Q4 2025 Earnings Conference Call Recaps: D.R. Horton (DHI)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers D.R. Horton’s (DHI) Q1 2026 earnings call.

![]()

D.R. Horton (DHI) is the largest homebuilder in the United States by volume. The company designs and constructs high-quality, attainable homes primarily for entry-level and first-time buyers, who represent over 60% of its business. Its scale spans 126 markets across 36 states, providing insight into the health of the American consumer and the broader housing market. Management reported a disciplined start to 2026, beating revenue expectations with $6.9 billion despite “cautious consumer sentiment.” To combat affordability headwinds, DHI aggressively utilized mortgage rate buy-downs, maintaining a floor as low as 3.99% for some buyers. This strategy successfully drove a 3% increase in net sales orders. A key focus this quarter was “rightsizing” product; the builder is transitioning to smaller floor plans and higher-density communities to lower monthly payments. Despite broader economic uncertainty, the company reiterated its guidance to close up to 88,000 homes this year. On better-than-expected results, DHI shares opened 2.9% lower on 1/20, though erased most of the losses intraday…

Continue reading our Conference Call Recap for DHI by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

B.I.G. Tips – A Break From the Banks

Chart of the Day: Lower Opens After Long Weekends

Bespoke’s Morning Lineup – 1/20/26 – One Year

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Remember, your mind is like a parachute: If it isn’t open, it doesn’t work. So keep an open mind!” – Buzz Aldrin

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If this is the price we pay for a three-day weekend, maybe we should have kept the market open. It’s looking like a terrible Tuesday for US equities as the S&P 500 is poised to open down 1.4% while the Nasdaq is indicated 1.7% lower. Over the weekend, President Trump escalated his rhetoric towards Greenland and threatened tariffs on European allies if a deal isn’t reached. Today also marks the first anniversary of Trump’s second inauguration, and it’s been eventful to say the least.

Equity indices in Asia were weak, given the declines in US equity futures and the global trade tensions. The Nikkei was down over 1%, but India was the only other country down more than 1%. South Korea’s KOSPI declined 0.4%. Yes, you read that correctly- South Korean stocks had a daily decline for the first time in 2026. The more concerning aspect of the weakness in Asia, though, is in the bond markets where JGB yields are surging to multi-decade highs in their biggest one-day moves since the Liberation Day turmoil last April.

European stocks are much weaker this morning, and in early trading, the STOXX 600 is down 1.3%. Spain is leading the declines with a drop of 1.7%, followed by Germany (-1.6%), and Italy (-1.5%). The weakness this morning stems from President Trump’s announcement over the weekend that he would put tariffs of 10% on the imports of eight European countries beginning on 2/1, which will increase to 25% on 6/1, if no deal is reached on Greenland. Making matters worse are reports that the President will put 200% tariffs on imports of French wine if French President Macron refuses to join the Gaza Board of Peace.

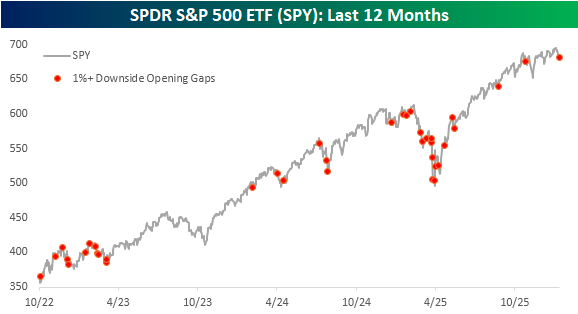

Whenever we see large declines like the market is poised for this morning, it always helps to put the move in perspective. The chart below shows SPY’s performance during the current bull market, and the red dots indicate every other time that SPY gapped down at least 1%. While today’s occurrence is only the third in the last eight months, since October 2022, there have been 37 other occurrences, which works out to an average of once per month.

Today’s gap down in SPY comes as the market has been stuck in a holding pattern for the last several weeks. Based on pre-market trading, SPY is trading right now at the same levels it traded in back in late October.

