Daily Sector Snapshot — 11/25/25

Chart of the Day – And Then There Was One

Bespoke’s Morning Lineup – 11/25/25 – Big Moves

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You have put me in here a cub, but I will come out roaring like a lion, and I will make all hell howl!” – Carrie Nation

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

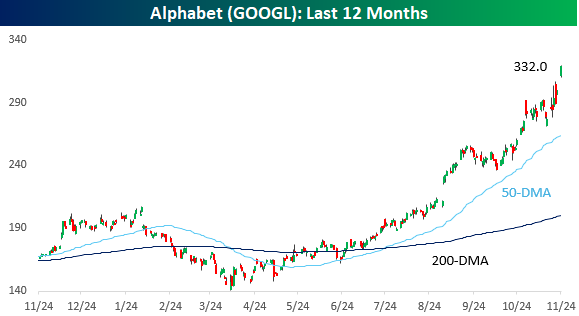

It’s an eventful morning in markets, but futures are little changed on all the cross-currents with the S&P 500 indicated to open up less than 0.10% while the Nasdaq is indicated to open down less than 0.10%. While futures on the Nasdaq are little changed, it comes are the index’s largest component – Nvidia (NVDA) – is down 5% while its third-largest component – Alphabet (GOOGL) – is up 4%.

Crude oil is down over 1% on reports of a truce in the Russia-Ukraine war while gold is up over 1%, and Bitcoin is down 2%. In Asia, major benchmarks were modestly higher, even as Softbank fell 10% as that stock corrects hard as investors question some of its massive and concentrated AI investments. In Europe, the tone is also muted with the STOXX 600 up 0.2%.

We also got some government economic data this morning, although it was from September, so it’s as stale as the bread you may be using for your Thanksgiving stuffing. Overall. the Retail Sales report for September was modestly weaker than expected while PPI was also slightly weaker.

It’s up again?

It’s up again!

When it comes to Alphabet (GOOGL), whether you identify with the phrasing above that uses the question mark or the exclamation point depends on whether you own it or not. We’ve seen a lot of unbelievable moves in mega-cap stocks in the last few years, but the recent surge in GOOGL ranks right up there with any of the others. Following news reports this morning that Meta Platforms (META) is considering the purchase of Google TPU chips for its data centers in 2027, the stock is up another 4% this morning which would take its one week gain to 16.7%. After trading as low as $140 back in April, the stock is up over 135%.

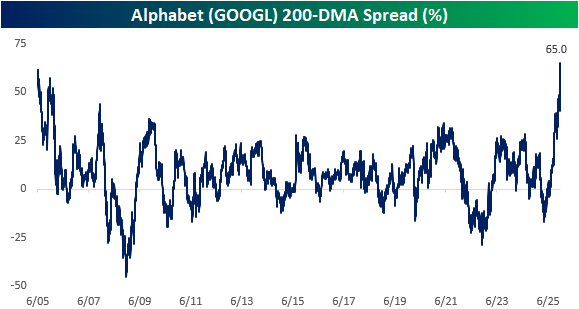

With the steep rally we have seen in GOOGL shares over the last few months, the stock is poised to trade 65% above its 200-DMA today. In the company’s entire history as a public company, that would be the most extended the stock has ever traded relative to its 200-DMA.

Besides the 135% rally off the April lows, over the last six months, GOOGL shares have rallied nearly 90%. The table below lists the ten largest gainers in the S&P 500 over the last six months, and GOOGL currently ranks eighth. In another sign that Tech and Communication Services still rule this market, the only two stocks on the list not from these sectors were Albemarle (ALB) and Robinhood (HOOD). What makes GOOGL stand out from the rest of the names is its market cap. At $3.8 trillion through yesterday’s close, GOOGL’s market cap is more than ten times larger than the next closest stock listed. It’s like an aircraft carrier sprinting with a fleet of skiffs.

