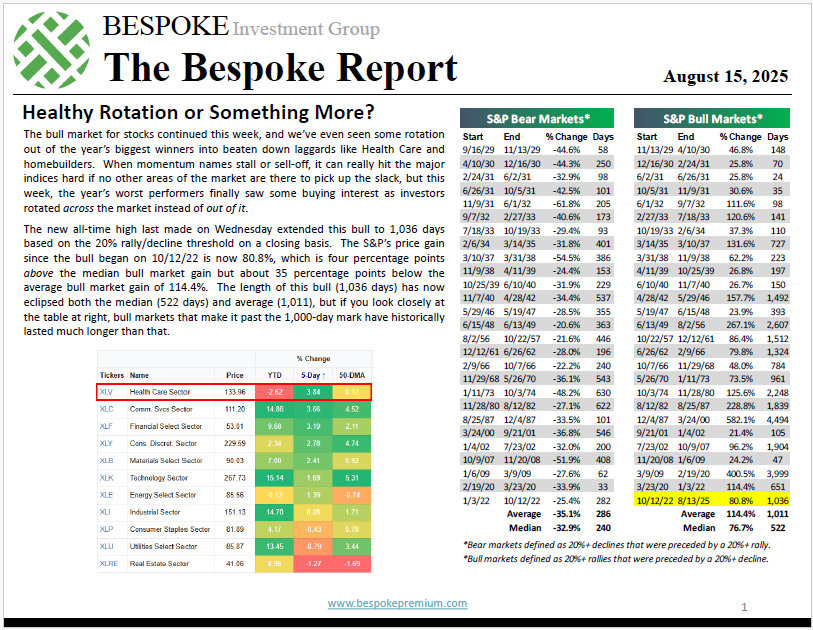

The Bespoke Report – Healthy Rotation or Something More?

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. Get caught up on everything going on in the investment world with the stock market at new highs by reading this week’s newsletter. Click here to sign up now!

B.I.G. Tips – Mixed Retail Sales

Bespoke’s Morning Lineup – 8/15/25 – Busy End for a Summer Friday

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The greatest danger occurs at the moment of victory” – Napoleon Bonaparte

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

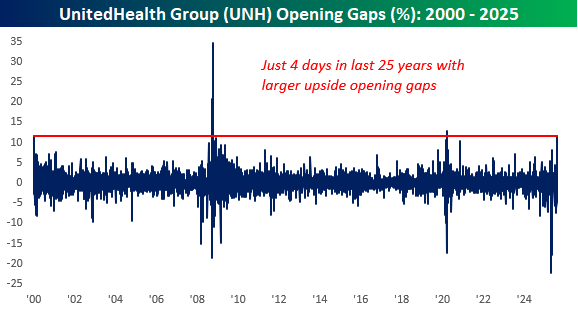

It may be a summer Friday, but there’s plenty of economic data to deal with this morning as Retail Sales and Import Prices were released at 8:30. At 9:15, we’ll get updates on Industrial Production and Capacity Utilization, and then at 10, Business Inventories and preliminary Michigan Sentiment will hit the tape. Heading into all the data, futures were mixed. Dow futures are sharply higher, but that’s all due to an 11% rally in UnitedHealth (UNH) following news that Berkshire Hathaway (BRK/b) has acquired a $5 bln stake in the company. Based on its current price, UNH is on pace to have its fifth-largest upside opening gap in the last 25 years.

It’s worth noting, though, that with the stock trading at $303 in the pre-market, it’s still trading more than 20% below its average closing price in Q2. We have no way of knowing Buffett’s cost basis on the position, but the odds are that Buffett is still underwater or barely positive on the position.

In Asia overnight, the Nikkei reversed Thursday’s losses following a better-than-expected GDP report and finished the day at another record with gains of over 1.5%. Chinese stocks were also higher, but economic data for the world’s second-largest economy missed forecasts as Retail Sales and Industrial output both came in weaker than expected.

European equities are higher across the board with modest gains as the STOXX 600 is up 0.20, led by France and Italy.

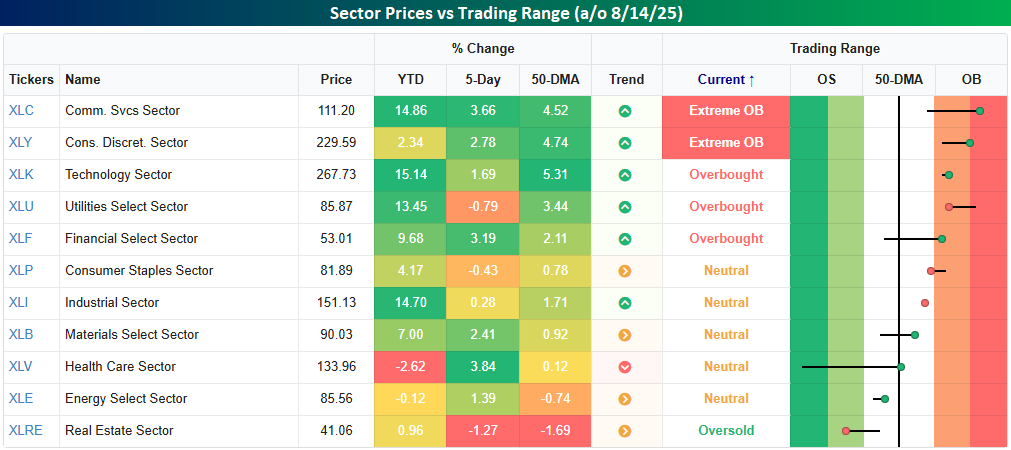

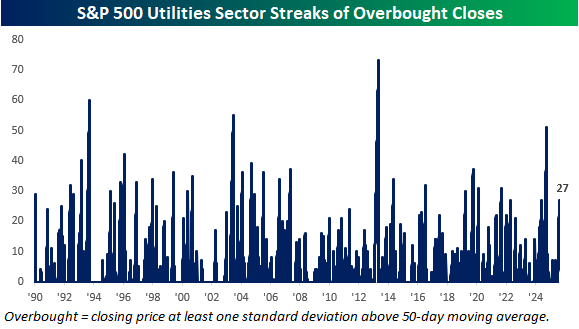

Looking through the various sectors and where they stand relative to their short-term trading ranges, we noted an interesting collection of sectors trading at overbought levels. Topping the list were Communication Services and Consumer Discretionary, which closed yesterday at ‘extreme’ overbought levels (2+ standard deviations above 50-DMA). Behind these two sectors, Technology, Utilities, and Financials all finished the day yesterday at overbought levels (1+ standard deviation above 50-DMA). It’s perfectly normal to see most of these sectors trading at overbought levels at a time when the market is in rally mode. The one exception is Utilities. Given its more defensive characteristics, Utilities tend to lag when the market is hitting all-time highs.

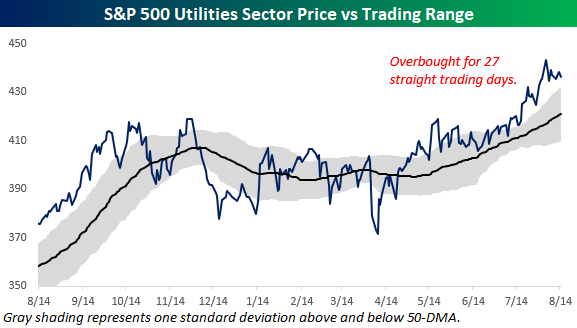

Utilities has been doing anything but lagging the broader market these days. As noted in last night’s Sector Snapshots report, the sector closed at overbought levels for the 27th day in a row yesterday.

At 27 days, the current streak of overbought closes for the Utilities sector is the longest since last October. As the chart below illustrates, though, this current streak is hardly extreme. The streak last October ended at 51 trading days, and there have been many other longer streaks in recent years.

The Closer – PPI, Best of Breed, Transportation – 8/14/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, wekick off with a look into the latest PPI report (pages 1 and 2) followed by an update on our Best of Breed basket (pages 3 and 4). We finish with a look into the disconnect between the Dow Transports and the semis (page 5) and then close out with a look at the latest freight data from Cass (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Weekly Sector Snapshot — 8/14/25

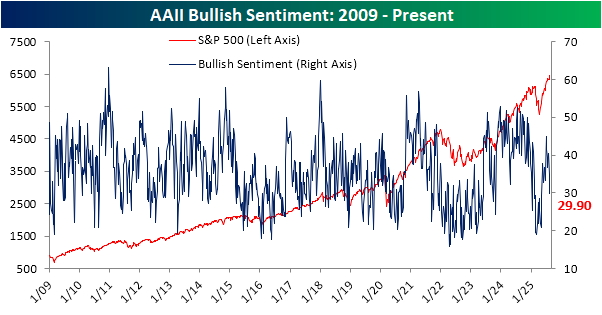

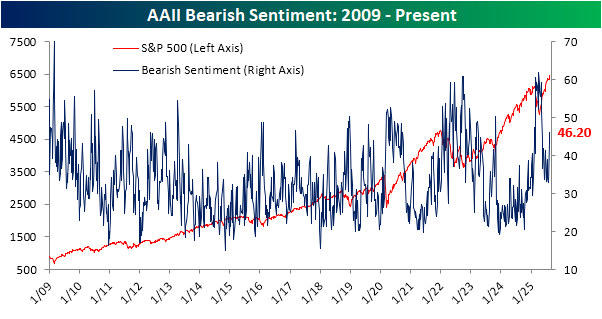

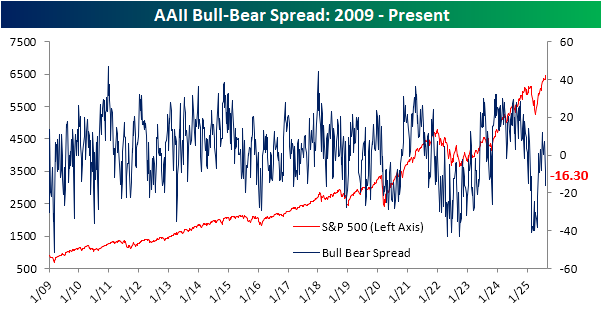

Sentiment and Stock Prices Diverge

The S&P 500 has had a couple of closes at record highs since last week’s update on sentiment from the American Association of Individual Investors (AAII). However, looking at the latest update, you wouldn’t have guessed the market was doing well. Bullish sentiment shed five points week over week, down to 29.9%, a level not seen since early May.

The lack of bulls coincides with a spike in bears up to 46.2%, which is the most elevated since May 8th.

Put together, bears are now outnumbering bulls by 16.3 percentage points, which is the lowest spread since the spring. Additionally, holding aside the fact that the S&P 500 is near record highs, this week’s reading is significantly lower than normal. Historically, the average bull-bear spread has been +6.4, putting the current spread 1.25 standard deviations below the historical average. In other words, sentiment has tipped into what can be considered elevated bearish levels.

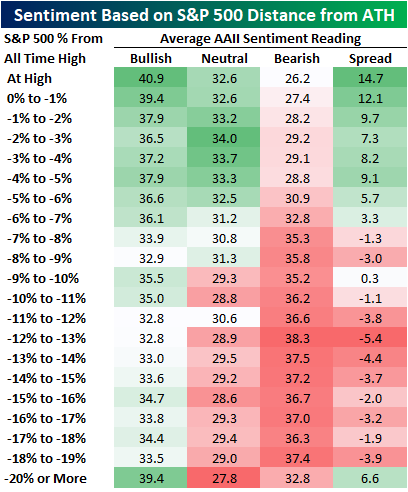

Again, it is one thing for bears to be out in full force to an extreme degree when stocks are weak. It is another entirely more surprising thing to see these levels when stocks are hitting record highs. In the table below, we show the average readings for bulls and bears in the AAII survey based on how far the S&P 500 is trading from all-time highs. As might be expected, sentiment has historically tended to be the most bullish/least bearish when the S&P 500 is closer to all-time highs. However, sentiment also tends to be more bullish when stocks are in pronounced pullbacks of at least least 20%. Comparing that to now, current levels of bullishness are about 11 points lower than what might be expected, and the level of bears is 20 points higher than what might be expected.

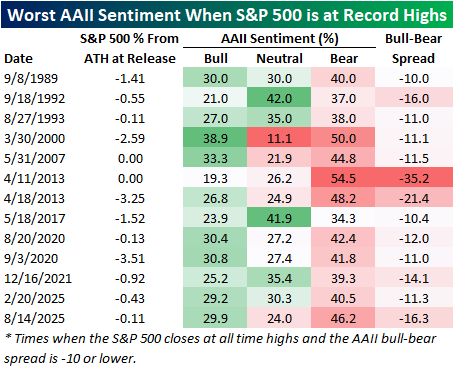

The degree to which investors reported as bearish was historic this week. In the history of the weekly AAII investor sentiment survey dating back to 1987, the bull-bear spread has only been lower in a week where the S&P 500 made an all-time high two other times. Both of those instances were in back-to-back weeks in 2013. Other than that, there have only been 13 weeks (including those two in 2013 and now) when the S&P 500 hit record highs and the bull-bear spread was -10 or lower. Before this week, there was also an occurrence earlier this year, almost exactly six months ago, right before the Q1 peak.

Chart of the Day: Solar Turning Point

Bespoke Consumer Pulse Report — August 2025

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Bespoke’s Morning Lineup – 8/14/25 – Ribbit!

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Don’t dream it, be it” – Dr Frank-N-Furter, Rocky Horror Picture Show

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Heading into this morning’s PPI and jobless claims reports, equity futures were all up less than 0.05% while the 10-year yield was unchanged. The July PPI report came in much higher than expected, though, and equity futures have moved lower, but not necessarily by as much as you would expect given the magnitude of the miss. While we’ll have to look further into the report for details, jobless claims remained subdued and came in lower than expected. It’s also worth pointing out that interest rates have barely budged higher.

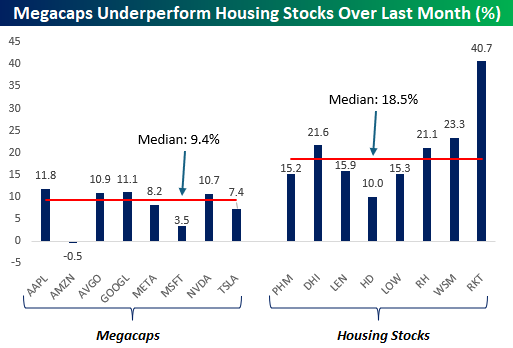

Quick question. Which group has done better over the last month? Megacaps or housing stocks? Most people would instinctively say the megacaps, but as the numbers show, the housing-related stocks have really surged over the last four weeks. The chart below compares the performance of the eight trillion-dollar megacap tech-like stocks to a group of eight housing-related stocks over the last month. For the housing basket, we’ve chosen a few homebuilders (Pulte, DR Horton, and Lennar), a couple of home improvement stocks (Home Depot and Lowe’s), housing retailers (RH and Williams Sonoma), and a mortgage company (Rocket Companies).

Of the eight megacap stocks, their performance over the last month has ranged between a decline of 0.5% and a gain of 11.1% for a median gain of 9.4%. Under any environment, 9.4% is impressive, but it pales in comparison to what the housing-related stocks have done. All eight of the stocks shown are up at least 10%, and their median gain has been nearly twice the gain of the megacaps (18.5%). HD is also the only stock in the group that isn’t outperforming all eight of the megacaps.

The Closer – Fedspeak, Distribution, Wild Moves – 8/13/25

Log-in here if you’re a member with access to the Closer.

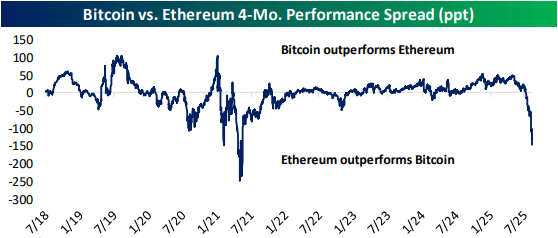

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, after a busy day of Fedspeak, we parse recent commentary to see what the likely outcome will be at the September meeting (page 1). We then dive into the bifurcation between well-off and insecure consumers (pages 2 and 3). Next, we check in on the wild moves observed under the hood today including the huge difference between value and momentum (pages 4 and 5). We finish with an update on the rally in crypto prices (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!