Q1 2026 Earnings Conference Call Recaps: Cintas (CTAS)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Cintas’ (CTAS) Q3 2026 earnings call.

![]()

Cintas (CTAS) provides outsourced uniforms, workplace safety products, facility services, and fire protection solutions to over a million businesses, helping them manage essentials like employee apparel, compliance, and cleanliness. The company delivered another strong quarter with revenue up 8.9% to $2.84B (8.2% organic) and record gross margins across all route-based segments. Demand remains steady despite a “complex” macro backdrop, with resilience across healthcare, hospitality, and government customers. Growth continues to be fueled by new customer wins (two-thirds from “no-program” users, meaning customers previously handling everything themselves) and cross-selling into existing accounts. Management emphasized ongoing investment in SAP, route capacity, and sales resources to sustain above-GDP growth. Input costs like fuel and tariffs are manageable (about 1.7% of revenue), with no reliance on surcharges. The pending UniFirst acquisition adds scale, with closing expected in the second half of 2026. Guidance was raised, signaling confidence in continued momentum. The stock was down a modest 0.72% on 3/25…

Continue reading our Conference Call Recap for CTAS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Tarnished Gold

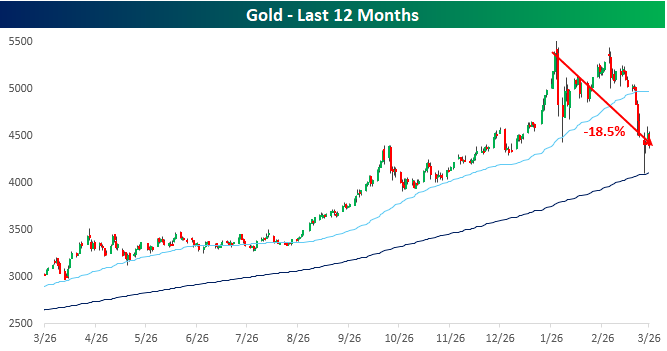

After bouncing yesterday, gold prices are declining again today, on pace for a one-day drop of over 3%. While today’s decline is not nearly enough for new lows on an intraday basis (it got down to the 200-DMA Monday), if gold closes at these levels, it will mark a new closing low for the current drawdown. That would take the peak-to-trough decline to 18.5% and very close to bear market levels (20%+ decline from a closing high without a 20%+ rally in between).

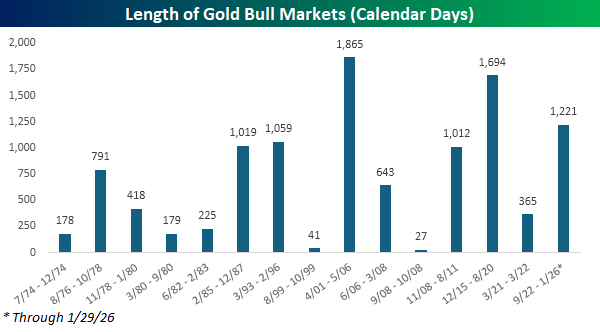

Bear markets haven’t been common for gold lately, as the current bull market began exactly three and a half years ago on 9/26/22. From that low through the closing high on 1/29/26, gold prices rallied 231.7%. In terms of magnitude, that would rank at the third longest since at least 1974, trailing only the 1,865-calendar-day bull market ending in May 2006 and the 1,694-day run ending in August 2020. For all 15 bull markets, the average length was 716 days, making the current one, if it turns out to have ended in January, 71% longer than average.

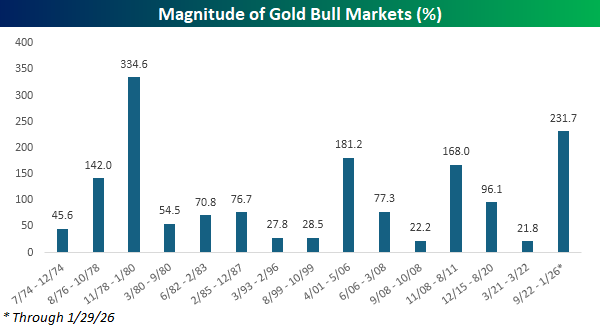

In terms of magnitude, the most recent bull market also ranks as one of the strongest. For all 15 bull markets since 1974, the average gain was 105%, or less than half of the gain during the current bull. In fact, the only bull market that experienced a larger gain was the 418-day bull market that ended in January 1980. In that 14-month rally, gold prices tripled from $191 up to $834 per ounce. Ironically, the level gold traded at when that bull market started is about the same as the amount by which gold prices are trading lower today!

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up:

Chart of the Day: Permanently Private

Bespoke’s Morning Lineup – 3/26/26 – No Joy in Marketville

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“When we have computers that can do more and more jobs, it’s going to change how we think about work. There’s no way around that. You can’t wish it away.” – Larry Page

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

There’s no joy in Marketville this morning as investors step up to the place for the opening bell. Nasdaq futures are down nearly 1% while the S&P 500 faces a gap down of 0.75% at the open. Treasury yields are higher across the curve, WTO and Brent crude oil are both up over 4%, gold is down 2.5%, and Bitcoin is down over 2%. Fun morning for the bulls!

With the five-day deadline imposed by the President, Monday fast approaching, and no signs of a diplomatic breakthrough, investors have no incentive to make a stand, and that doesn’t even take into account the government shutdown snarling air traffic. Maybe the only good news is jobless claims. Initial claims came in right inline with expectations, while continuing claims were well below forecasts, falling to a nearly two-year low.

In Asia, stocks reflected the pessimism as the Nikkei fell 0.3%, China declined 1.1%, and South Korea dropped the most, falling 3.2%. European stocks are doing no better. The STOXX 600 is down 1.0% halfway into the session, led lower by Germany and the UK, which are both down over 1.25%. ECB council member and Bundesbank President Joachim Nagel even noted that a rate hike in April is “certainly an option”.

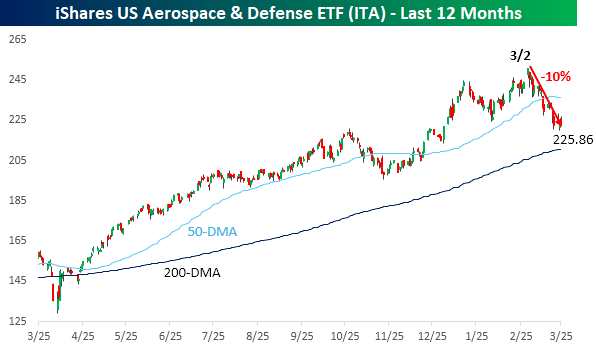

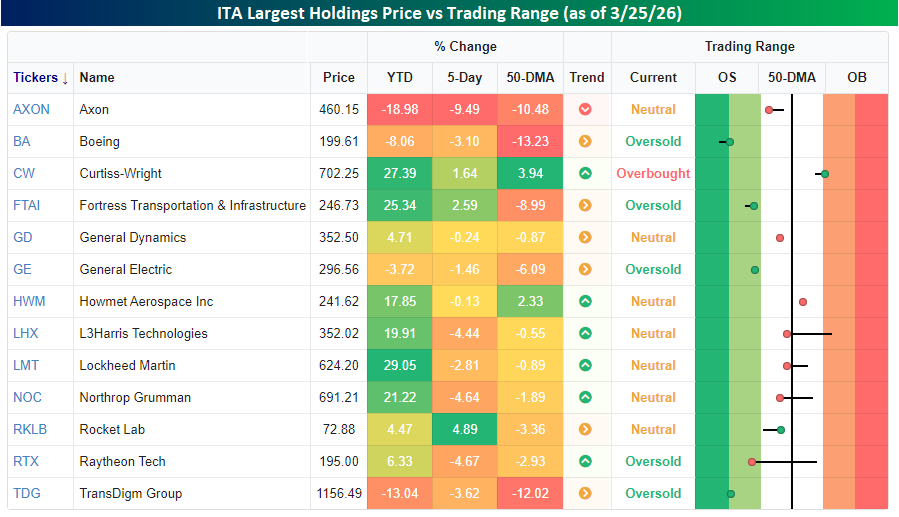

We’re now a month into the war in Iran, where every day’s news has shown images of precise strikes against the Iranian military. With all those weapons, it must be great for the defense contractors, right? Ironically, while aerospace and defense stocks performed well over the last year, they’ve seen a sell-the-news reaction since the war started. As shown in the chart of the iShares Aerospace & Defense ETF (ITA) below, the sector peaked on the first trading day after the first missiles were launched and has declined 10% since. That’s worse than the S&P 500!

Looking through a list of ITA’s 13 largest holdings (all greater than 2% weighting), performance this year has mostly been positive. Nine of the thirteen stocks are up YTD, with an average YTD gain of just under 9%. Like the ETF, though, most of the largest holdings are below their 50-DMAs. In total, their average 50-DMA spread is -4.2%, and they’re down an average of 2% in the last five trading days.