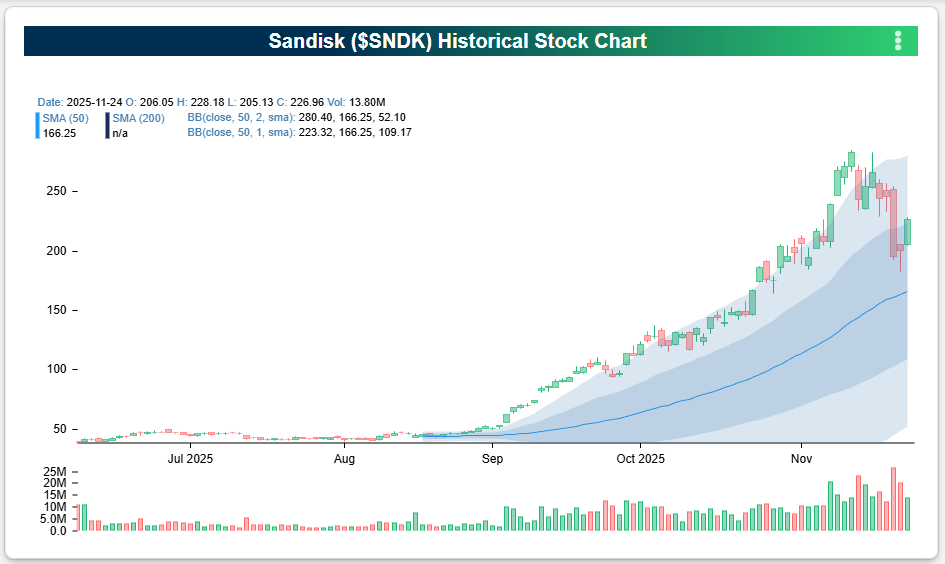

Last night after the close, news hit the tape that Sandisk (SNDK) would be added to the S&P 500 effective Friday (11/28). With the stock up nearly 500% over the last six months, the list of current top performers over the last six months is eating its dust. Looking at the chart below, it’s hard to imagine why, from a market timing perspective, anyone would think that now is a good time to add the stock to an index.

The people who make the decisions to add and subtract stocks to the various indices aren’t market timers, though. And while there are plenty of other stocks out there that would make worthy candidates, SNDK currently resides in the S&P 600 Small Cap Index. With a market cap of over $33 billion, though, it’s hardly a small cap, and it casts a large shadow over all the other stocks in the index in terms of size. After SNDK, the next largest stock in the S&P 600 is SPX Technologies (SPXC), but its market cap is less than a third of SNDK’s market cap. So, why not put it in the S&P 400 Mid Cap Index, you may ask. That would have been an option, but even in that index, SNDK would have already been the largest company in the index based on market cap. Even in the S&P 500, SNDK will still be larger than 228 of the index’s 500 components. Sometimes stocks become so large that there’s just nowhere else to put them!

The Closer – Quarterly Banking Profile, FOMC Dealmaking – 11/24/25

Log-in here if you’re a member with access to the Closer.

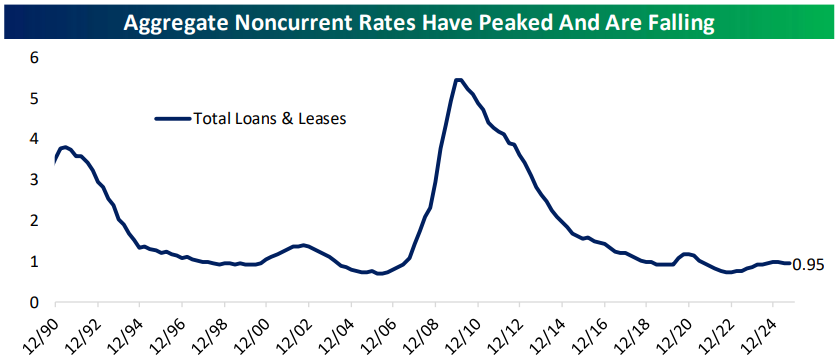

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we dive deep into the FDIC’s quarterly snapshot of the aggregate balance balance sheet for the US banking sector (pages 1-5). We then close out with a review of Fedspeak that suggests a deal has been struck between Governor Waller and Chair Powell (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 11/24/25

Q3 2025 Earnings Conference Call Recaps: Walmart (WMT)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Walmart’s (WMT) Q3 2026 earnings call.

![]()

Walmart (WMT) is the world’s largest retailer, serving millions of households across income levels through a massive physical footprint of supercenters, Sam’s Clubs, and expanding eCommerce. Known for its everyday low prices, Walmart provides groceries, general merchandise, health and wellness services, and an enormous third-party marketplace. Walmart delivered another strong quarter with 6% revenue growth, 27% eCommerce growth, and continued market share gains in grocery, apparel, and general merchandise. Higher-income households drove much of the momentum, while lower-income customers showed modest pressure. Delivery speeds hit records, with 35% of US digital orders arriving in under three hours, and automation now supports 50%+ of fulfillment center volume, lowering shipping costs. International strength was notable: China up 22%, and Flipkart’s Big Billion Days (BBD) generated over 700 orders per second at peak. Management was generally confident in its value proposition and growing alternative profit streams like advertising and membership, despite some discussion around tariffs. On better-than-expected results, WMT shares climbed 6.5% on 11/20…

Continue reading our Conference Call Recap for WMT by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: Mean Reversion Month; Big Losers

Q3 2025 Earnings Conference Call Recaps: NVIDIA (NVDA)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers NVIDIA’s (NVDA) Q3 2026 earnings call.

![]()

NVIDIA (NVDA) designs the world’s most powerful accelerated computing hardware and software, best known for its GPUs, networking platforms, and full-stack AI systems used in data centers, autonomous vehicles, robotics, and high-performance computing. The company sits at the center of the global AI infrastructure boom, supplying hyperscalers, sovereign governments, pharmaceutical companies, automakers, and millions of developers worldwide. NVIDIA posted another blowout quarter with $57B in revenue, up 62% YoY, as demand for AI infrastructure remained well above supply, and hyperscaler CapEx expectations rose to roughly $600B for 2026. Data center revenue hit $51B (+66% YoY), driven by the GB300 Blackwell platform and explosive growth in networking (+162% YoY). The company announced 5 million GPUs’ worth of new AI factory projects, including xAI’s gigawatt-scale Colossus 2 and Lilly’s drug-discovery supercomputer. Management also highlighted soaring momentum from frontier model builders: OpenAI reaching 800M weekly users, Anthropic hitting a $7B run rate, and both expanding compute commitments. Despite geopolitical limits in China, NVIDIA expects Q4 revenue of $65B and sees multi-year leadership ahead with the Rubin architecture ramping in 2026. NVDA shares rose more than 5% after hours on 11/19 in reaction to its triple play earnings report, but fell in the tech-led market reversal to close down 3% on 11/20…

Continue reading our Conference Call Recap for NVDA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke’s Morning Lineup – 11/24/25 – Rebound Continues

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“No man becomes rich unless he enriches others.” – Andrew Carnegie

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Following a Friday rebound on the back of comments from NY Fed President John Williams that he was open to a rate cut at the December meeting, the week is starting on a positive note. S&P 500 futures have rallied 0.5% while Nasdaq futures point to a gain of 0.76% as shares of Alphabet (GOOGL) trade up another 3% following comments from Marc Benioff saying how much better Gemini 3 is than ChatGPT and that he’s ‘not going back’.

Japanese stocks were closed for a holiday, but Hong Kong stocks surged 2% while South Korean stocks declined modestly in what was a generally quiet session to start the week. European stocks are generally off to a quiet start this week as well. The STOXX is basically unchanged, while Germany (0.5%) leads and Italy (-1.0%) lags. One major weakness in the region, though, is the defense sector, as a potential end to fighting in the Ukraine war has that sector selling off. In terms of data, it’s been quiet. The only report was German Business confidence from ifo, which showed an unexpected decline from October, falling from 88.4 to 88.1 versus forecasts for an uptick to 88.6.

