Chart of the Day: Welcome December

Bespoke’s Morning Lineup – 12/1/25 – Back to Gravity

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Many people are busy trying to find better ways of doing things that should not have to be done at all. There is no progress in merely finding a better way to do a useless thing.” – Henry Ford

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a zero-gravity rally on Friday that pushed the S&P 500 into positive territory for the month and extended the S&P 500’s monthly winning streak to seven, equities are rediscovering gravity to start December as futures on the major averages all trade lower. The Nasdaq is poised to open down nearly 1% while the S&P 500 faces a 0.7% decline. Even with equities falling, treasury yields are also higher as the 10-year ticks up 3 bps to 4.05%. Crude oil is up just over 1% as OPEC+ announced plans to maintain output levels rather than raise them, and gold is back near $4,300, gaining about 0.8%. The big loser on the day, though, is Bitcoin. With a decline of over 6%, the largest crypto is on pace for its worst day since March, and part of the weakness could be related to reports that Strategy (MSTR) could potentially be forced to sell some of its holdings to fund its dividend.

The weakness started in Asia as the Nikkei fell close to 2% as JGB yields continue hitting levels not seen since before the Financial Crisis, as expectations for a rate hike later this month solidify. In China, stocks went the other way with the Shanghai Composite rallying 0.7%, even as November Manufacturing and Non-Manufacturing PMIs remained in contraction territory.

In Europe, the losses have been more uniform as the STOXX 600 falls 0.5% as Manufacturing PMIs for the economic bloc and individual countries missed expectations. The biggest loser on a country basis is Germany, as the DAX declines more than 1.5% as defense contractors have been especially weak on reports of progress in the Russia-Ukraine war talks.

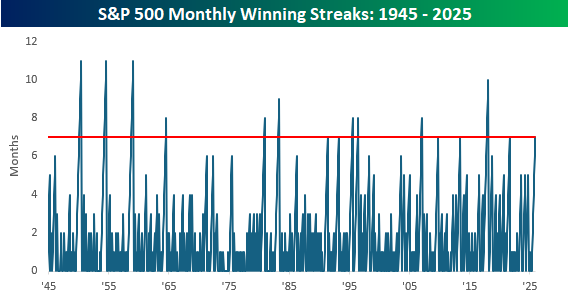

As mentioned above, the S&P 500’s winning streak extended to seven in November, and that’s the longest streak of gains for the index in more than four years (August 2021). Since the end of WWII, there have been 15 other seven-month winning streaks, with the longest being eleven. Believe it or not, that happened three times, all of which were all in the 1950s. So, while history always talks about the roaring twenties, don’t forget about the fantastic fifties.

Outside of those three eleven-month winning streaks in the 1950s, the only other streak that extended into the double-digits was the 10-month streak that kicked off President Trump’s first term in office, ending in January 2018 (seventh month was October 2017). Getting back to the most recent streak, the seven months ending in August 2021 were followed by a sharp decline of 4.8% the following month, and weak returns thereafter.

