Bespoke’s Consumer Pulse Report – March 2026

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

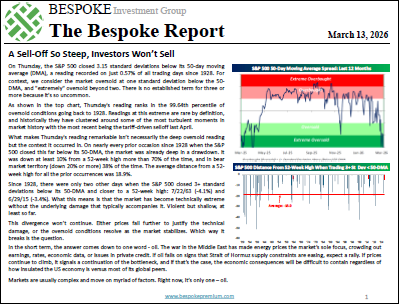

The Bespoke Report – 3/13/26 – A Sell-Off So Steep, Investors Won’t Sell

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. It was another eventful week in the market as we witnessed an extraordinary divergence between the S&P 500’s extreme oversold reading despite its relatively close proximity to all-time highs. This divergence won’t continue. Either prices fall further to justify the technical damage, or the oversold conditions resolve as the market stabilizes. Which way it breaks is the question. In this week’s Bespoke Report, we discuss the main factor(s) facing the market and put some of the recent moves into perspective.

Bespoke’s Morning Lineup – 3/13/26 – Tempting Fate

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Don’t let what you cannot do interfere with what you can do.” – John R. Wooden

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The market has one more day to salvage what’s been a negative week for stocks, and so far, it’s making a valiant effort. Futures on the S&P 500, Nasdaq, and Dow are all up 0.39%. With today being both Friday the 13th and the last day of trading into a weekend, it’s surprising to see equities catching a bid. Treasury yields are modestly lower, with the 10-year yield at 4.25%, and oil prices are down 2% to $93.50 per barrel. Gold prices are also pulling back, but Bitcoin is trading up close to 3% and above $72K.

Asian stocks ended what was already a down week on a negative note. The Nikkei was down over 1%, which took its weekly decline to over 3%, while China finished the week with a 0.7% decline, and India was down over 5%. Higher oil prices are a major pain point for the Asian economy, so the longer the Strait of Hormuz remains cut off, the more pressure it will put on these economies.

Equity performance has been more muted in Europe. The STOXX 600 is little changed for both the day and week, and no major index in the region is up or down more than 0.5% on the day. Industrial Production for January fell 1.5% versus expectations for an increase of 0.6%. Weaker growth, coupled with increasing inflationary pressures from rising energy prices, is the type of cooking markets would prefer not to see on the menu.

The economic calendar is jam-packed this morning with most of the reports (Personal Income, Personal Spending, GDP, PCE, Durable Goods) hitting the tape as we send this out, but at 10 AM Eastern, we’ll also get Michigan Confidence and JOLTS.

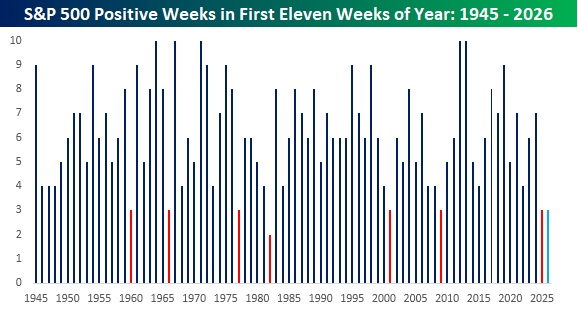

With the S&P 500 down 1% on the week heading into today, we’re on pace for the eighth negative week in the first eleven weeks of the year. With just three positive weeks, it’s been one of the weakest starts to a year for the S&P 500 in the post-WWII period. If the S&P 500 doesn’t rally more than 1% today, it will be the eighth year since 1945 that it has had three or less positive weeks to start a year. Ironically, last year also started weak, and while the market remained shaky through early April, it ended up being a good year. Before last year, the last time the year started out this inconsistently was in 2009, and the only year where there were fewer positive weeks to start a year was in 1982.

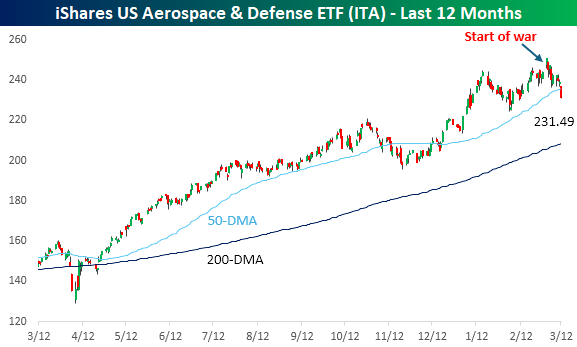

Two groups you would expect to benefit from the war in the Middle East are energy and defense stocks. Right out of the playbook, Energy stocks have rallied since the war broke out, but defense stocks have taken a sell-the-news response.

The chart below shows the performance of the iShares US Aerospace and Defense ETF (ITA) over the last year. While the ETF has surged over the last 12 months, it has struggled since the first missiles were fired. While ITA gapped up the Monday after markets reopened for trading after the war started, it’s been drifting lower ever since. Yesterday, it closed below its 50-DMA for the first time this year, and as Bloomberg noted in a news story overnight, the ETF had the largest outflow of assets in its history yesterday. Understandably, investors would take profits after the rally of the last year, but it’s interesting to see it follow the opposite path of Energy stocks.

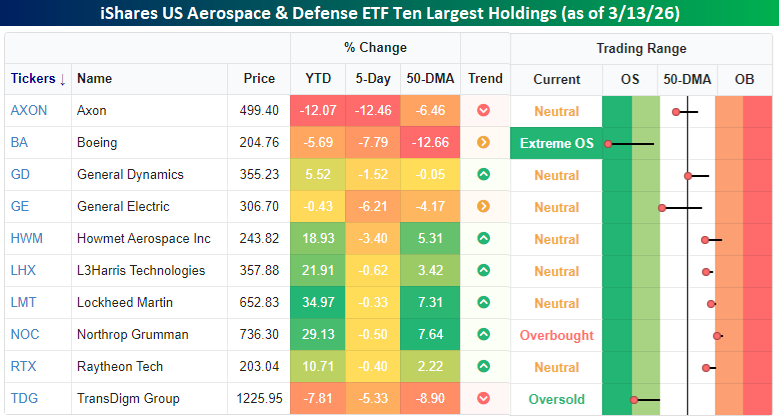

Below, we show the ten largest holdings in the ITA ETF and where each one closed relative to its trading range yesterday. Over the last week, all ten stocks are lower and some by a lot. General Electric (GE) and Boeing (BA) are the ETF’s two largest holdings, and both stocks are down more than 6% in the last week alone. For BA, that decline has taken it more than 12% below its 50-DMA and into ‘extreme’ oversold territory (2+ standard deviations below 50-DMA).

The Closer – Retail Teeter, Fertilizer, Trade – 3/12/26

Log-in here if you’re a member with access to the Closer.

- Retail flows and options volumes have moderated in the past year.

- US based fertilizer prices have now risen 29% MTD thanks to the closure of the Strait of Hormuz.

- The December 2026 Fed Funds rate implied by futures markets is now at the highest level since February of last year.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

