Eye-Popping Moves in Quantum Stocks

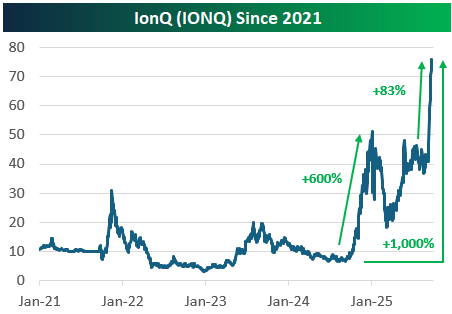

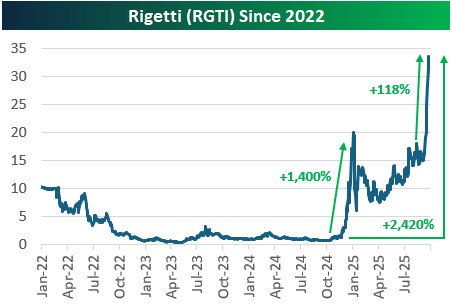

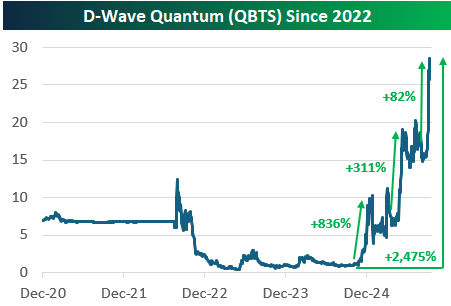

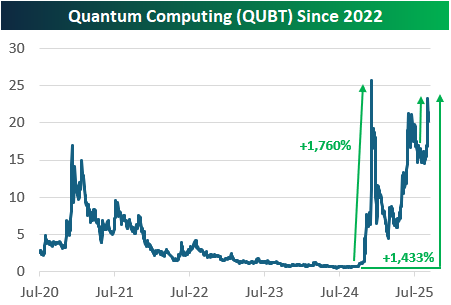

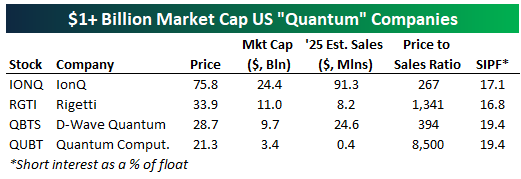

Quantum computing stocks have had another parabolic run recently. There are now four “quantum” stocks with market caps in the billions, and we provide recent price charts of them below.

IonQ (IONQ) is up the least of the bunch with a gain of 1,000% since its lows late last year. Quantum Computing (QUBT) is up the 3rd most with a gain of 1,433%, while Rigetti (RGTI) and D-Wave Quantum (QBTS) are both up more than 2,400%.

At their core, these “quantum” companies are working on the long-term promise of quantum computing: leveraging quantum mechanics to perform computations exponentially faster than today’s computers. The technology has the potential to transform industries such as cryptography, pharmaceuticals, and logistics, but the reality is that commercial viability remains decades away. Systems are still experimental, error-prone, and difficult to scale, with many breakthroughs required before they can solve real-world problems at scale. That hasn’t stopped speculators from bidding up quantum stocks to ungodly valuations, though.

As shown below, IONQ is projected to do $91.3 million in sales this year, which is the most of the group. Its market cap is all the way up to $24.4 billion, however, which gives it a price to sales ratio of 267! And that’s the smallest P/S ratio of the four stocks shown. 2025 sales estimates for RGTI are $8.2 million, while they’re $24.6 million for QBTS and just $400k for QUBT.

Q3 2025 Earnings Conference Call Recaps: Cintas (CTAS)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Cintas’ (CTAS) Q1 2026 earnings call.

![]()

Cintas (CTAS) provides uniforms, safety gear, first aid, and facility services to over one million businesses across North America, ranging from healthcare and education to state and local governments. The company is best known for its massive uniform rental business, but it also runs first aid and fire protection divisions. What makes Cintas stand out is its ability to thrive across economic cycles by converting “do-it-yourself” customers into long-term outsourcing clients, giving investors a real-time window into small and mid-sized business sentiment across the US. Q1 FY26 revenue grew 8.7% to $2.72B, with organic growth of 7.8%. Themes included resilient demand despite “somewhat uncertain” macro conditions, steady customer behavior, and continued success converting non-programmers. Labor market softness was noted but was not viewed as limiting growth. Tariff impacts are being managed via a diverse supply chain, rather than passed off on customers. Tech investments like AI, SAP, myCintas, and SmartTruck are improving customer self-service and salesforce productivity. CTAS shares stayed flat most of the day on 9/24 despite EPS and revenue beats…

Continue reading our Conference Call Recap for CTAS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day – Lithium and Uranium Power Surge

Q2 2025 Earnings Conference Call Recaps: Thor Industries (THO)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Thor Industries’ (THO) Q4 2025 earnings call.

![]()

Thor Industries (THO) is the world’s largest manufacturer of recreational vehicles, producing towable trailers and motorhomes under brands like Airstream, Jayco, and Keystone. The company gives unique insight into discretionary consumer spending, dealer sentiment, and broader macro forces like interest rates, tariffs, and labor market health, since RVs are big-ticket purchases that rely heavily on financing and consumer confidence. THO does not have a standard quarterly earnings call, but does release a presentation and Q&A document. In the Q&A, the company described a mixed backdrop: North American dealers are cautiously optimistic, but industry shipments are forecast to decline about 6% in the second half of 2025. Retail demand strengthened in spring, yet THO expects a low- to mid-single digit retail decline in fiscal 2026, citing affordability challenges and tariff pressures. Rising household debt and a softening labor market are clouding consumer sentiment, though falling borrowing costs could unlock demand if rates continue to ease. In Europe, sales remain flat as mainstream models lose share to premium and entry-level offerings, though new products debuted at Düsseldorf were well received. Innovation was a bright spot, with Keystone’s product refresh and the launch of Jayco’s Entegra Embark hybrid Class A motorhome, a notable step toward electrification. On the better-than-expected results, THO shares rose as much as 7% on 9/24…

Continue reading our Conference Call Recap for THO by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q3 2025 Earnings Conference Call Recaps: AutoZone (AZO)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers AutoZone’s (AZO) Q4 2025 earnings call.

![]()

AutoZone (AZO) is the largest US retailer and distributor of aftermarket automotive parts and accessories, operating more than 7,000 stores across the US, Mexico, and Brazil. It serves both do-it-yourself (DIY) customers and professional repair shops. The company’s massive hub and mega hub store network, along with new distribution centers, gives it an edge in parts availability and delivery speed. Q4 FY25 results held up despite tariffs and FX headwinds. Domestic commercial sales jumped 12.5% on a 16-week basis, with traffic up 6.2% and ticket growth of 3.7%, highlighting share gains from faster delivery and expanded parts availability. DIY comps rose 2.2% as tickets climbed 3.9% while traffic fell 1.9%, with discretionary categories showing “green shoots” for the first time since 2023. International comps grew 7.2% constant currency, though Mexico faced a $36M FX headwind. Inflation and tariffs remain central, with at least 3% SKU inflation expected and $120M in LIFO charges projected for Q1 FY26. AutoZone opened a record 304 net new stores this year, representing confidence in long-term demand. AZO shares were up less than 1% on 9/23 after posting weaker results…

Continue reading our Conference Call Recap for AZO by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Energy Comes to Life

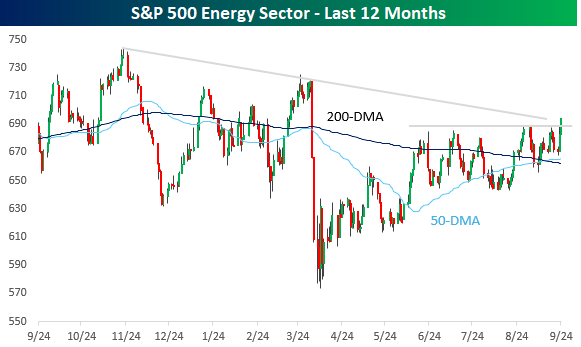

With a gain of less than 6% for the year, the Energy sector has been a big laggard, but with sectors like Technology and Communication Services starting to come under question for their valuations, investors are looking to other places for opportunities. Energy has been a beneficiary in the last few days. The sector has been meandering in a sideways range for the last three or four months, but just today, it broke above the high end of that range to its highest level since the tariff-tantrum in early April. Along with this new short-term high, the sector is also looking to test its downtrend line that has been in place since its high last fall.

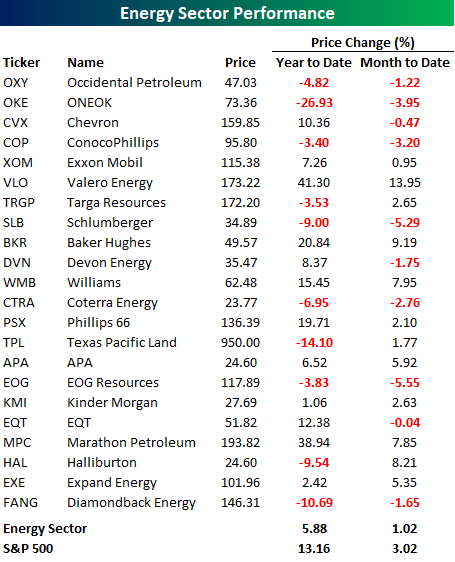

In terms of performance, Energy stocks have been chronic underperformers this year and even this month. The table below lists the YTD and MTD performance of the sector’s 22 components. On a YTD basis, less than half of the sector’s components are outperforming the sector this year, and less than a quarter have outperformed the S&P 500. Even on a MTD basis, the sector’s 1.02% gain has lagged the broader market’s rally of over 3%. Similarly, just half of the sector’s components are outperforming the sector this month, and less than a third (32%) are outperforming the S&P 500. It’s somewhat ironic that even with a positive chart formation, the Energy sector is still underperforming the S&P 500 by a wide margin on both a YTD and MTD basis, but that only provides another example of how strong the overall market has been.

Bespoke’s Morning Lineup – 9/24/25 – Repeat of Last Year?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Life starts all over again when it gets crisp in the fall.”- F. Scott Fitzgerald

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The S&P 500 was only down 0.55% yesterday, but that was enough to be the worst day for US stocks since the first trading day of the month. This morning, futures are showing modestly positive gains, with the S&P 500 up 0.13% and the Nasdaq trading 0.21% higher. Treasury yields are also higher as the 10-year has ticked up to 4.13% and is on pace for the fifth daily increase in the six trading days since last week’s cut. Crude oil is up 1% and back up to $64 per barrel for the first time since the middle of the month, but gold is giving back some of the gains from the last two days as it trades back down to $3,800 per ounce. It’s been a rough few days for crypto, but the sector is catching a break this morning as Bitcoin rallies more than 1% while Ethereum is up a more modest 0.55%.

Overnight in Asia, stocks were mixed, with Japan and China trading higher, while India and South Korea slid by about 0.5%. As we saw in many European PMI readings yesterday, Japan’s flash Manufacturing PMI slid further into contraction, falling from 49.7 to 48.4 versus forecasts for a more modest drop to 49.5.

European markets are more negative this morning, with the STOXX 600 trading down 0.3%, as luxury stocks drag the major averages, especially in France, lower.

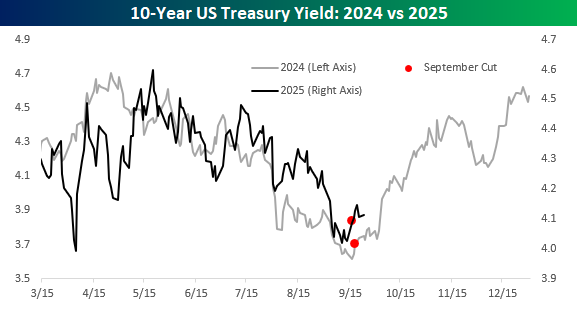

It’s been a week now since the Fed cut rates, and so far the equity market has seen a modestly positive reaction while treasury yields have moved higher, with the 10-year yield moving up to 4.11% from 4.03% last Tuesday, the day before the cut. The rise in yields over the last week undoubtedly is at least partially a reflexive response to what happened after last year’s cut. Back then, yields were in a steady decline in the six months leading up to the cut, falling from 4.7% to just over 3.6%, but the cut rang the bell, and from there, rates retraced all their previous decline by year’s end.

This year, we’ve seen a similar pattern where yields steadily declined leading up to last week’s cut and have been moving higher ever since. The one difference is that last year, most investors expected yields to continue falling into year-end, while this year, the consensus is expecting yields to rise and the curve to steepen. Will history repeat itself, or is it too obvious?

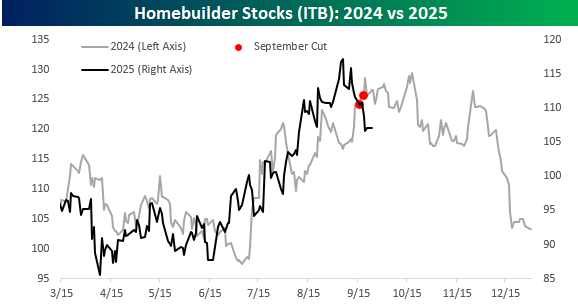

Homebuilder stocks are one of the most interest rate-sensitive sectors of the market, and like treasury yields, they’ve followed a similar pattern this year compared to last year. The one difference is that while the iShares Homebuilder ETF (ITB) was hitting highs for the year at the time of last year’s September cut, this year the ETF peaked about two weeks before last week’s cut. The fact that investors were starting to take profits in the homebuilders ahead of the cut illustrates the sentiment that there was less optimism towards long-term yields continuing lower after the September cut this year, compared to last year.

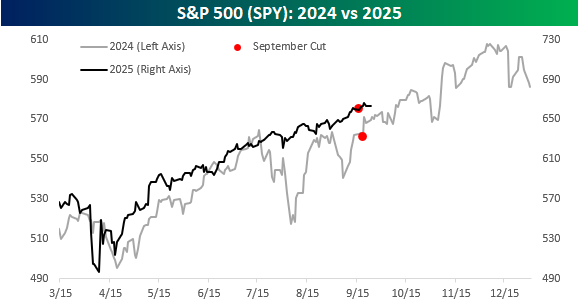

The S&P 500’s pattern this year varied from last year in that it has been much less volatile leading up to the cut than it was last year. In each case, though, it was trading either right at or very close to new highs at the time of the cut.

The Closer – Bottlenecks, S&P Additions, Ludicrous – 9/23/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with a look at the energy bottlenecks for the AI trade (page 1 and 2) before pivoting over to the latest flash PMIs (page 3). We then dive into the latest earnings and Fedspeak (page 4) before closing out with a look into S&P 500 new addition performance (page 5) and an update of our Ludicrous List (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!