Brunch Reads – 1/18/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Oh, Bother: Every year on January 18, we celebrate Winnie-the-Pooh Day, which marks the birthday of A. A. Milne, the writer who created Pooh and the rest of the Hundred Acre Wood crew. Written nearly a century ago, Winnie-the-Pooh follows a honey-loving bear and his friends in a countryside inspired by the real Ashdown Forest in England.

Each character plays a distinct role that helps explain why these stories have endured. Pooh himself isn’t especially clever, but thoughtful in his own slow, roundabout way. He’s certainly forgetful and is intensely motivated by his love for honey. Piglet embodies anxiety, often afraid but willing to try anyway. Eeyore is connected to melancholy and pessimism, but he’s still always included and valued. Tigger has over-the-moon enthusiasm and confidence, while Owl is wise, despite his tendency to misspell words. Rabbit needs control, Kanga is overprotective, and Roo is very dependent. Christopher Robin, the only human, anchors the group.

The stories are filled with instantly recognizable symbols and lines that have become cultural shorthand. Pooh’s love of “a little something” to eat, his confusion over long words, and his tendency to pause mid-thought all reinforce the idea that not everything needs to be rushed or optimized. Lines like “You’re braver than you believe, stronger than you seem, and smarter than you think” and “Sometimes the smallest things take up the most room in your heart” are still iconic almost a century later.

Markets & Investing

Even Warren Buffett couldn’t keep beating the market without fail. Here’s why. (MarketWatch)

Even Warren Buffett’s edge has faded some, not because his skill spontaneously disappeared, but because extraordinary success attracts so much capital that beating the market becomes structurally harder. Berkshire Hathaway’s once-massive long-term outperformance steadily shrank as the portfolio grew, with returns converging toward the S&P 500 benchmark over the past couple decades. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

The Bespoke Report – 1/16/26 – Looming Return To Normalcy

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. This week we muse about a return to normalcy across markets, the economy, and society that is rapidly progressing but not quite complete. A review of equity markets from across the globe shows that normal might mean lower given valuations and price action that investors have gotten used to. We also dive into early earnings reports, US economic data, and some notable releases from the rest of the global economy this week.

Daily Sector Snapshot — 1/16/26

Bespoke’s Morning Lineup – 1/16/26 – South Korea’s 11-Day Streak

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“My advisers built a wall between myself and my people. I didn’t realize what was happening. When I woke up, I had lost my people.” – Mohammed Reza Pahlavi

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are bucking a general trend of weakness in international markets and are poised to open modestly higher. S&P 500 futures are indicated to open 0.15% higher, while the Nasdaq is looking at a gain of over 0.4%. Tech is leading the way higher as chip and memory stocks rally, while we’re seeing mixed reactions to earnings from regional banks. Treasuries are selling off as the 10-year yield pushes up near 4.2%, and crude oil is trading up over 1% to just under $60 per barrel. Metals are seeing weakness as gold is down nearly 1% while silver and platinum are down over 4%. Lastly, Bitcoin is up fractionally and above $95K, and Ether pushes up above $3,300.

Asian stocks ended the week on a mixed note but finished the week generally higher. The Nikkei fell 0.3% but finished the week up nearly 4%, while the Hang Seng was down by the same amount and finished the week 2.3% higher. China was the only outlier as the Shanghai Composite also traded down 0.3%, taking its YTD decline to 0.5%. South Korea traded 0.9% higher to close out the week (what else is new) and finished the week 5.6% higher.

Europe appears poised to close out the week on a sluggish note. The STOXX 600 is down 0.2% but still on pace for a weekly gain. France is the biggest laggard this morning as the CAC 40 drops nearly 1%, setting the stage for a weekly decline of 1.4%. The DAX is down close to 0.5% and teetering around the unchanged level for the week. December CPI in Germany was unchanged, which took the year/year rate down to 1.8%.

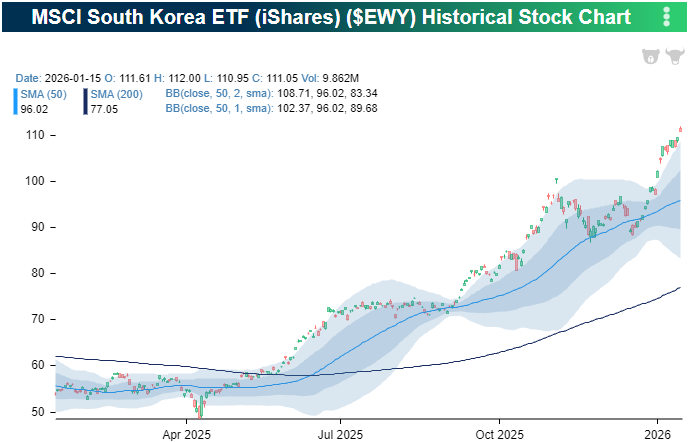

Getting back to the performance of South Korea, 2025 was already a strong year for the country, but it hasn’t skipped a beat so far in 2026. The chart below shows the performance of the MSCI South Korea ETF (EWY), and even after accounting for changes in the currency, it’s been a series of record highs all year.

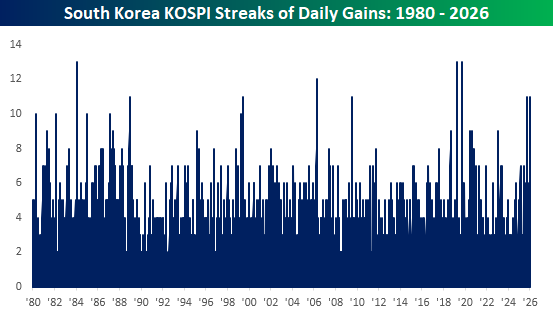

In local currency terms, the KOSPI traded higher on all eleven trading days this year. That’s an impressive streak, but it had another streak of the same length back in September. Before that, though, you have to go back to 2019 to find a streak lasting as long or longer. In fact, that 13-day streak in September 2019 was tied with a streak in April 2019 and February 1984 for the longest on record.

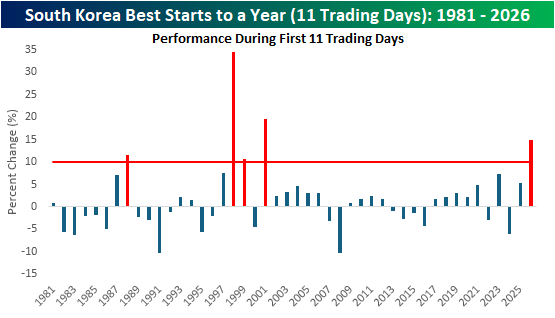

Over its current eleven-day winning streak, the KOSPI has rallied 14.9%, which ranks as the best start to a year for the index over 11 trading days since 2001 (19.6%). Since 1981, there have been four other years when the KOSPI rallied more than 10% in the first eleven trading days of the year. When you think about it, it’s interesting to see how a parallel to this period for the KOSPI traces back to the period starting in 1998, which is also just where we would be based on the comparison between the Nasdaq following the launch of Chat GPT versus its performance following the launch of Netscape in the early to mid-1990s.

Bespoke’s Wealth Management Report – January 2026

Please click here or on the link below to read our latest quarterly Wealth Management Report. You can learn more about Bespoke’s wealth management services available to investors here or by calling our office at 914-315-1248.

Below are links to prior quarterly Wealth Management Reports:

The Closer – Here Comes Midterms, Sentiment New High – 1/15/26

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with some commentary on the midterms (page 1) and the Health Care industry (page 2). Next up, we give an update of our Five Fed Manufacturing Composite (page 3) and check in on jobless claims (page 4). We then review the 52-week high in sentiment (page 5) before rounding out the report with a look at the resurgence of memory prices and related stocks (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!