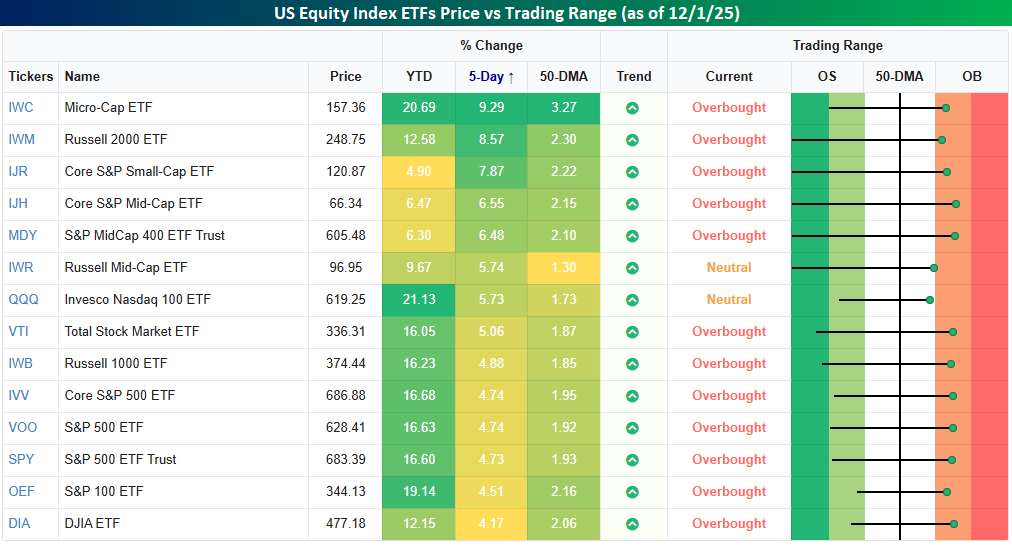

Last week, right before Thanksgiving, we pointed out that the S&P 500 and other major US equity indices had quickly gone from oversold to neutral. In the two trading days since then, the rally kicked into another gear with little selling resistance (as evidenced by Friday’s rally), and all but two of the major equity index ETFs in our Trend Analyzer snapshot have moved into overbought territory. The only exceptions are the Russell Mic-Cap ETF (IWR) and the Nasdaq 100 (QQQ), and while they may not be overbought, they still rallied over 5% in the five trading days through last Friday’s close (from close on 11/20).

Of all the ETFs shown, every one of them was up at least 4% in the trailing five trading days. While large-cap ETFs lagged with gains of less than 5%, small caps had a day in the sun with the Russell Micro Cap ETF (IWC) surging 9% while the Russell 2000 ETF rallied over 8.5%. While usually not the case in recent months, this rally has been one where big gains came in small packages.

Brunch Reads – 11/30/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

The Chatbot Big Bang: ChatGPT launched three years ago today, as a free public demo meant to collect feedback, but it immediately blew up far beyond that. Within a week, it had more than a million users, and by early 2023, it became the fastest-growing consumer app ever. People were drawn to it because it could do everyday tasks like explain things clearly, draft emails, help with homework, debug code, and outline reports, all in plain conversational language. It was the first time the general public had hands-on access to an AI model that felt genuinely useful on day one. ChatGPT was to AI what Netscape Navigator was to the internet.

Since then, ChatGPT has gone through multiple iterations, each making it faster, more accurate, and more capable. Millions now use it for work: companies build workflows around it, customer service teams draft responses with it, researchers use it to summarize huge documents, and marketers use it to create content at scale. Coding has changed, too, as developers lean on ChatGPT for troubleshooting, boilerplate, and idea generation, making software work noticeably faster. The education world hasn’t been the same either. Students rely on it for explanations and study help, while teachers have had to rethink assignments and plagiarism rules.

The ripple effects across the tech industry have been huge. ChatGPT’s popularity pushed nearly every major company to accelerate its own AI tools. It also sparked the boom in open-source models and made “AI integration” a priority in almost every software product. At a broader level, ChatGPT moved AI from an abstract, futuristic concept into something people actually use daily.

AI & Technology

How the Internet Rewired Work—and What That Tells Us About AI’s Likely Impact (WSJ)

In the late ’90s, many expected the internet to either erase jobs or create new ones right away, but most of the change happened inside the jobs people already had. A few routine roles dropped off fast, while most work adjusted bit by bit as digital tools became part of normal work and new support roles formed around them. The article suggests AI will likely follow that same path, with changes spreading through tasks and teams over time instead of a sudden hit to entire occupations. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

Daily Sector Snapshot — 11/28/25

Q3 2025 Earnings Conference Call Recaps: Kohl’s (KSS)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Kohl’s (KSS) Q3 2025 earnings call.

![]()

Kohl’s (KSS) is a retailer serving over 60 million primarily low-to-middle-income customers through 1,100+ stores. Offering a mix of national brands and exclusive private labels like FLX, the company acts as a bellwether for middle-class discretionary spending. The partnership with Sephora has notably grown into a nearly $2 billion business. In Q3, newly appointed CEO Michael Bender reported improved momentum with comparable sales declining just 1.7%, aided by a 2.4% rise in digital sales and renewed engagement from core credit customers. Its strategy shifted back toward “opening price point” value through private labels to combat inflation fatigue. While inventory management remains strong (down 5%), KSS is anticipating a highly promotional holiday season and headwinds from potential tariffs. The company remains cautious as consumers become increasingly “choiceful” with spending. The company reported its first triple play in four years, resulting in the stock climbing 42.3% on 11/25, and another 6.5% on 11/26 before the Thanksgiving holiday! Since the April lows, the stock has almost quadrupled in value…

Continue reading our Conference Call Recap for KSS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