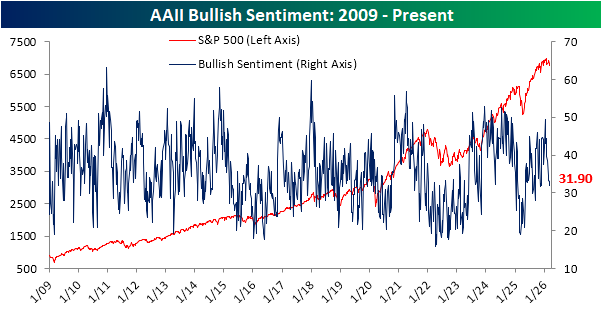

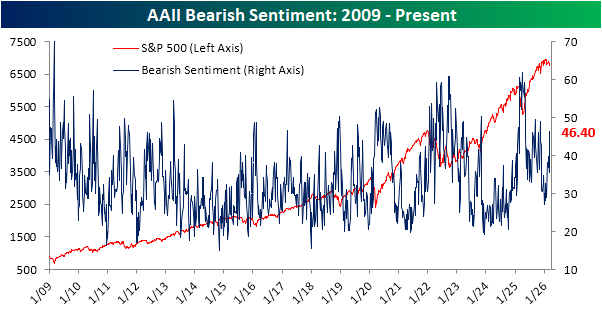

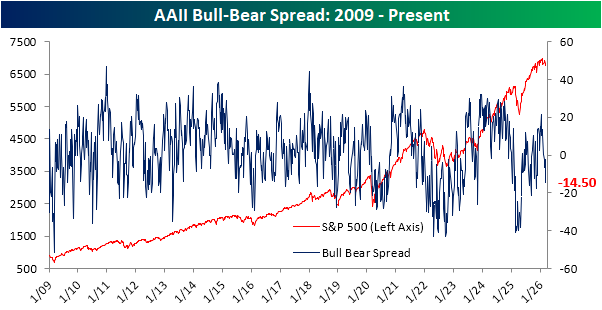

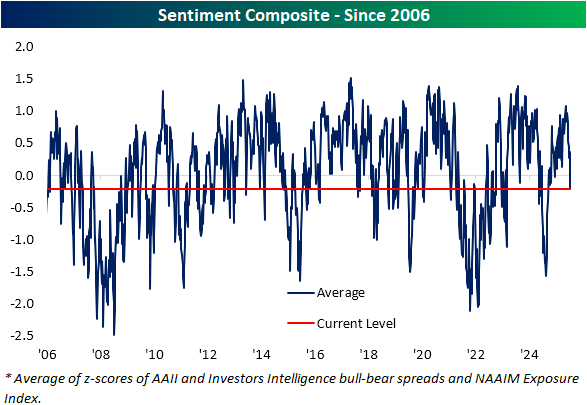

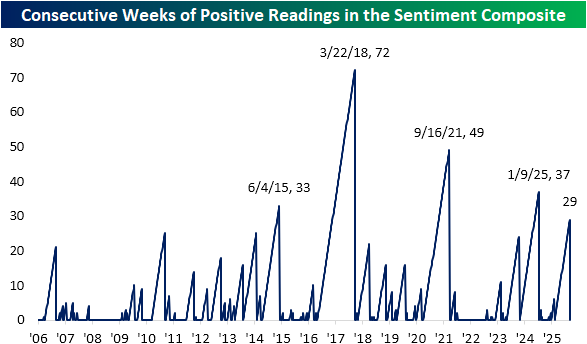

Positive Sentiment Streak at an End

This week’s sentiment gauges saw some big moves. As we noted in last night’s Closer, the Charles Schwab (SCHW) Schwab Trading Activity Index, or STAX for short, experienced a near record increase in February. Meanwhile, other weekly sentiment gauges have deteriorated. The AAII survey is a prime example, as bullish sentiment fell to 31.9% this week. That is the sixth consecutive weekly decline, bringing bullish sentiment to the lowest level since the week of 11/13.

That drop in bulls was met with a double-digit percentage point surge in bears. Bearish sentiment leaped from 35.5% last week, a one-month low, to 46.4% today. That is the highest reading for bears since the week of 10/16 and the largest one-week increase since November.

Put together, the bull-bear spread has now been negative (meaning there are more bears than bulls) for the fourth week in a row. The 12.1 point drop this week was the biggest WoW decline since the week of 11/13, and the spread is also the lowest since that same week.

In other words, the AAII survey has taken a decisively negative tone partway through the second week of conflict with Iran. Likewise, the same can be said for other surveys, such as the NAAIM Exposure Index and the Investors Intelligence survey. The former showed active managers reporting as the least aggressively long since the final week of last April during the tariff-tantrum. Meanwhile, bulls dropped below 50% in the Investors Intelligence survey for the first time since November. Putting it all together, our Sentiment Composite is back to negative territory following over six months of positive readings.

As shown below, this week snapped a streak of 29 consecutive weeks of positive readings in the sentiment composite. With the streak over, it ends as the fifth-longest streak on record.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up:

Q4 2025 Earnings Conference Call Recaps: Dick’s Sporting Goods (DKS)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Dick’s Sporting Goods’ (DKS) Q4 2025 earnings call.

