and understandably so, as the company debuted with a market cap above $1 trillion. As the company trades up another 11.5% as of this writing today, its market cap is now greater than $2.8 trillion. In the chart below, we put SPCX in the mix with the S&P 500’s largest companies, or those with market caps above $500 bn; as we have covered in depth previously here and here, SPCX is not yet a member of any major index, and the prospect of it joining the likes of the S&P 500 isn’t guaranteed despite the large market cap. Today’s move higher puts SPCX ahead of Elon Musk’s other company, Tesla (TSLA), by well over one trillion dollars, and it is now passing Amazon (AMZN) to rank as the fifth-largest US company behind Microsoft (MSFT).

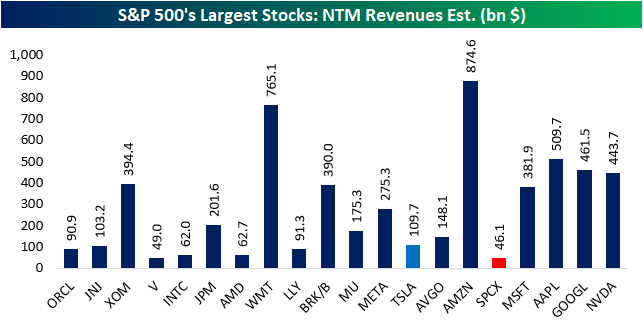

While SPCX has quickly rocketed to become one of the largest companies in the world in terms of market cap, the underlying fundamentals are an entirely different story. As shown below, relative to those other mega-caps, SPCX has miniscule revenue on a blended forward basis. Its $46 bn of estimated NTM revenues are more similar to the likes of Visa (V), which trades with a market cap of $580 bn, and is not even half of what Tesla (TSLA) is estimated to have for the coming year.

Given this, its valuation on a forward price-to-sales basis is astronomical relative to these mega-cap peers. The stock is trading with a 61.7 forward P/S ratio. That compares to an average P/S ratio for the other mega-caps shown of 7.91.

To expand out the universe of stocks, of the Russell 3,000 members, only 64 stocks have higher P/S ratios than SpaceX, and the two largest of those with market caps of $68.25 bn and $46 bn are Rocket Lab (RKLB) and Strategy (MSTR), respectively. In other words, SpaceX is expensive relative to a wide universe and mega-caps alike.

Of course, equities are inherently forward-looking. And to play devil’s advocate to the fact that the valuation is extremely lofty, the company possesses a unique moat of space exploration in addition to having other high-growth avenues of business, namely AI. The other side of the coin of the high valuation is that markets are pricing the potential for substantial growth.

Want more from Bespoke? You can start by joining our Think BIG mailing list, where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

Chart of the Day – Tied For the Biggest Miss on Record

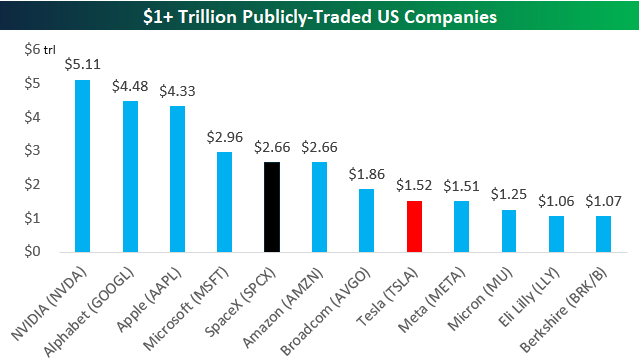

SpaceX (SPCX) As Big As Amazon (AMZN)?

Shares of SpaceX (SPCX) are up another 5% this morning in pre-market trading ahead of the 9:30 AM ET open.

Based on where it’s trading right now, SpaceX has a market cap of $2.66 trillion. That’s the exact same market cap as Amazon (AMZN), which went public just over 29 years ago in May 1997.

Should current levels hold, SPCX would be the fifth largest public company in the US behind NVIDIA (NVDA), Alphabet (GOOGL), Apple (AAPL), and Microsoft (MSFT). The gap between SPCX and MSFT is roughly $300 billion.

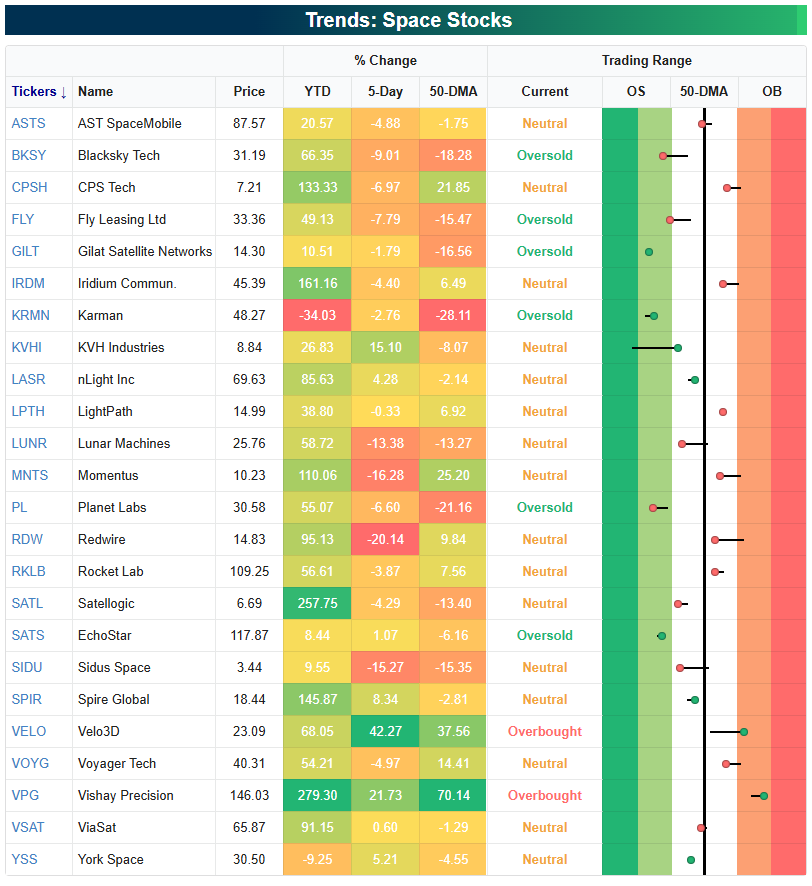

We’ve been monitoring space stocks for the past couple of months ahead of the SPCX IPO, and below is a basket of them using our Trend Analyzer tool (available to members here).

Late last week when SpaceX first began trading, the rest of the space-stock space sold off hard as investors rotated into SPCX. Some of them bounced back a little yesterday, but they’re collectively now just 1.3% above their 50-DMAs on average. Year-to-date, though, they’re still up an average of 75%, with six of the 24 stocks shown up 100%+.

Want more from Bespoke? You can start by joining our Think BIG mailing list, where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

Bespoke’s Morning Lineup – 6/16/26 – Oil Drawdown Reaches 30%

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Reality is wrong. Dreams are for the real.” – Tupac Shakur

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a strong start to the week on Monday, US futures are modestly higher this morning, with S&P 500 futures indicated 5 basis points higher, while the Nasdaq looks to gain 0.15%. Treasury yields are lower, with the 10-year yield falling below 4.45%, while crude oil falls another 3.8% to under $78 per barrel for WTI. Even Brent crude oil prices are on the verge of falling below $80, and these declines all point to lower gas prices ahead of the July 4th holiday. Gold prices are slightly higher, while Bitcoin is basically unchanged at $66,500.

Asian stocks put in a mixed performance overnight. The Nikkei barely finished higher after the BoJ hiked rates 25 bps, pushing rates to 1.0% for the first time since 1995. Chinese stocks finished lower, while India (+0.7%) and South Korea (2.1%) both finished higher. The weakness in Chinese stocks came as Retail Sales fell 0.6%, which was twice the expected decline, while Industrial Production was slightly better than expected.

European stocks are broadly higher this morning, with the STOXX 600 up 0.4%. Italy is leading the way higher with a gain of 1.2%, while Spain lags. Economic sentiment, as measured by ZEW, came in higher than expected for both Germany and the entire EU region.

It’s a quiet day for economic data this morning, as the only notable reports on the calendar were Building Permits and Housing Starts for May. Building Permits came in slightly weaker than expected at 1.413 million versus forecasts for 1.418 million. The big surprise, though, was in Housing Starts, which came in much weaker than expected at 1.177 million versus forecasts for 1.430 million. That’s the smallest monthly reading since May 2020, and one of the largest misses relative to expectations that we can remember.

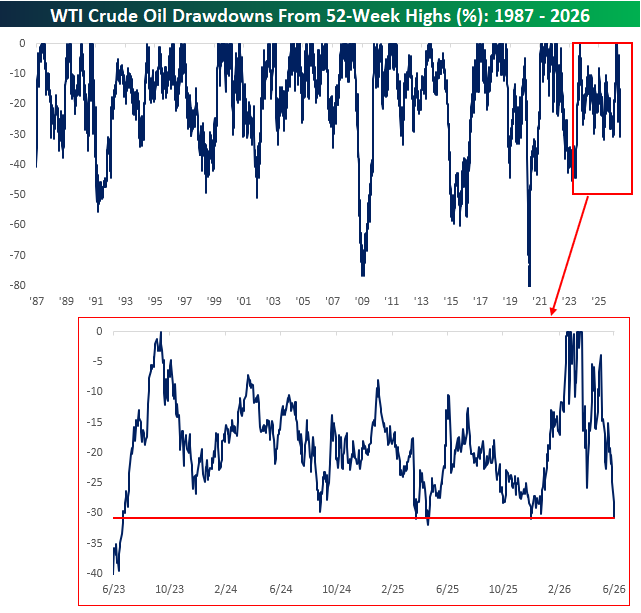

Lower oil prices have been a driver of higher stock prices over the last several days, and with crude oil trading down over 2% this morning, prices are down over 30% from their recent highs, putting the current drawdown from a 52-week high near the most extreme levels since mid-2023.

Shares of SpaceX (SPCX) are up over 5% again in the premarket but were up over 10% at one point overnight. With a market cap of $2.5 trillion as of yesterday’s close, the stock briefly had a market value in excess of Microsoft (MSFT) overnight, and it’s still right around the same levels or slightly above Amazon (AMZN). Obviously, only a small percentage of the company’s shares outstanding are available for trading, so the stock is incredibly volatile for a $2.5 trillion company, but these moves for such a large company are incredible.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – Industrial Strength, Grid in Growth Mode – 6/15/26

Log-in here if you’re a member with access to the Closer.

- Although it didn’t finish there, Industrials reached a record high today as capital goods have been a leading area.

- As Transportation stocks contribute to the strength in Industrials, freight volumes have begun to rebound although price pressures still remain.

- With data center and re-shored manufacturing load being added to the grid over recent years along with other factors, the structural backdrop of US grid load is firmly in growth mode.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!