Chart of the Day: Intraday Weakness

Bespoke’s Morning Lineup – 3/30/26 – Five, Going on Six?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The circumstances of the world are so variable that an irrevocable purpose or opinion is almost synonymous with a foolish one.” William H. Seward

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a rough finish to the week for bulls last Thursday and Friday, futures are looking to rally this morning after the President posted that “The United States of America is in serious discussions with A NEW, AND MORE REASONABLE, REGIME to end our Military Operations in Iran. Great progress has been made.”

As optimistic as those statements are, the President has made a habit of making positive early-week comments to try and soothe the market. It’s become so predictable that the Speaker of Iran’s Parliament posted on X last night that “ Pre-market so-called “news” or “Truth” is often just a setup for profit-taking. Basically, it’s a reverse indicator. Do the opposite: If they pump it, short it. If they dump it, go long.” So that’s where we are now.

Regardless of the investment advice from Iran, futures remain positive with the S&P 500 and Nasdaq both indicated to open up 0.6%, even as crude oil is higher (but off the overnight peak). Treasury yields are also sharply lower as the 10-year yield dips down to 4.37% from 4.44% last Friday. Gold prices are also 1.4% higher, and both moves could be taken as a sign that investors are becoming more aware of potential recessionary risks if the war drags on.

In economic data today, the Dallas Fed Manufacturing is the only report on the calendar, and economists expect a modest rebound from last month’s modestly positive report.

US futures may be higher this morning, but it was a rough night in Asia, with the only green shoot being China, where the Shanghai Composite eked out a 0.2% gain. Other indices in the region were all down roughly 1% or more, with the steepest declines coming in South Korea (-3.0%) and Japan (-2.8%). The yen briefly slumped to its lowest level versus the dollar in nearly two years, but rebounded to finish off its lows of the day after BoJ officials hinted that intervention could be on the way.

European equities are in a more jovial mood this morning as the STOXX 600 trades up 0.4% in the early going, while the FTSE 100 leads the region with a gain of 0.9%, but the rally has been broad with every major benchmark in positive territory, at least for now.

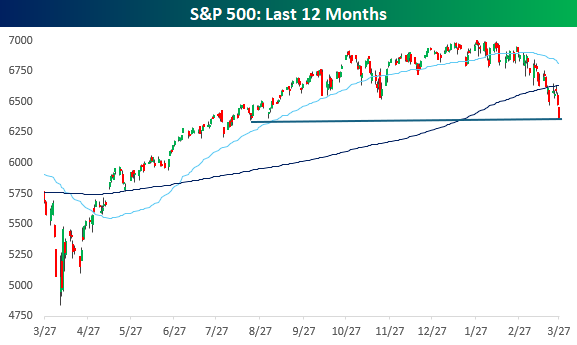

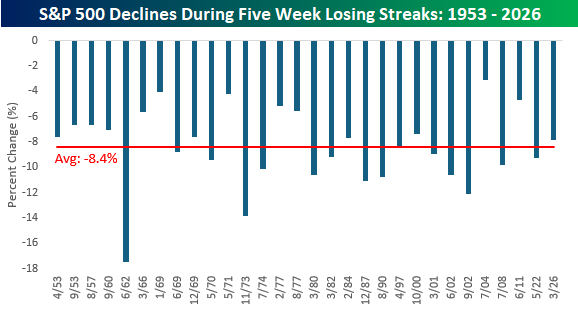

The S&P 500 traded down another 2.1% last week, extending its weekly losing streak to five and taking the total decline over this period to 7.8%. After breaking below its 200-day moving average the week before last, the intensity of selling picked up steam last week, taking the S&P 500 down to the lowest level since August 7. For anyone who argued that the market had gotten ahead of itself and needed a rest late last year, you got what you wanted. Despite all the weakness, though, the S&P 500 is still more than 30% above its intraday tariff-tantrum low from last April.

The current five-week losing streak in the S&P 500 ranks as the first such streak for the index in nearly four years (May 2022) and the 30th such streak since 1953, when the five-day trading week in its current form started in late 1952. With a decline of 7.8% during the last five weeks, the current decline has been less than the average of 8.4% for all streaks since 1952. The deepest decline was 17.5% in June 1962, while the mildest was in July 2004 when the S&P 500 declined just 3.1%.

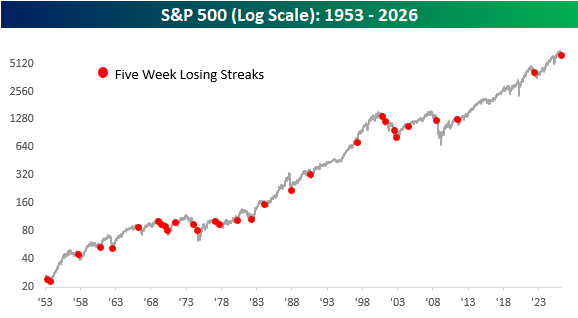

The long-term chart of the S&P 500 below shows when each prior streak occurred with a red dot. It’s interesting to see in the chart how these streaks were relatively common for much of the period from the early 1950s up through the Financial Crisis. Since the end of 2008, though, there have only been two other streaks in the last 17 years. Finally, in terms of whether these types of streaks represent buying opportunities or not, a look at the chart shows an inconclusive picture. Some of these streaks marked short-term lows for the market, but several others occurred right in the middle of longer-term downtrends.

Brunch Reads – 3/29/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Terracotta Tombkeepers: On March 29, 1974, a group of farmers digging a well in the countryside outside Xi’an struck fragments of clay that seemed ordinary at first but soon revealed pieces of life-sized human figures. Local authorities were notified, and archaeologists quickly determined the site was connected to the tomb complex of Qin Shi Huang, the ruler who unified China more than two thousand years earlier in 221 BC.

As excavation began, the scale of the find became shocking. Thousands of intricately detailed terracotta soldiers, along with horses and chariots, were arranged in battle formation across multiple pits, each figure unique in facial expression and posture. During the Warring States period, China was defined by constant conflict among rival kingdoms, where survival depended on military strength, innovation, and centralized control. When Qin Shi Huang emerged victorious, he imposed sweeping standardization across currency, writing, and infrastructure, while ruling with an iron grip. At the end of his life, rather than relying on symbolic burial items, he commissioned a full-scale army to guard him in the afterlife, a testament to the immense power of his rule and the extraordinary craftsmanship of the Qin dynasty.

Energy

The 2,000-Year-Old Cement Battery That Could Reduce Our Reliance on Fossil Fuel (WSJ)

A new “cement battery” uses a reversible chemical reaction to store heat from electricity, offering a simple and potentially cheap way to replace natural gas for industrial heating and buildings. If it scales, the technology could turn excess renewable energy into stored heat that can be used anytime, helping smooth out energy supply while reducing reliance on fossil fuels. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

The Bespoke Report – Equity Market Pros and Cons – Q2 2026

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition for Q2 2026.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking.

On page three of the report, you’ll see a full list of the pros and cons that we lay out. Slides for each topic are then provided on page four and beyond.

To read this report and access everything else Bespoke’s research platform has to offer, start a trial to any of our three membership levels today!

Daily Sector Snapshot — 3/27/26

B.I.G. Tips – End of Week Declines

Bespoke’s Morning Lineup – 3/27/26 – More Losses

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If my answers frighten you then you should cease asking scary questions.” – Quentin Tarantino

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s another one of those days where futures drift lower throughout the morning as traders follow the new daily routine of getting up, brushing their teeth, and clicking “Sell”. At 5 AM on the East Coast, when most of us were still asleep, futures were flat to marginally higher, but they have steadily lost steam all morning, and the S&P 500 is on pace to gap down 0.4%, while the Nasdaq is down 0.6%. Barring a major reversal during the trading day, the Nasdaq is poised for its 10th down week in the last 11. That consistency to the downside has only been seen in a handful of other periods throughout the index’s history.

Treasury yields are higher, with the 10-year yield up 4 bps to 4.46%, and WTI crude oil is up another 2.5% to just under $97 per barrel. That increase comes after President Trump said he would extend the deadline for Iran to open the Strait of Hormuz by 10-days because talks were “going very well”. While that looks bullish on the surface, it’s been taken as either a sign that the President is just buying more time to launch a ground invasion, or that talks are not going anywhere and the President is just stalling. The reality is that only a handful of people really do know, so investors are using the uncertainty as an excuse to sit things out.

On a more positive note, it looks like the government shutdown will end today, which should alleviate some of the pressure at US airports. Isn’t it ironic that after more than 40 days without paying TSA employees and subjecting people across the country to airport delays, Congress finally reached an agreement just in time for their two-week vacation? The idea that members of Congress are ‘public servants’ is starting to feel like the ultimate oxymoron; unless, of course, the public they’re serving is just each other.

In Asia overnight, most major equity benchmarks were lower on the session, although Hong Kong and China managed fractional gains. Outside of Australia, though, every other equity market was down for the week. In Europe, it’s much weaker with the STOXX 600 down 1.4%, putting it into the red for the week, and most individual country indices are down at least 1% on the day.

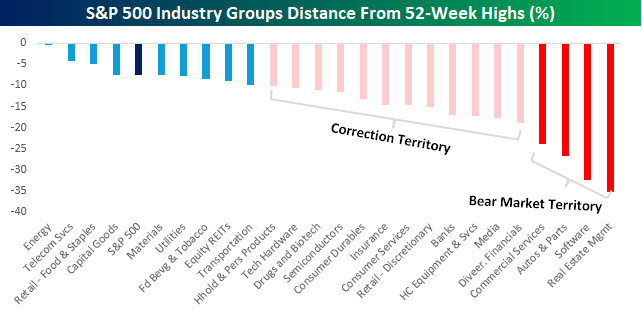

With yesterday’s decline, the S&P 500 is now down 7.5% from its intraday high earlier this year, putting it increasingly closer to correction territory. Of the 25 industry groups within the index, 16 closed at least 10% below their respective 52-week highs (on an intraday basis), and four of those are down at least 20%, putting them in bear market territory based on the 20% definition. Leading the way down, Real Estate Management has lost more than 35% of its value, but the most painful of the declines, given its weighting in the index, is Software, which is down by nearly a third.

On the positive, or less negative side, three groups closed within 5% of their respective highs yesterday, with the most obvious being Energy.

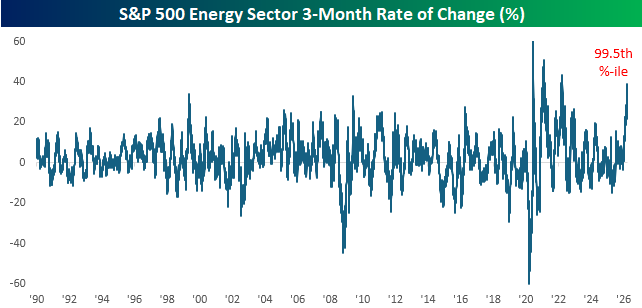

The rally in the Energy sector has reached historic proportions in the last few weeks. Over the last three months, the sector has rallied more than 38%, which ranks in the 99.5th percentile compared to all other periods since 1990. As shown in the chart below, the only times it experienced a larger rally were coming out of Covid and early in the Russia-Ukraine war.

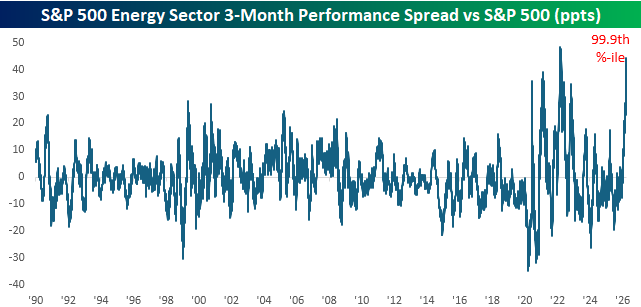

What’s even more impressive about the sector’s rally is that it came as the overall market declined. With the S&P 500 down over 6% in the last three months, the 44.4 percentage point performance spread between the two has only been wider for a brief period in March 2022. Outperformance of this magnitude on the part of the Energy sector is nearly unprecedented.

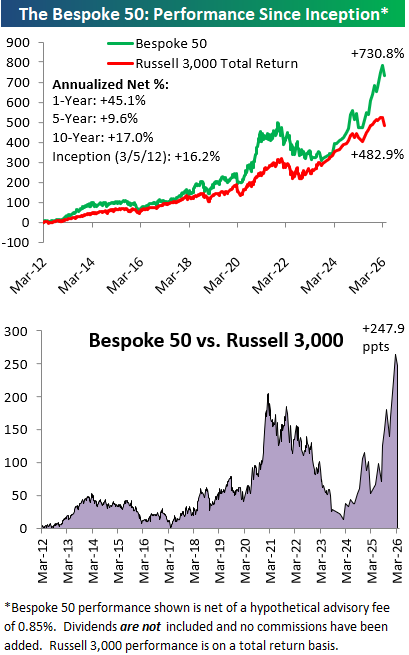

The Bespoke 50 Growth Stocks – 3/26/26

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. There was one change to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. With Bespoke Premium, you’ll receive a number of daily market updates from us along with our weekly newsletter and a portion of our investor tools. With Bespoke Institutional, you’ll receive everything that’s included with Premium plus additional daily macro analysis and more stock-specific research.

To see all 50 stocks that currently make up the Bespoke 50, simply start a two-week trial to Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated monthly on Thursdays unless otherwise noted. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning after publication. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

The Closer – Chart Check, 50-DMA Stops, S&P Streaks – 3/26/26

Log-in here if you’re a member with access to the Closer.

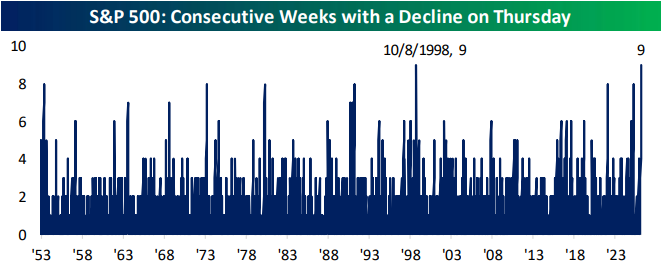

- Thursdays have been the weakest day of the week for the S&P 500 over the past decade, and 2026 has no exception with nine consecutive weeks of Thursday declines.

- Over the past 50 trading days, the Energy sector has seen some of the highest consistency of daily gains on record.

- A hypothetical strategy of only owning the S&P 500 when it has been above its 50-DMA has underperformed a simple buy and hold strategy for decades.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!