![]()

Dick’s Sporting Goods (DKS) is one of the largest sporting goods retailers in the US, selling athletic footwear, apparel, equipment, and outdoor gear through stores and digital channels. The company serves athletes, teams, and casual sports enthusiasts while increasingly positioning itself at the intersection of sports and culture. Its growing ecosystem includes experiential retail concepts like House of Sport, youth sports platform GameChanger, and a retail media network that connects brands directly with athletes and fans. Management highlighted steady consumer demand and strong product momentum across footwear, apparel, and hardlines, with Q4 comparable sales up 3.1% on top of a 6.6% comp last year, producing a nearly 10% two-year stack. Executives emphasized that shoppers are still spending on innovation and premium launches, especially in running, basketball, and women’s sports, while major events like the 2026 World Cup are expected to support demand. The biggest focus remains the turnaround of Foot Locker following its acquisition, where DKS is implementing its “Fast Break” merchandising reset, removing roughly 30% of unproductive SKUs and testing store redesigns that are generating strong comps. Meanwhile, experiential formats like House of Sport and Fieldhouse continue to expand, and digital platforms such as GameChanger and the Dick’s Media Network are emerging as new engagement and advertising channels. The company guided to 2%–4% comps in 2026 with Foot Locker expected to inflect around back-to-school. DKS shares opened 4.6% higher on 3/12 after reporting EPS and revenue beats…

Continue reading our Conference Call Recap for DKS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke’s Morning Lineup – Homebuilders Yield to the Treasury Market

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Great things are not accomplished by those who yield to trends and fads and popular opinion.” – Jack Kerouac

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on CNBC’s Money Movers yesterday to discuss the moves in the energy market and their impact on the equity market. To view the segment, click on the image below.

After a mixed session yesterday where the Nasdaq finished up 8 basis points (bps) while the S&P 500 fell 8 bps, US futures are firmly lower this morning, with the S&P 500 and Nasdaq both indicated to open down by about 35 bps. The primary culprit is crude oil, where prices are up over 5% and back above $90 as Iran stepped up attacks on tankers in the Persian Gulf. Energy Secretary Chris Wright was also just on CNBC and noted that the US is not yet ready to escort tankers through the Strait of Hormuz, but could be mobilized later this month. As long as the bottlenecks around the Strait continue, oil prices will remain elevated, raising the risk that the conflict makes its mark on the economy.

With crude oil prices rising, treasury yields are higher again as investors focus on the potential inflationary impacts. Gold prices are essentially flat, silver is up 2%, and Bitcoin is down fractionally but still above $70K.

Stocks were down across the board in Asia overnight, as the Nikkei was down 1.0%, while China’s Shanghai Composite was only down 0.1%, and the Kospi fell 0.5%. Relative to the last two weeks, it was a muted session! Given the spike in crude oil prices and the region’s dependence on energy imports, you could make the argument that it could have been worse.

In Europe, equities are also taking the overnight spike in crude oil prices in stride. The STOXX 600 is down just 0.4%, while Germany is fractionally higher. We’re also starting to see impacts of the conflict showing up in corporate results as UK travel firm On the Beach lowered guidance, citing a sharp slowdown in travel bookings for locations in the Eastern Mediterranean.

On the economic calendar this morning, we just had jobless claims, Building Permits, and Housing Starts at 8:30. Initial claims came in 2K lower than expected, while continuing claims were 1K higher, so from this perspective at least, the labor market remains very well behaved. With respect to the housing numbers, permits were lower than expected (1376K vs 1410K) while starts were much higher than expected (1487K vs 1341K), although much of the strength was due to multi-family units.

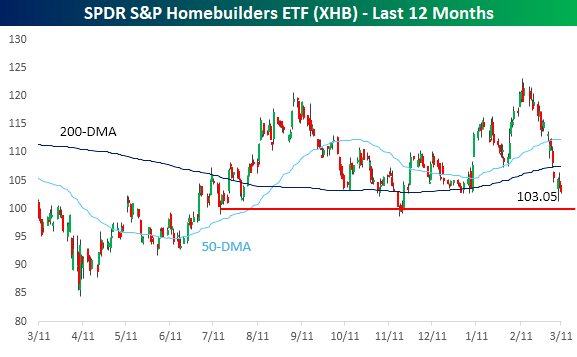

With treasury yields moving higher, it’s been a rough month for homebuilder stocks. The SPDR S&P Homebuilder ETF closed at $121.36 on 2/13, but has since declined more than 15% through yesterday’s close. Those highs in February were enough to push the group to 52-week highs, but the gains for 2026 quickly evaporated, and it’s now close to testing support at the $100 level.