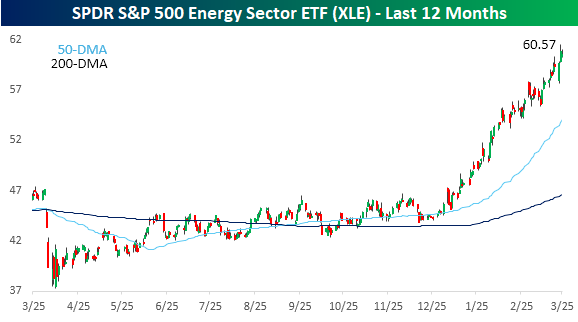

While defense stocks have struggled this month, Energy stocks have been on fire. The SPDR S&P 500 ETF (XLE) started to go parabolic at the turn of the calendar and hasn’t looked back since.

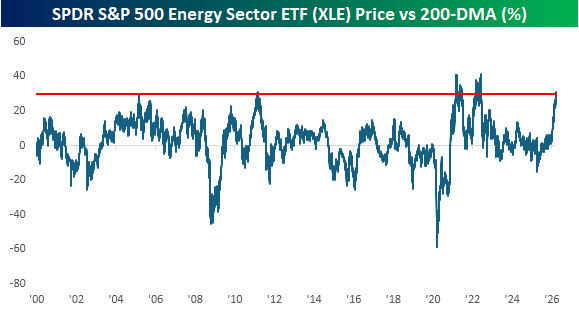

The rally in the sector has been so strong that the spread between XLE’s price and 200-DMA exceeded 30% this week. Since the ETF’s inception in 1999, there have only been a few other periods where the spread exceeded 30%. The most recent was early in the Russia-Ukraine war, and before that, the only other occurrences were in the first half of 2021 as the economy reopened from Covid and then briefly in early 2011 when oil prices spiked due to the Arab Spring and a civil war in Libya.

The Closer – Tech Valuations, Rotation, Trade Prices – 3/25/26

Log-in here if you’re a member with access to the Closer.

- Over the past six months the decline in the P/E ratio of Tech versus the S&P 500 has fallen by the largest amount since 2002.

- Performance this week has appeared to be largely rotational as the best performers were also those that were the worst performers month-to-date through Friday.

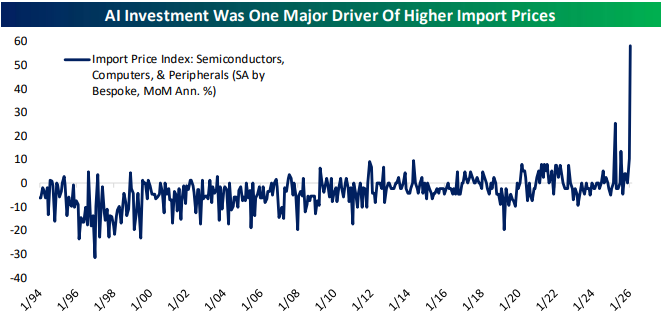

- After seasonal adjustment February saw the third-largest increase in ex petroleum import prices since monthly data begins at the end of the 1980s.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 3/25/26

Chart of the Day: Magnificent Valuations

Bespoke’s Morning Lineup – 3/25/26 – More Headline Driven Moves

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s the rough side of the mountain that’s the easiest to climb; the smooth side doesn’t have anything for you to hang on to.” – Aretha Franklin

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on Fox Business yesterday. To view the segment, click on the image below.

Global equity markets are in rally mode this morning after reports of potential negotiations between the US and Iran to end the war. Asian markets surged overnight, and that flowed into the European open and US futures this morning. Some of the air has come out of the balloon as we type this, though, on reports that Iranian officials have rejected the US terms delivered via Pakistan. There’s really no way to know at this point what the facts are regarding the state of negotiations, as neither side has any real incentive to conduct talks via the press, so expect more whipsaw action as things continue to progress. The bottom line is that while Iran still holds some cards, the chips are stacked heavily against them.

Outside of equities, the 10-year yield is down 5 bps, crude oil is down 5%, gold is up nearly 4%, and Bitcoin is up 2.5% to more than $71K.

In economic data, the only report on the calendar was Import Prices, which came in at more than double expectations (1.3% m/m vs 0.6%). If you’re looking for lower rates or a dovish Fed, these are not pretty numbers.

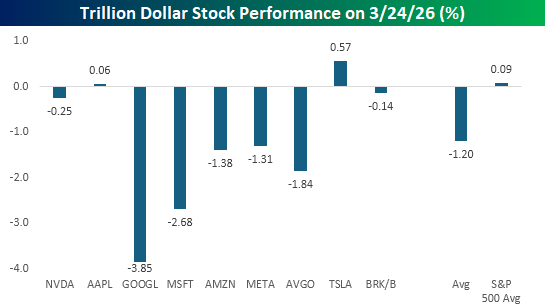

The S&P 500 finished down 0.37% yesterday, but most of the losses were focused in the trillion-dollar stock club, where the damage was much more concentrated. While the ‘average’ stock in the S&P 500 traded slightly higher yesterday, seven of the nine stocks in the trillion-dollar club traded lower, with an average of 1.2%. Stocks like Alphabet (GOOGL) and Microsoft (MSFT) were notably weak with declines of more than 2.5%, and both closed at multi-month lows. Other mega-caps like Broadcom (AVGO), Amazon.com (AMZN), and Meta Platforms (META) all fell more than 1%. The only mega-caps to buck the trillion-dollar market cap weight were Tesla (TSLA) and Apple (AAPL), which saw modest gains.

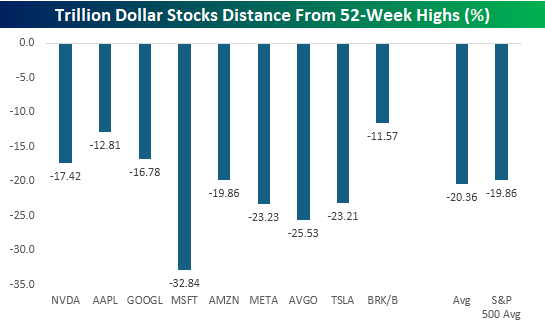

While the trillion-dollar stocks have been market leaders, they’re no longer the cool-kids table in the lunchroom. For months, they stood out above the rest of the market as the most popular in terms of where they were trading relative to 52-week highs, but now they no longer stand out. MSFT, AVGO, META, and TSLA are all down more than 20% from their respective 52-week highs, and the average drawdown from their peaks is just over 20%. That’s flirting with bear market territory and slightly more than the average 19.9% drawdown for all 500 stocks in the S&P 500.

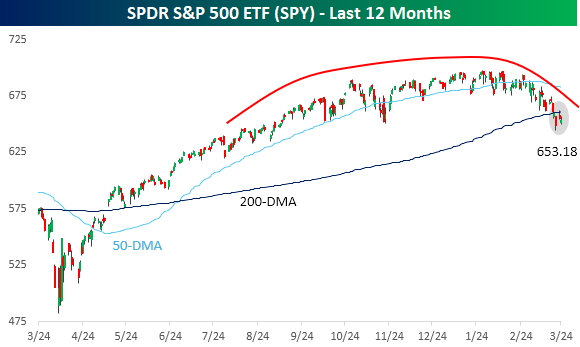

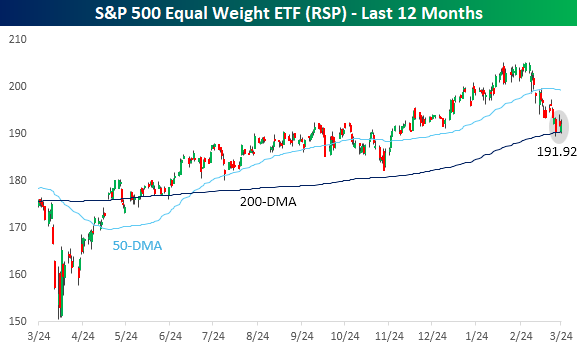

The cap-weighted S&P 500 (SPY) closed down just over 4% for the year yesterday, while the equal-weight version (RSP) is still slightly higher on the year (+0.2%), and their charts have two key differences.

First, as we’re all aware, the cap-weighted S&P 500 has been stuck in a sideways range for several months, forming a gradually curving, rounded top which accelerated when the war started at the turn of the month. The topping process for RSP was much sharper. From the start of the year right up until late February, RSP was steadily making new highs. Once the war broke out, though, the rally was stopped in its tracks, erasing two months’ worth of gains in less than a month.

Second, with RSP still holding on to gains for the year, it has also stayed above its 200-DMA. The same can’t be said for the S&P 500, which broke that level last Thursday. For now, bulls can rationalize SPY’s break of the 200-DMA by pointing to RSP still hanging on to that level. If both indices break that long-term average, though, bulls will have one less arrow in their quiver.

The Closer – 200-DMA Stop, Terrible 2s, 5 Fed – 3/24/26

Log-in here if you’re a member with access to the Closer.

- Throughout the S&P 500’s history, a hypothetical strategy that goes to cash when the index falls below its 200-DMA has outperformed.

- Today’s 2-year note auction saw terrible demand; similar to other coupon sales so far in March.

- Regional Fed surveys showed that there may have been supply chain stress even before the war with Iran began.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!