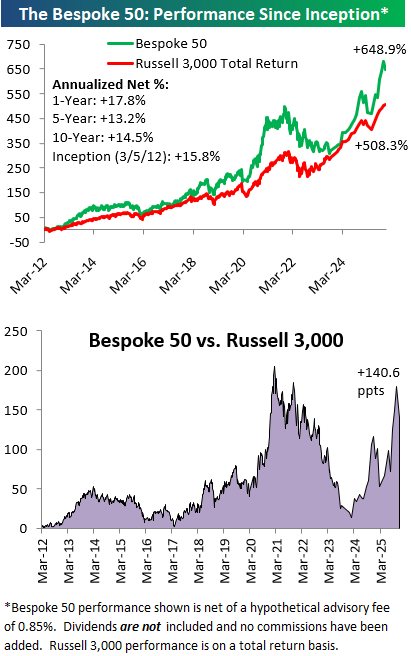

The Bespoke 50 Growth Stocks – November 2025

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. There were 7 changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. With Bespoke Premium, you’ll receive a number of daily market updates from us along with our weekly newsletter and a portion of our investor tools. With Bespoke Institutional, you’ll receive everything that’s included with Premium plus additional daily macro analysis and more stock-specific research.

To see all 50 stocks that currently make up the Bespoke 50, simply start a two-week trial to Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated monthly on Thursdays unless otherwise noted. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning after publication. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 11/28/25 – Going Down to the Wire

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Scientific knowledge advances haltingly and is stimulated by contention and doubt.” – Claude Lévi-Strauss

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Hope everyone in the States had a great Thanksgiving! Futures are halted this morning following a technical glitch on the CME, but equity ETFs tracking the S&P 500 and Nasdaq are indicated to open up 0.34% and 0.51% respectively, on this holiday-shortened day. Small caps are also higher with the Russell 2000 poised to open up 0.33%, although that won’t even be enough to erase the declines seen in the final half hour of trading on Wednesday. Treasury yields are little changed relative to Wednesday’s close, while crude oil and gold are both up about 0.60%. Even Bitcoin isn’t doing much this morning as it hovers just above $91K, although that’s a big improvement from the $86K level it was at on Wednesday afternoon.

Today may not seem like an important day, with many people taking the day off and the market open for only 3.5 hours, but it is coming down to the wire on the S&P 500’s six-month winning streak. Heading into today, the S&P 500 is down 0.40%, which is only slightly more than SPY’s current pre-market gain. So grab your popcorn, and don’t hit the mall just yet!

In most Asian markets, trading activity to close out the week was generally positive, adding to an already positive week. The one exception was South Korea, where the KOSPI fell 1.5%, taking its YTD gain down to just below 2% on the week. In Japan, CPI came in at 2.8% y/y, which was slightly higher than expected. Despite that increase, a BoJ policymaker contended that underlying inflation remains below their 2% target.

In Europe, trading is very quiet so far this morning, with the STOXX 600 up 0.1%, but the index and the individual country benchmarks that underly it are all firmly in positive territory for the week. French CPI data for November unexpectedly declined 0.1% versus expectations for an unchanged reading.

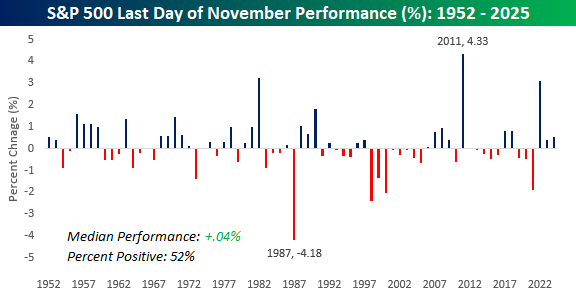

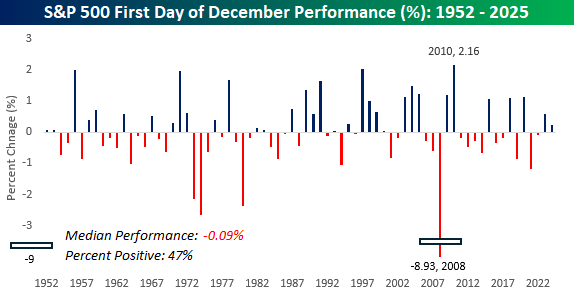

From a market perspective, there was a lot to be thankful for yesterday, especially given where it stood at various points in the year. As we head into the last day of the penultimate month of 2025, we wanted to take a quick look at how the S&P 500 has historically performed on the final trading day of November and the first trading day of December.

