Performance by Region

The US has had an incredibly strong 2021, especially when considering the headwinds the economy faced. Supply chain constraints, labor challenges, inflation, energy shortages, high oil prices, and new COVID variants all hindered the global economy this year. Nonetheless, since the start of the year, the SPDR S&P 500 ETF (SPY) has rallied over 25% YTD. While the US has been able to withstand the many headwinds, the same can’t be said for the rest of the world. The average performance for all of the other regions we looked at (Europe, Australia, Africa, Asia, and Latin America) was a loss of 3.4%. In 2021, there has been a huge divergence between the performance of developed markets and emerging markets. The US, Europe, and Australia have seen YTD gains of 15%+, while Africa, Asia, and Latin America have all seen pretty sizable declines. The US is on track to outperform both the rest of the world and emerging markets for the fourth consecutive year. Click here to view Bespoke’s premium membership options.

Daily Sector Snapshot — 12/8/21

Chart of the Day – Tantrum in Treasuries

B.I.G. Tips – State Level Searches for COVID Tests (12/8/21 update)

Job Openings Surge

The BLS released October results of the Job Openings and Labor Turnover Survey this morning showing a significant uptick in job openings. Openings totaled 11.03 million in October, slightly below the record of 11.098 million from this past July. Openings rose by 431K month over month which ranks as the biggest one-month uptick since July and is in the 94th percentile of all monthly moves.

While the JOLTS data is insightful, it is released at a decent lag. Job listings website Indeed, however, offers a higher frequency (daily) dataset with more up-to-date readings with the latest data available through November 26th. As we discussed ahead of the JOLTS release in last night’s Closer, postings through this reading have been hitting new highs and are 57% above the February 2020 baseline reading. That comes with acceleration in new postings being put up on the site throughout the fall, but especially so in recent weeks.

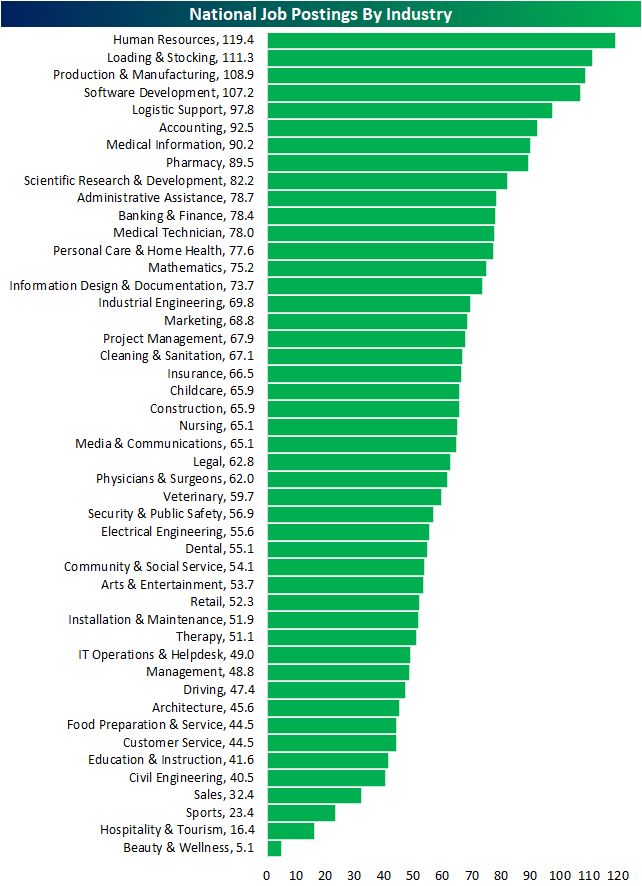

Indeed also offers a breakdown based on industry. As shown below, there are four industries that currently have postings that are twice as high as they were pre-pandemic. Ironically, given the fair degree of labor market slack, the human resources sector continues to top the list with postings almost 120% above the baseline level. Loading & Stocks, Production & Manufacturing, and Software Development are the other most in-demand industries through late November. The other end of the spectrum continues to include many reopening sensitive areas like Hospitality and Tourism (which has also been on the decline in recent weeks as shown in the next chart below), though, these too are now all above baseline levels.

As previously mentioned, Hospitality and Tourism have seen a decline in postings recently likely as a result of rising case counts. Noting a few other industries, Banking & Finance, Construction, Cleaning & Sanitation, and Food Preparation & Service have all seen an acceleration in postings. Click here to view Bespoke’s premium membership options.

Breezy Does It – Chicago Home Prices the Last to Take Out Prior Bubble Highs

The S&P Case Shiller home price indices for September 2021 were released recently and showed that home prices nationally are now up 47% from their prior highs made during the housing bubble of the mid-2000s. And notably, all 20 of the individual cities/regions tracked by S&P Case Shiller have now eclipsed their prior housing bubble highs now that Chicago has finally moved above its prior high from September 2006. As shown below, home prices in Chicago are now 1% above those September 2006 levels.

Two cities — Dallas and Denver — have home price levels now that are 100%+ above their mid-2000 highs. Five more cities are up at least 50% from their prior housing bubble highs — Seattle, Portland, Charlotte, San Francisco, and Boston.

You can see Chicago home price levels based on the S&P Case Shiller indices just barely eclipsing their prior highs in the chart below:

The pandemic has of course been a huge boon for home prices across the country. Below is a look at how much home prices are up versus levels seen in February 2020 just prior to COVID. Prices in Phoenix are up the most post-COVID at 45%, followed by San Diego and Tampa at 35%. Las Vegas, Charlotte, Miami, Dallas, and Seattle have all seen prices rise by 30%+, while the remaining cities are all up between 19% and 27%. Chicago, New York, and DC have seen home prices rise the least, but even these three cities are up ~20% since COVID hit. Like this type of analysis? See more of it with a Bespoke Premium membership. Click here to learn more and start a two-week trial.

Bespoke’s Morning Lineup – 12/8/21 – Booster Boost

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Change is the investor’s only certainty.” – Thomas Rowe Price Jr.

The pre-market tone for equities was flat to negative early, but a report from Pfizer (PFE) showing that three doses of its COVID vaccine were able to neutralize the Omicron variant sent futures notably higher. That boost has proved to be somewhat temporary, though, as futures have given up half of their earlier gains. With all the volatility we have had in the market lately, at this point, the most constructive activity we could see in markets today would be a quiet session for a change. Yesterday, the Russell 2000 had its 5th straight day of daily moves of more than 2%, and while the index traded back above its 200-DMA on an intraday basis, it wasn’t able to hold on to those levels into the close.

It’s another light day of economic data today as the only report on the calendar is the JOLTS report at 10 AM. Economists are expecting to see total job openings in excess of 10 million.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

On the Wednesday before Thanksgiving, the VIX traded as high as 20.96 intraday before closing the session at 18.58. The following Friday, it spiked as high as 28.99 on the emergence of the Omicron variant and continued higher the following week hitting an intraday high of 35.32 last Friday. This week has been another story for volatility, though, as the VIX has been in retreat finishing the day yesterday at 21.82. While still well above where it closed on the Wednesday before Thanksgiving, the VIX is currently within a point of its intraday high on the day before Omicron entered the lexicon.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.