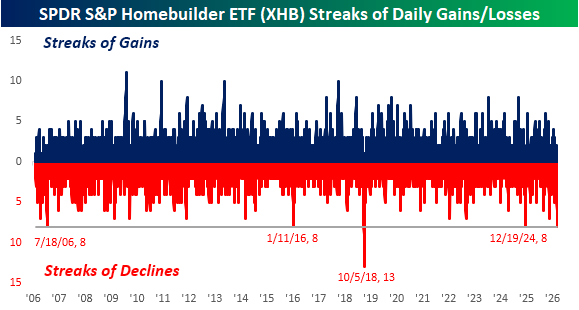

Part of that 15% decline since the February highs includes what is now an eight-day losing streak, which is tied for the longest losing streak in the ETF’s entire history. The last time there was a streak this long was over a year ago in late 2024, and the only longer streak was 13 days ending in October 2018.

The Closer – Inline CPI, Commodities and Recession, SPR – 3/11/26

Log-in here if you’re a member with access to the Closer.

- CPI came in right in line with expectations in February as deceleration in supercore services acts as a major factor.

- As the IEA announces release of emergency stockpiles, US strategic petroleum reserves are hardly recovered from massive drawdowns following the invasion of Ukraine.

- Retail investor sentiment experienced one of the largest monthly increases on record in February.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q1 2026 Earnings Conference Call Recaps: Oracle (ORCL)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Oracle’s (ORCL) Q3 2026 earnings call.

![]()

Oracle (ORCL) develops enterprise software, databases, and cloud infrastructure used by companies and governments to run core operations like finance, HR, supply chains, banking systems, and healthcare records. Its flagship technologies include the Oracle Database, Fusion ERP/HCM applications, and Oracle Cloud Infrastructure (OCI), which competes with hyperscalers in AI computing and cloud services. Oracle’s Q3 fiscal 2026 call centered on explosive growth tied to AI and cloud adoption. Multicloud database revenue surged 531% YoY, while AI infrastructure grew 243%, with management saying demand for GPU and CPU compute still exceeds supply. The company has secured 10+ gigawatts of future data-center power capacity and signed $29B in new infrastructure contracts, while its remaining performance obligations climbed to $553B. Oracle is embedding AI directly into enterprise software, with 1,000+ AI agents already inside its applications, and executives argued AI will strengthen, not replace, large enterprise SaaS platforms. A major push is also underway to run Oracle databases across Microsoft Azure, Google Cloud, and AWS, accelerating cloud migrations as companies move sensitive data to environments where it can be used with AI. ORCL shares rose as much as 12.5% on 3/11 after posting better-than-expected results…

Continue reading our Conference Call Recap for ORCL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q4 2025 Earnings Conference Call Recaps: AeroVironment (AVAV)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers AeroVironment’s (AVAV) Q3 2026 earnings call.

AeroVironment (AVAV) is a US defense technology company that develops autonomous drones, loitering munitions, counter-drone systems, directed-energy weapons, and space communications technologies for the US military and allied nations. Its portfolio includes battlefield-proven systems like the Switchblade loitering munition, Puma and Jump reconnaissance drones, Titan RF counter-UAS (Uncrewed Aircraft System) jammers, and the LOCUST directed-energy anti-drone system. AVAV reported a mixed quarter, with results missing expectations due to government funding delays, supply-chain shipping issues, and the termination of the Space Force’s SCAR (Satellite Communication Augmentation Resource) program. Despite the short-term setback, management emphasized strong underlying demand, pointing to $1.1B in funded backlog and $4.6B in year-to-date awards, and guided for record Q4 revenue with FY26 sales expected between $1.85B–$1.95B. The company is ramping production aggressively, including a new 140,000-sq-ft Utah factory capable of producing $2B of systems annually, to meet surging demand for Switchblade drones, Titan counter-UAS systems, and reconnaissance platforms. Management repeatedly linked demand growth to current geopolitical tensions, noting that conflicts involving large-scale drone warfare, including Iran’s regional attacks, are accelerating global military demand for both offensive drones and defensive counter-drone systems. Shares fell as much as 10% on 3/11…

Continue reading our Conference Call Recap for AVAV by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below: