The Closer – Chinese ADRs & EM, Jobs, BIS Triennial – 9/30/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a look at the performance of Chinese ADRs (pages 1 and 2) in addition to the outperformance of EM equities in Q3 (page 3). Next, we dive into the latest jobs data in the form of the JOLTS report (page 4) and Indeed job postings (pages 5 and 6). After that, we review consumer confidence figures (page 7) before closing out with the triennial snapshot of FX and interest rate derivatives (pages 8 and 9).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 9/30/25

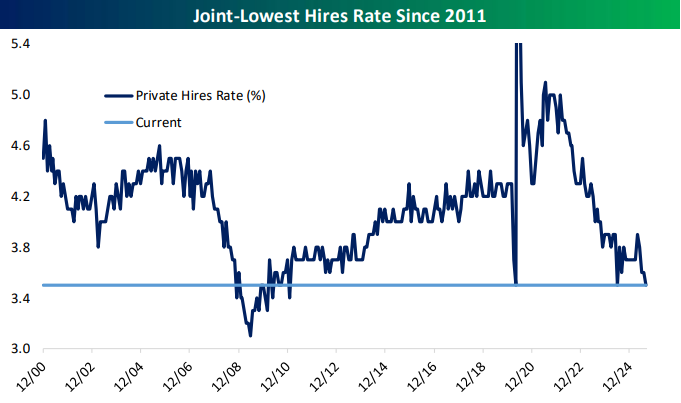

Chart of the Day – Shut it Down

Biggest Winners to Close Out Q3

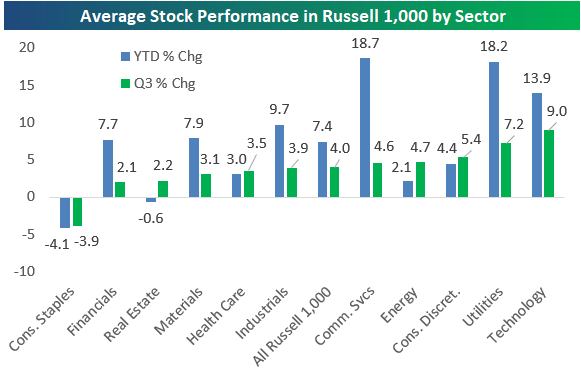

The large-cap Russell 1,000 is set to close out Q3 with a gain of roughly 7%, but the average stock in the index is up much less than that at 4%. The performance divergence is due to outperformance from mega-caps that push the cap-weighted index ever higher.

The five sectors whose stocks averaged bigger Q3 gains than the broad index (4%) are Technology (9%), Utilities (7.2%), Consumer Discretionary (5.4%), Energy (4.7%), and Communication Services (4.6%). Just one sector saw its stocks average declines in Q3: Consumer Staples (-3.9%).

Year-to-date, two sectors stand out: Communication Services and Utilities. Stocks in each of these sectors are up an average of 18%+ year-to-date through three quarters. Tech ranks 3rd at 13.9%, followed by Industrials at 9.7%.

Two sectors have seen their stocks fall year-to-date on average: Consumer Staples (-4.1%) and Real Estate (-0.6%).

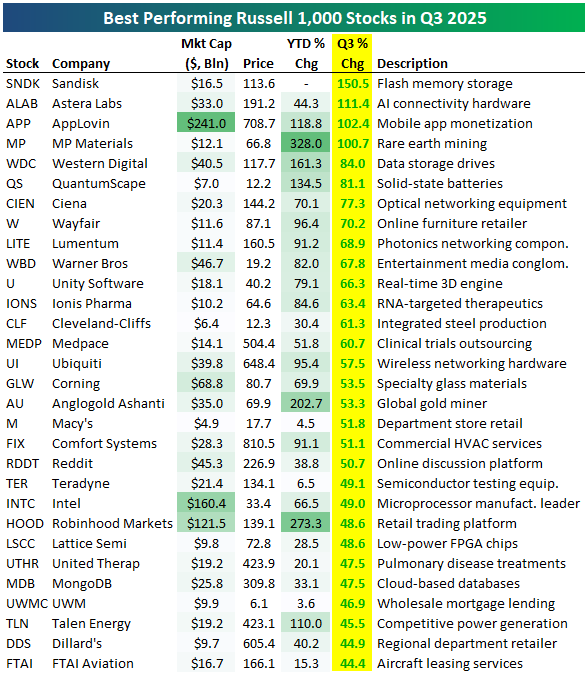

Below are the 30 best performing stocks in the Russell 1,000 in Q3. There are four companies that gained more than 100% during the quarter: Sandisk (SNDK), Astera Labs (ALAB), AppLovin (APP), and MP Materials (MP). Another four gained more than 70%: Western Digital (WDC), QuantumScape (QS), Ciena (CIEN), and Wayfair (W). While there are a few names on the list of Q3’s big winners that aren’t related to AI, the AI Boom certainly made its presence felt.

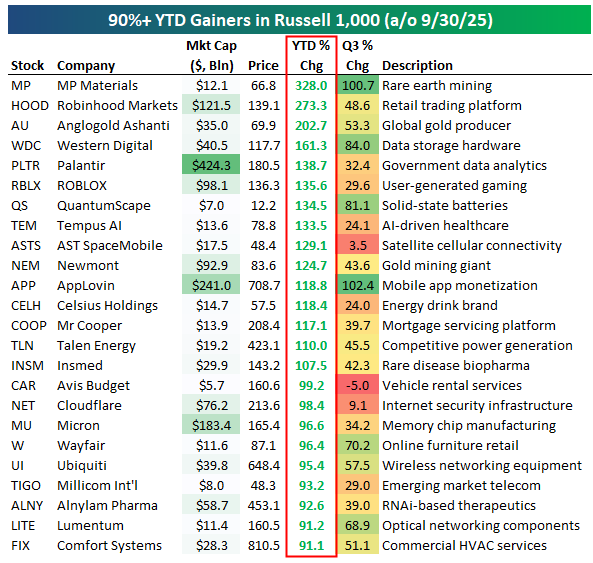

There are 24 stocks in the Russell 1,000 up 90%+ year-to-date as we close out Q3, including 15 that are up 100%+. MP Materials (MP), which gained 100% in Q3, is at the top of the leaderboard with a YTD gain of 328%. Two more stocks are up 200%+ on the year: Robinhood (HOOD) and Anglogold (AU). Western Digital (WDC) and Palantir (PLTR) round out the top five with YTD gains of 161% and 139%, respectively.

Other 100%+ winners through three quarters include social-gaming app ROBLOX (RBLX), AI healthcare platform Tempus AI (TEM), satellite cell-service provider AST SpaceMobile (ASTS), and energy-drink maker Celsius (CELH).

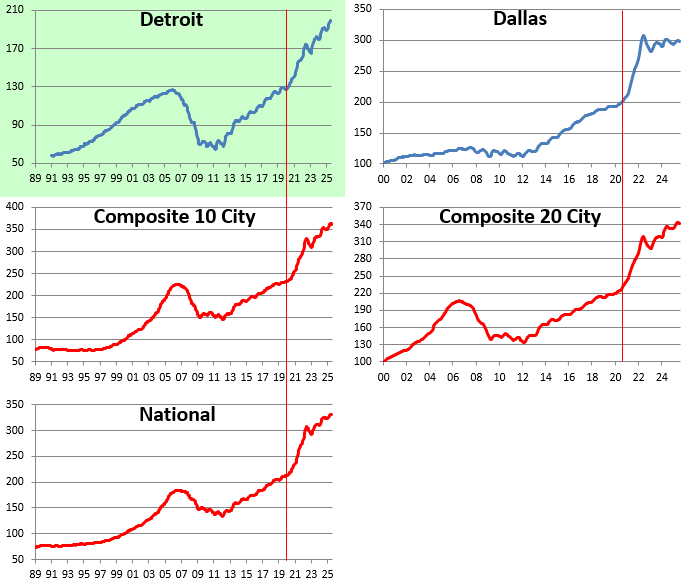

Midwest Resilience vs. Coastal Fatigue

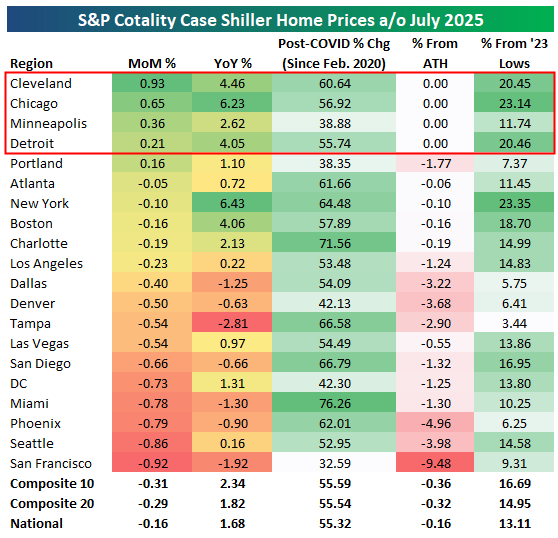

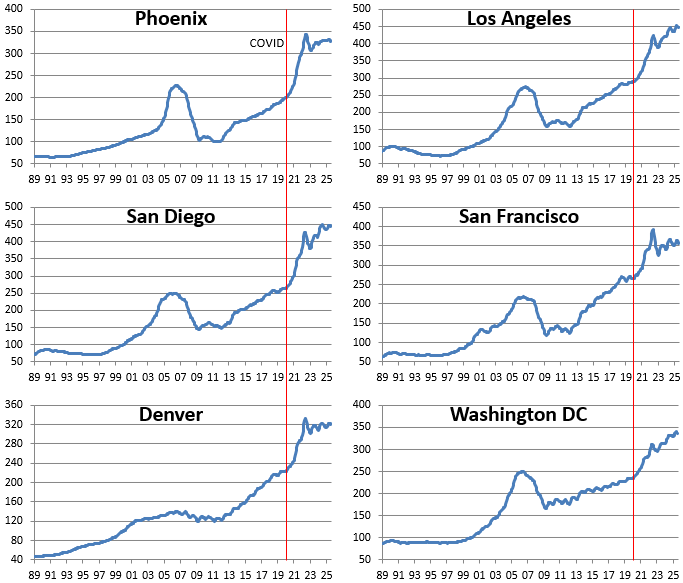

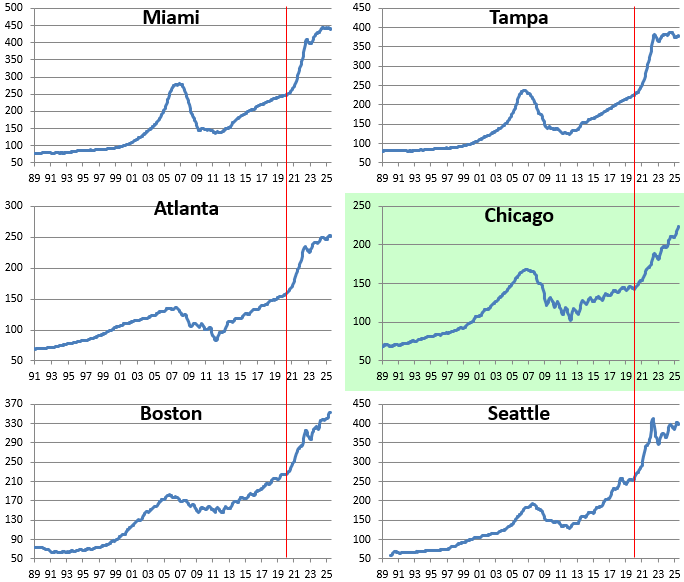

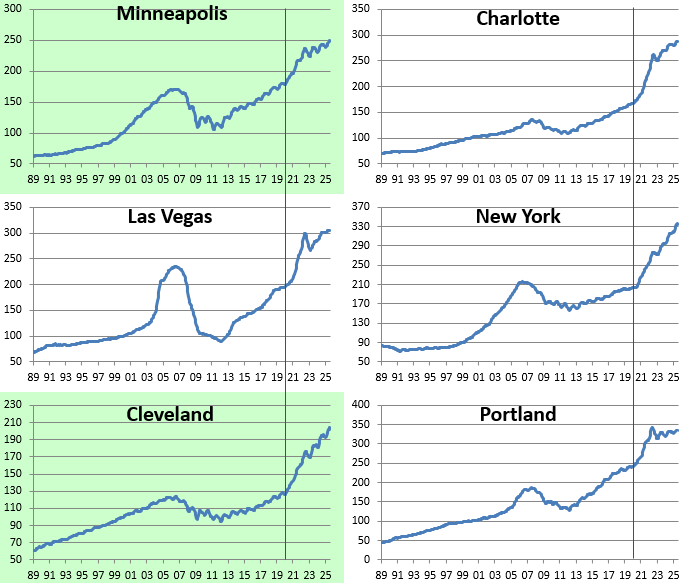

The latest S&P Case-Shiller home price data paints a clear regional divide in the U.S. housing market. Midwest cities were up on the month and remain at all-time highs (Cleveland, Chicago, Minneapolis, Detroit), while cities in the South and West continue to struggle.

Strength in the Midwest appears to be driven by relatively lower absolute price levels, tight supply, and steady migration in from more expensive regions.

In the South and West, many metros that were pandemic-era darlings are now rolling over. Places like San Francisco, Phoenix, Seattle, Las Vegas, Tampa, and Miami all saw monthly declines and remain below all-time highs. San Francisco was down the most of any metro on the month with a drop of 0.92%, while Tampa is down the most year-over-year at -2.8%.

Along with the Midwest, major metros in the Northeast like Boston and New York that are also supply constrained remain up solidly year-over-year and were only down slightly on the month.

Based on the latest Case Shiller data, the dynamic has flipped: instead of “Sun Belt boom, Rust Belt lag,” the post-COVID housing cycle now features a Midwest resilience vs. coastal fatigue narrative.

Below are price charts for each of the metros tracked. The four Midwest cities that hit all-time highs in the latest month are highlighted in green.

Bespoke’s Morning Lineup – 9/30/25 – Tuesday, The New Monday

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It is easy to ignore the rain if you have a raincoat” – Truman Capote

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Be sure to catch Paul Hickey today on CNBC’s Squawk on the Street at 10 AM.

It’s a modestly negative tone this morning as S&P 500 futures trade down 0.2% and the Nasdaq is down slightly less. Headline writers are attributing the weakness to concerns over a government shutdown, but those fears didn’t seem to bother anyone yesterday. Maybe it’s just Tuesday (see below). Treasury yields are slightly higher, crude oil is down nearly 1%, gold and other precious metals are lower across the board, as is crypto.

Overnight, Asian stocks were mostly lower. Japan traded down 0.3% as market expectations for a rate hike increase, and the government raised its forecasts for consumer spending for the first time in over a year. PMI data in China was mixed, with the manufacturing component coming in slightly ahead of forecasts (but still below 50) while the services index missed expectations.In Europe, most major indices are little changed as economic data in Germany (Retail Sales) and France (CPI) missed expectations.

In the US today, we’ll get the Chicago PMI, which always seems to disappoint, at 9:45 followed by JOLTS and Consumer Confidence at 10 AM. The only earnings report of note is Nike (NKE) after the close.

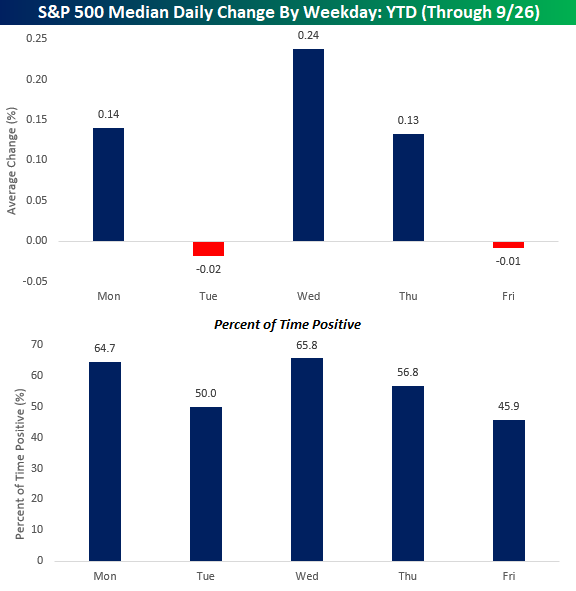

What’s so bad about Monday anyway? Lately, not much. The S&P 500 rallied 0.26% yesterday for its fourth straight positive start to the week and continuing a trend that has been in place for most of the year. Through last Friday, Mondays have been the second most positive weekday of the year with a median gain of 0.14% and gains 64.7% of the time. The only day of the week that has been stronger this year is Wednesday, with its median gain of 0.24% and gains 65.8% of the time.

\While Mondays have been strong, Tuesday is the new Monday as it ranks as the weakest weekday of the year with a median decline of 0.2% this year and gains just half of the time. The only other day of the week that has experienced negative returns on a median basis this year is Friday. So, maybe it shouldn’t come as any surprise that futures are lower this morning.

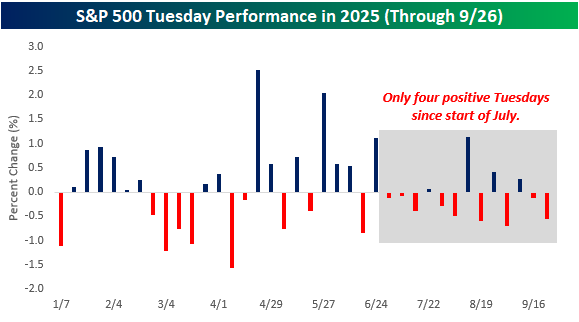

Looking at Tuesday performance more closely, the third quarter has been especially weak. Since the start of July, only four of the twelve Tuesdays have seen gains, so if the S&P 500 can manage to squeeze out a gain today, it would break what has been a pretty consistent trend of recent weakness.

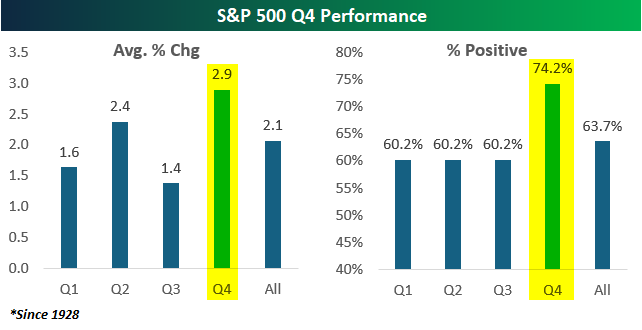

Today marks the last trading day of Q3, which has historically been the weakest quarter of the year. Since 1928, the S&P 500’s average performance during Q3 has been a gain of 1.4% with positive returns 60.2% of the time, but returns in Q4 have been better than and more consistent to the upside with an average gain of 2.9% and gains just under three-quarters of the time. For more analysis on quarterly seasonality, make sure to check out Monday’s Chart of the Day.

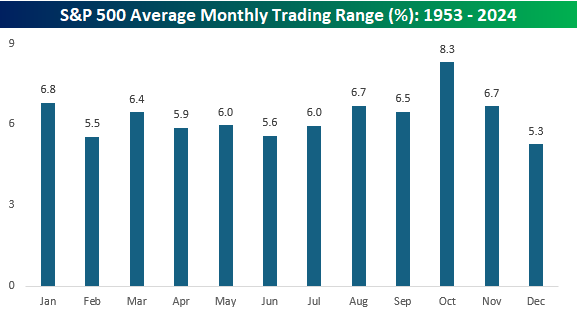

While Q4 has historically been strong, buckle up for some volatility. The chart below shows the average monthly trading range of the S&P 500 since 1953 (when the five-day trading week in its current form started). October’s average high-low spread (%) has been 8.3% which far surpasses the average monthly range of any other month. The next closest month is January at 6.8%. What’s notable about the 1.5 percentage point spread between the most volatile and second most volatile months is that it’s also the same as the spread between the second most volatile (January) and the least volatile months (December).

The Closer – Credit Cooking, Retail Risk, AI Targets – 9/29/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a check up on the health of leveraged loan activity (page 1) followed by an update on regional Fed manufacturing indices (page 2). We then review the performance of some of today’s top performing stocks, namely those associated with retail risk appetite (page 3) in addition to how far AI stocks are trading relative to price targets (page 4). We finish with an update on some Brazilian data releases (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 9/29/25

Q3 2025 Earnings Conference Call Recaps: Carnival (CCL)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Carnival’s (CCL) Q3 2025 earnings call.

![]()

Carnival (CCL) is the world’s largest cruise company, serving millions of guests annually across North America, Europe, and Asia, offering vacation experiences that blend transportation, lodging, dining, and entertainment in one package. Its global footprint gives insight into leisure travel demand, consumer discretionary spending, and how travel trends shift across regions. Carnival’s scale, private island destinations, and disciplined capacity growth make it a bellwether for evolving consumer preferences in the broader travel industry. Carnival posted record net income of $2B, with yields up 4.6% on strong close-in demand and onboard spending. Bookings set new highs, with nearly half of 2026 already sold at higher prices and 2027 off to an “unprecedented” start. Celebration Key, the company’s new private Caribbean destination, generated 1.5B media impressions and is driving ticket premiums, while a pier expansion at Half Moon Cay will add lift in 2026. Minimal capacity growth (about 0.8% in 2026) and diversified strength in Europe and Alaska provide a favorable supply-demand backdrop. CCL shares popped 5.3% at the open on 9/29 but slumped more than 9% from the opening high despite the triple play…

Continue reading our Conference Call Recap for CCL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below: