Democrats Expected to Keep Senate Control

President Joe Biden currently has the worst pre-mid-term approval rating since President Truman in 1950. A multitude of factors, including inflation, the botched withdrawal from Afghanistan, weakening economic data, age, and a lack of definitive action on campaign promises have all contributed to the President’s unpopularity. Although Americans are generally dissatisfied with the President, betting markets still project a nearly two-thirds chance that Democrats retain control of the Senate (chart below from electionbettingodds.com). The only two previous Presidents that saw approval ratings lower than Biden’s heading into mid-terms (since the start of WWII), Roosevelt in 1942 (third term) and Truman (first term) in 1946, ended up in the mid-terms losing twelve and five senate seats, respectively. In fact, only five Presidents have seen their party’s position in the Senate improve or remain flat since the start of WWII in a mid-term election cycle. In these five cycles, the sitting President averaged an approval rating of 57.2%, which is 19.2 percentage points higher than that of Biden.

Although only 20% of Presidential terms since the start of WWII have seen their party gain Senate seats during mid-terms, subsequent sessions of congress following these election cycles passed some significant legislation. The 88th Congress (under the Kennedy/Johnson administration) passed the Civil Rights Act of 1964, which prohibited discrimination on the basis of race, sex, religion, ethnicity, or national origin. In addition, that session of congress banned the discrimination of pay in regards to sex, and the 24th amendment was passed (which banned states from making the right to vote in federal elections conditional). The 92nd Congress (under Nixon) removed the dollar from the gold standard and established Title IX. The 116th Congress under Trump passed the CARES act, which helped the country recover from the pandemic and funded vaccination initiatives.

Regarding equity market returns, in the five mid-terms where the sitting President’s party gained Senate seats in a mid-term election year, the S&P 500 has averaged a gain of 3.1% between the election date and year-end, posting gains three out of five times. Click here to start a two-week trial to Bespoke Premium and receive our paid content in real-time.

The table below summarizes every mid-term election year since the US entered WWII, For each cycle, we show the number of seats gained or lost by the President’s party, the S&P 500’s YTD performance as well as the YTD change in the 10-year US Treasury yield. In terms of economic data, we also included a look at the y/y change in CPI and the Unemployment Rate (through September), and then finally Gallup’s Presidential Approval Rating. Although one might assume that a strong stock market boosts the President’s party in the Senate for the mid-terms, the equity market was down on a YTD basis heading into mid-terms in three of the five years highlighted above. However, the average y/y change in CPI was just 2.7% and only above 5% once. For the sake of comparison, y/y headline CPI as of the end of July currently stands at 8.5%. In terms of approval ratings, every other President who saw a gain in Senate seats in a mid-term election year had the approval of a majority of Americans, whereas nearly two-thirds of Americans currently disapprove of the President. In those mid-term years when the President had an approval rating below 50%, the average loss of Senate seats for the President’s party was five, and the only one to pick up Senate seats was Trump (+2) in 2018. Given this backdrop, the possibility of Democrats keeping their effective majority in the Senate would seem unlikely, but with less than three months until Election Day, the betting markets say otherwise. Click here to start a two-week trial to Bespoke Premium and receive our paid content in real-time.

Chart of the Day: The Great American Summer of Falling Gas Prices

Bespoke’s Morning Lineup – 8/22/22 – Looking Ahead to Jackson Hole

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You are always a student, never a master. You have to keep moving forward.” – Conrad Hall

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It’s another weak showing for the bulls this morning as investors assess the upcoming Jackson Hole Fed meeting and grasp to come up with what could be a positive takeaway for financial markets. Risk assets have had big summer rallies and Powell and Company have no interest in being seen as cheerleading the gains, so it is widely assumed that the tone will be hawkish. It’s a quiet day on the data front, as the only economic report on the calendar is the Chicago Fed National Activity Index for July which actually came in better than expected at +0.27 versus expectations for a reading of -0.25.

In what looks like a textbook example of a bear market rally grinding to a halt right at resistance, the S&P 500’s attempt to take out its 200-day moving average (DMA) proved extremely unsuccessful in its first and only attempt last week. The bulls cut out early Friday and still appear to be on vacation heading into the new week as the S&P 500 appears to be bookending the weekend with declines of over 1% on each side. Rallies can’t go on forever, so the pullback shouldn’t surprise anyone, but if the bulls don’t get back on the field soon, the S&P 500’s chart will only look increasingly worse.

The S&P 500 snapped a four-week winning streak last week, and most sectors contributed to the decline. Leading the way lower, Communication Services and Materials each pulled back over 2%. In the process, Communication Services moved back into the down 25% YTD range and is one of only two sectors that is no longer overbought. Besides these two sectors, five others pulled back over 1% last week, so the declines were broad-based. On the downside, defensives attracted investor interest with Consumer Staples and Utilities rallying more than 1%. Along with those two, Energy also managed to rally more than 1% taking its YTD gain back over 46%.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 8/21/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Decarbonization

Germany to Keep Last Three Nuclear-Power Plants Running in Policy U-Turn by Bojan Pancevski (WSJ)

With Russia slashing gas supplies, Germany is facing a long, cold winter, but delaying full shutdown of its last three nuclear plants may help stave off the cold. [Link; paywall]

Can the F-150 Lightning Make Everyone Want a Truck That Plugs In? by Talmon Joseph Smith and David Walter Banks (NYT)

As battery manufacturing scales up in rural Georgia to fill the frames of F-150s, it’s still unclear if the truck buyers in the heartland of US pickup demand will adopt the batteries that they build in their local factory. [Link; soft paywall]

Crypto

Fact-checking SBF’s ‘circle jerk’ by Bryce Elder and Robin Wigglesworth (FTAV)

FTX founder and crypto advocate Sam Bankman-Fried recently went on a long Twitter rant about the allegedly circular nature of “tradfi” financial flows. This post is a useful corrective of some of the misrepresentations. [Link; registration required]

The Crypto Geniuses Who Vaporized a Trillion Dollars by Jen Wieczner (NYMag)

Borrowings running near $3bn led to an unprecedented collapse in monster crypto firm Three Arrows Capital this year, fueling a substantial portion of the subsequent collapse in those markets more broadly. Here’s the inside story. [Link; soft paywall]

Tragedy

Should It Be Easier to Take Away a Driver’s License? by Alissa Walker (NYMag)

Why so many Americans who have proven they have no business behind the wheel are still causing crashes that kill tens of thousands per year across the country. [Link]

Russia’s Republic of Grief by Nanna Heitmann and Keith Gessen (NYer)

Soldiers fighting for Russia are overwhelmingly from poor, ethnically diverse areas of the sprawling country where economic opportunities are negligible and the military is one of the only ways out. [Link]

Corporate Press Releases

American Airlines Announces Agreement to Purchase Boom Supersonic Overture Aircraft, Places Deposit on 20 Overtures (American Airlines)

Denver-headquartered Boom has taken a deposit for 20 supersonic aircraft from American, with as many as 20 more planes to follow as the startup moves towards a 2026 target test flight for its Overture airliner. [Link]

Illuminating possibility: Duke Energy and Ford Motor Company plan to use F-150 Lightning electric trucks to help power the grid (Yahoo!/PRNewswire)

A Carolinas utility will work with Ford customers to test a program that takes electricity from parked EVs in order to balance the grid during periods of peak demand. [Link]

Student Loans

Biden administration cancels $3.9 billion in student debt for 208,000 borrowers defrauded by ITT Tech by Annie Nova (CNBC)

Student loan balances borrowed by students at ITT Technical Institute will have their remaining balances forgiven in response to findings that the school engaged in widespread and pervasive misrepresentations. [Link]

Comebacks

Adam Neumann Gets a New Backer by Andrew Ross Sorkin, Vivian Giang, Stephen Gandel, Lauren Hirsch and Ephrat Livni (NYT)

The disgraced founder of WeWork has received the largest seed investment in the history of Andreessen-Horowitz, for a company that at this point is nothing more than a vague idea on paper. [Link; soft paywall]

Drought

How We Got Into This Mess on the Colorado River by Jack Schmidt, John Fleck, and Eric Kuhn (Inkstain)

As the flow of water down the mighty Colorado trickles to almost nothing, years of excessive draws on the waterway are catching up with consumption vastly exceeding the flow of water through the river. [Link]

Politics

Conservative push to alter Constitution focuses on primaries by Nicholas Riccardi (AP)

A little-noticed push to re-write the US Constitution via a convention of states has started to gather steam, although the radical and extreme motivations of the movement are far from being realized at this point. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report + Q3 Macro Report

This week’s Bespoke Report newsletter is now available for members.

This week we have published our weekly Bespoke Report plus our quarterly Macro Report by Bespoke Macro Strategist George Pearkes.

To read both and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Daily Sector Snapshot — 8/19/22

Bespoke Morning Lineup – 8/19/22 – The 1962, 1970 Comp

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you don’t know who you are, the stock market is an expensive place to find out.” – Adam Smith, The Money Game

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

With August coming to an end soon and what has historically been the worst month of the year for the stock market — September — on deck, this morning we looked for years similar to 2022 that saw strong S&P 500 gains in the first two months of Q3 even though the index was still down big YTD.

Only two other years since WW2 really fit the bill. Both 1962 and 1970 saw 7%+ gains in the first two months of Q3 with the S&P still down more than 10% YTD through August. Below is a chart showing the YTD % change throughout the year in 1962, 1970, and so far in 2022. The patterns look quite similar, and it’s noteworthy that 1962 and 1970 were both mid-term election years for first-term Presidents, just like 2022.

In September 1962, the S&P fell 4.8%, but after that weakness, the index surged higher in Q4. In September 1970, the S&P rallied 3.3% and continued to gain sharply in Q4 as well. In both 1962 and 1970, the S&P was higher from the end of August through year-end. Investors would certainly take a repeat of that this year!

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Total Return vs Price Change Spreads

As we mentioned in today’s Chart of the Day, there can be a wide spread between total returns and price change based on dividend yield. Although it doesn’t always make financial sense for a company to pay dividends, they can certainly magnify returns all else equal. Click here to start a two-week trial to Bespoke Premium and receive our paid content in real-time.

The table below outlines twenty S&P 500 stocks that have seen a high percentage of their returns over the last twenty years come from dividends. The average stock on this list has seen over 80% of their gains over the last two decades come from dividends alone. Although the average stock on this list has only seen a price gain of 61.1% since August of 2002, their average total return when factoring in dividends re-invested has been 278%.

To show you what we mean, below is a chart of price change versus total return over the last 20 years for Altria Group (MO). As you can see, the dividend in this case turns a below average stock into an outperformer. Click here to start a two-week trial to Bespoke Premium and receive our paid content in real-time.

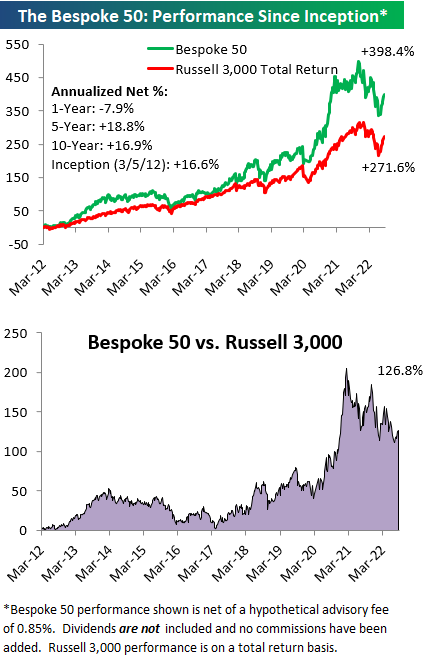

The Bespoke 50 Growth Stocks — 8/18/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were three changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.