Daily Sector Snapshot — 3/10/20

Buckle Up for the Close

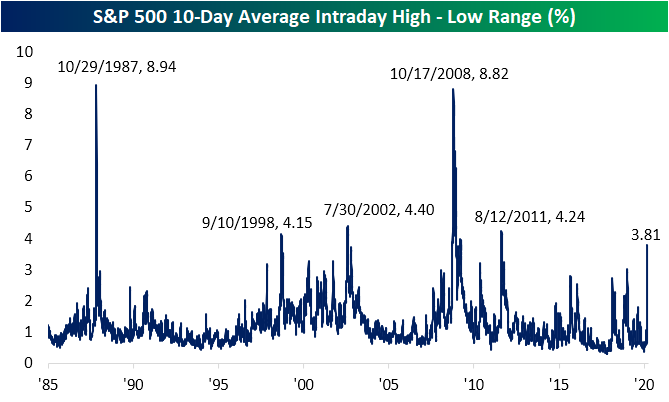

In the past 48 hours, we have witnessed futures reach both their limit up and down as well as a 15-minute freeze on trading yesterday when the S&P 500 fell 7%. If that is any indication, equities have been remarkably volatile. As shown in the chart below, over the past ten trading days the S&P 500 has averaged a 3.81% difference between the intraday high and intraday low. That is the highest reading since 2011 and since 1985 there have only been a few other periods of higher readings; the highest of which occurred in October of 1987 and 2008.

Delving deeper into the intraday patterns, the last hour, in particular, has been very volatile. Just from three o’clock to the close at four o’clock, the S&P 500 has moved up or down 1.1% on average over the past ten days. Again you would have to go back to 2011 to find this type of late-day volatility. Prior to that, only the financial crisis, 2002, 1997, and 1987 saw similar instances.

If the final hour of trading is too long of a time horizon for you, then try the final 15 minutes. Going back to 1985, there has only been one other 10-day period with a more volatile finish to the day: October of 2008. Back then, the final 15 minutes of trading averaged a 1.7% move; more than double the current volatility. The only other comparable period is back in October of 1987 when the last 15 minutes averaged a slightly smaller move of 0.83%. For comparison, from the start of the year to the S&P 500’s high on 2/19, the average absolute full-day change for the S&P 500 was even less than this at 0.57%. Start a two-week free trial to Bespoke Institutional to access our full range of research and interactive tools.

B.I.G. Tips – Strong Fundamentals and No New Lows

B.I.G. Tips: Puking Stocks

Chart of the Day: Playing an APAC Recovery

Bespoke Stock Scores — 3/10/20

Bespoke’s Morning Lineup – 3/10/20 – Turnaround (For Now)

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

After starting the day limit down yesterday, futures were briefly limit up today but have pulled back a bit. Besides the deeply oversold readings in equities, a catalyst for the surge is the Administration’s promised “very dramatic” actions last night. The White House plans being floated by the President last night include a payroll tax cut and short-term expansion of paid sick leave. Full details are due later today.

For now, markets will continue to trade off fear and headlines, so expect more of the same in terms of volatility.

Read today’s Bespoke Morning Lineup for a discussion of the moves overnight and this morning, the latest updated figures on the coronavirus, and a recap of Asian and European markets.

Below is an update of our S&P 500 sectors and where they are trading relative to their trading ranges. Every sector is currently oversold, and the only sector that isn’t at ‘extreme’ levels is Utilities. Along with Utilities, the only two sectors not more than 3-standard deviations below their 50-DMA are Consumer Staples and Health Care.

The Closer – Manic Mondays – 3/9/20

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we recap today’s historic session in which the S&P 500 fell by its largest amount since the financial crisis. We show what stocks drove these declines before evaluating claims that low oil prices will be a good thing for the economy. We finish by looking at what weakness in energy means for credit markets.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Daily Sector Snapshot — 3/9/20

A Day for the Decade

There have been bigger declines in the equity market throughout history, but not many. In fact, for the S&P 500 and many sectors, larger one-day declines haven’t been seen in at least a decade. The S&P 500 fell more than 7.5%, which was the largest one-day decline for the index since 12/1/08. After today’s drop, the US equity benchmark is down to its lowest level since June 3rd of last year.

In terms of individual sectors, ground zero for the market was the Energy sector. Going back to 1989 when daily data begins, today’s 20.1% decline was the largest one-day drop on record, and the index is now at its lowest level since August 2004. That’s not a typo! The only other sector that was down more than 10% today was Financials, which saw its largest one-day decline since 4/20/09 and is at its lowest level since Christmas Eve 2018. Industrials was another hard-hit sector today, and while it was down less than 10%, the 9.2% drop was still the largest one-day fall since at least 1989 and took the index to its lowest level since January 2019. Start a two-week free trial to Bespoke Institutional for full access to our research and interactive tools.