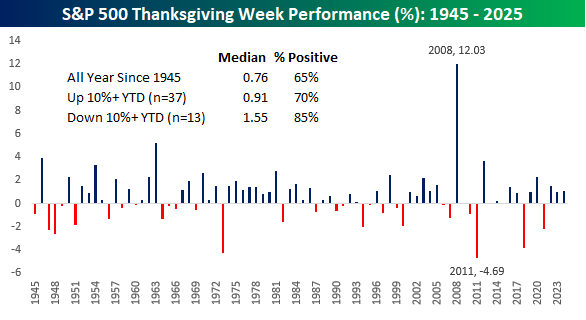

With the market only open for trading three-and-a-half days this week, it’s one of the shortest trading weeks of the year. With many on Wall Street usually taking Friday off, it’s only a three-day work week for many. It may be short, but Thanksgiving week has historically been strong. Since 1945, the S&P 500’s median performance during the week has been a gain of 0.76% with gains 65% of the time.

This year is the 38th time since 1945 that the S&P 500 was up by double-digit percentages heading into the week, and in the 37 prior years, the S&P 500’s median gain for Thanksgiving week was even stronger at 0.91% with positive returns 70% of the time. There have also been 13 years when the S&P 500 was down by double-digit percentages heading into Thanksgiving week. While you wouldn’t expect that investors would have had much to be thankful for in those years, the S&P 500’s median gain during the holiday week was a gain of 1.55% with positive returns 85% of the time.

As shown in the chart below, recent Thanksgiving week performance have also been positive. In the last three years, the S&P 500 rallied more than 1% in each Thanksgiving week, and it’s been positive during this week in eleven out of the last 13 years.

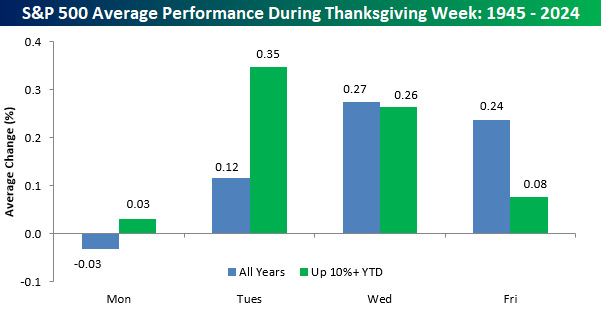

Looking at day-to-day returns, the chart below shows the S&P 500’s average performance during each day of Thanksgiving week for all years since 1945 and years when the S&P 500 was up 10%+ YTD. For all years since 1945, the strongest days of the week have been Wednesday and Friday (maybe you want to reconsider taking Friday off!), but in years when the S&P 500 was already up by double-digits, Tuesday and Wednesday were the best days of the week. One constant trend for Thanksgiving week? Monday was the weakest in terms of performance for all years and just years when the S&P 500 was already up 10%. What would you expect for a Monday?

Brunch Reads – 11/23/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

A Hail Mary on the Hurricanes: On November 23, 1984, Doug Flutie etched his name into college football history books with a single throw. Boston College was locked in a Thanksgiving-week shootout against the Miami Hurricanes, a national powerhouse. BC trailed 45–41 in the final moments of the fourth quarter, sitting 48 yards from the end zone with time for one last snap. Everyone in the Orange Bowl expected a desperation heave.

Flutie took the snap, scrambled back against a strong Miami rush, and uncorked a Hail Mary that traveled more than 60 yards in the air, dropping just behind two defenders into the waiting arms of wide receiver Gerard Phelan, Flutie’s roommate and closest friend on the team. Touchdown. Ballgame. Instant legend.

It changed Flutie’s life and solidified his Heisman trophy bid. It also gave Boston College one of the most iconic moments in its sports history. For a program without many national headlines, the Miracle in Miami became a forever highlight.

Click the image below to watch the clip on YouTube.

AI & Technology

He’s Been Right About AI for 40 Years. Now He Thinks Everyone Is Wrong. (WSJ)

Yann LeCun, one of AI’s most influential researchers, is drifting away from Meta as the company doubles down on large language models he thinks are a dead end. He’s been open about his belief that future AI will come from “world models” that learn through perception, not text prediction, and he’s been laying the groundwork for a startup built around that idea. Inside Meta, his old research group has lost influence while newer teams chase rapid, product-focused breakthroughs. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.