Earlier this week, we showed how Black Friday has historically been a positive day for stocks, with the S&P 500 averaging a one-day gain of 0.24%. However, Black Friday isn’t usually the last trading day of the month, and market performance hasn’t been particularly strong on that day. Since the five-trading-day week in its current form began in late 1952, the S&P 500’s median performance on the last trading day of the month has been a gain of 0.04% with positive returns 52% of the time.

The worst year was in 1987, when the market was still reeling from the October crash, and the S&P 500 fell 4.18% while the best day was in 2011 – another volatile year – when the S&P 500 rallied 4.33%. 2022 was the third-best performance for the last day of November when the S&P 500 saw a nice gain of 3.09% in the early weeks of the bull market. That also happened to be the exact day that ChatGPT came into our lives!

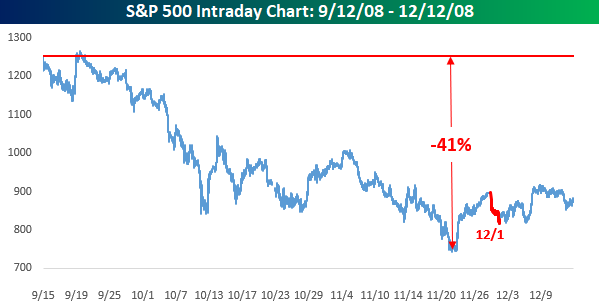

The first trading day of December has also been as bland as an overcooked turkey with no gravy. Since 1952, the S&P 500’s average performance on the first trading day of the month has been a decline of 0.09% with positive returns just 47% of the time. The best performance was a gain of 2.16% in 2010, while the worst was a year earlier in 2008, when the S&P 500 plunged 8.93%. 8.93%! Think about that for a second. We didn’t even fall that much in the latest market pullback (at least not yet), and some people were already acting like it was the end of the world, but in 2008, the S&P 500 fell that much in a single day!

If you’ve been around the block a few times, it may sound hard to believe, but there are now people with driver’s licenses and/or who are applying to college that were born after Lehman Brothers filed for bankruptcy in 2008. Time has a way of dulling memories, especially the bad ones, so for both people who weren’t around during the Financial Crisis and those who were (and just may not have been paying attention), it’s easy to forget how crazy that time was.

That 8.93% decline on the first trading day of December wasn’t just an outlier. In November 2008, the S&P 500 had a daily move of +/-5% on eight of the month’s 19 trading days, and in the three months after Lehman’s bankruptcy, there were 18. That’s more than once every four days!

A better way to show this, though, is to look at an intraday chart of the S&P 500 in the three months following Lehman’s bankruptcy. On the Friday before Lehman went belly up, the S&P 500 closed at 1,251.70. Besides a brief period in the following days, it didn’t reach that level again for a few years, and by Thanksgiving, just over two months later, more than 40% of the S&P 500’s market value was vaporized. Also, you almost need to squint to see it, but that red ‘scratch’ on the right of the November low represents the 8.93% one-day decline from 12/1/08. In the markets, just like life, everything is relative.

Q3 2025 Earnings Conference Call Recaps: Dick’s Sporting Goods (DKS)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Dick’s Sporting Goods’ (DKS) Q3 2025 earnings call.

![]()

Dick’s Sporting Goods (DKS) is the dominant US omnichannel sporting goods retailer, serving athletes and outdoor enthusiasts through an extensive portfolio that now includes Foot Locker. By combining experiential retail concepts like “House of Sport” with the “GameChanger” youth sports technology platform, DKS provides insight into consumer discretionary spending on health, wellness, and sneaker culture. DKS discussed a distinct bifurcation between its core business and its new Foot Locker acquisition. The legacy DKS brand was strong, delivering 5.7% comparable sales growth and raising full-year guidance despite tariff headwinds. Conversely, the integration of Foot Locker requires a “cleaning out the garage” phase. Management announced aggressive Q4 inventory cleanouts, projecting a steep 1,000–1,500 basis point margin contraction for that segment while targeting an inflection point by the 2026 Back-to-School season to make the deal accretive. DKS beat EPS and revenue estimates, and the stock finished the trading day flat on 11/25 after opening almost 3% lower and completely erasing the losses…

Continue reading our Conference Call Recap for DKSby becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Daily Sector Snapshot — 11/26/25

The Closer – Factory Acceleration, Dour Beige Book – 11/26/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at weekly claims and what they say about the labor market (page 1), the mixed signals from factory sentiment indices (page 1), accelerating activity reported in hard manufacturing sector data (page 2), a concerning backdrop from the Fed’s Beige Book (page 2), and a review of how big swings in near-term rate pricing impact equity markets (page 3).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!