Brunch Reads – 12/14/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

The Quantum Question: On December 14, 1900, German physicist Max Planck presented a paper to the German Physical Society in Berlin that solved how energy is emitted by a “blackbody,” an idealized object that absorbs and radiates energy perfectly. Physicists had been studying how hot objects glow, like a piece of metal heated in a fire or the filament inside a light bulb. According to the physics of the day, the math predicted that as objects got hotter, they should release infinite energy at certain wavelengths. That clearly didn’t happen in the real world, so something in the theory was broken.

Planck’s solution suggested that energy doesn’t flow out smoothly, like water from a faucet. Instead, it comes out in tiny, fixed-size packets. He called these packets “quanta.” The key idea was simple: energy could only be released in certain amounts, not just any amount continuously.

This small change made the math work and matched what experiments actually showed. Planck even introduced a new number to describe how big these energy packets are, now known as Planck’s constant. At the time, it didn’t seem especially important. Even Planck himself thought of it as a mathematical workaround, not a deep truth about nature. But that idea turned out to be a big deal. If energy comes in packets, then the universe isn’t perfectly smooth at its smallest levels. That insight became the foundation of quantum physics. Over the next few decades, other scientists built on Planck’s work to explain atoms, light, electricity, and eventually technologies like semiconductors, lasers, and computers.

Markets & Investing

401(k)s Are Minting a Generation of ‘Moderate Millionaires’ (WSJ)

Three straight years of market gains have pushed a record number of retirement accounts past the million-dollar mark. While these savers hit a massive financial goal, many find that seven figures no longer buys the lavish lifestyle they once imagined. It seems the new face of being a millionaire looks less like owning a yacht and more like hunting for grocery deals. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

Annual Outlook — 2026 Global Macro Outlook

Our Bespoke Report – 2026 Global Macro Outlook is now available for Bespoke subscribers. This report is a top-down perspective on the global economy and the big narratives driving financial markets around the world as we head in to the new year.

- The AI boom has been the most pivotal driver of markets in 2025, and we don’t see that changing next year…though there are some key hurdles being set up that promise to make the AI trade much more volatile.

- US labor markets weakened in the middle of the year. We have a clear view on where they head next year, as well as how that will inform the Federal Reserve’s rate path.

- Around the world foreign central banks are starting to hike. That’s despite economic weakness in China. We explore why hikes are coming and the implications for the US and other global markets.

- We also cover commodities, credit, and much more in this snapshot of what lies in wait during 2026.

You can read our 2026 Pros and Cons by signing up for a two-week trial to our Bespoke Premium plan. You can review our membership plans here to help make your decision.

Daily Sector Snapshot — 12/12/25

Q4 2025 Earnings Conference Call Recaps: Adobe (ADBE)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Adobe’s (ADBE) Q4 2025 earnings call.

![]()

Adobe (ADBE) defines the standard for digital creativity and document productivity, serving solo artists to Fortune 500 marketers. Known for powerhouses like Photoshop and Acrobat, the company is aggressively pioneering the “agentic web” with Firefly AI and GenStudio. In ADBE’s Q4 2025 ended 11/28, the company reported record revenue of $23.77 billion, signaling a major inflection point in AI monetization. “AI-influenced” solutions now drive over one-third of their business, with generative credit consumption tripling quarter-over-quarter. Management discussed “agentic experiences,” autonomous interfaces that execute complex tasks, and the pending acquisition of Semrush to secure brand visibility in the age of AI search. With a bullish FY26 forecast targeting $2.6 billion in net new ARR, ADBE demonstrated that integrating third-party models alongside its proprietary Firefly engine is successfully converting AI hype into durable enterprise revenue. ADBE shares rose 2% on 12/11 after posting EPS and revenue beats…

Continue reading our Conference Call Recap for ADBE by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

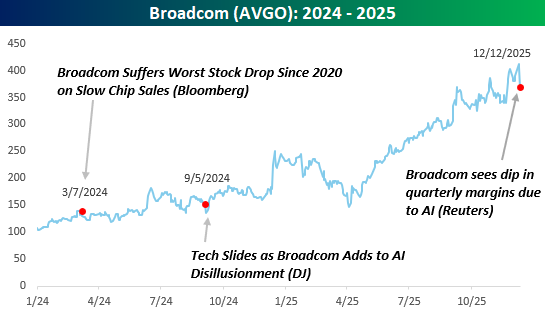

Broadcom (AVGO) Earnings Disappoint

“Broadcom Suffers Worst Stock Drop Since 2020 on Slow Chip Sales” – Bloomberg

“Tech Slides as Broadcom Adds to AI Disillusionment” – DJ

“Broadcom sees dip in quarterly margins due to AI” – Reuters

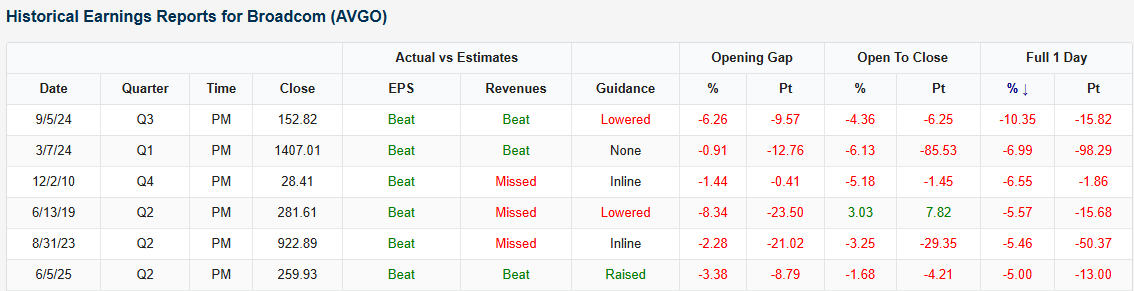

Shares of Broadcom (AVGO) are having a rough go this morning after the company reported earnings after the close yesterday. Despite reporting better-than-expected EPS and sales, as well as raising guidance, the stock is down around 9% this morning as management comments concerning margins and backlog spooked investors. Several analysts have said the comments were misinterpreted, but the stock’s reaction this morning tells another story.

Based on where the stock is trading this morning, today would be just the 7th time since at least 2009 that the stock declined more than 5% on an earnings reaction day, and if it stays at current levels through the close, it would go down as its second-worst earnings reaction day on record.

What’s interesting to note about the performance above, however, is that heading into today, the stock’s two worst earnings reaction days were in 2024. Despite those two clunker earnings reports, heading into today, AVGO has rallied over 275% since the start of 2024, making it the seventh-best-performing stock in the S&P 500!

Getting back to those headlines at the top, all three were written in reaction to AVGO earnings reports, but not yesterday’s. Only the Reuters headline was in reference to the most recent report, but the Dow Jones headline was written in response to its September 2024 report, while the Bloomberg headline pertained to its March 2004 report. In both cases, there was widespread concern over AVGO’s results, but the declines are barely visible on the chart.

Not a Bespoke client? We’d love for you to give our equity research platform, Bespoke Premium, a try. You can sign up for complimentary access for 14 days at this link to start receiving our daily emails today!

Bespoke’s Morning Lineup – 12/12/25 – Disco Fever

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Feel the city breakin’ and everybody shakin’, and we’re stayin’ alive, stayin’ alive” – Stayin’ Alive, Bee Gees

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Make sure to catch Bespoke co-founder Paul Hickey on Making Money with Charles Payne today at 2 PM Eastern on Fox Business.

Saturday Night Fever was released 48 years ago today, and when you think of that movie, “Stayin’ Alive” is the song that comes to everybody’s mind. With the S&P 500 closing at a new high yesterday, we can’t think of a song much better for the current market.

Ever since October 2022, the bull market has been ‘kicked around” by skeptics almost since the day it “was born.” The kicks came from all angles. Throughout the last three years, there have been repeated events that supposedly spelled the end of the AI rally. In the Summer of 2024, it was the unwind of the yen carry trade. Earlier this year, the haphazard rollout of US trade policy caused a tariff tantrum and raised concerns that Brand USA had lost its luster. Now, the fact that the Fed is cutting rates and rates at the long end of the curve aren’t falling has some arguing that the Fed has lost control.

With all these events and the scary headlines that accompany them, we can “understand the New York Times effect on man” and the potential to scare investors out of the market. Time after time (wait, that’s a Cyndi Lauper song), it felt like the market was “breaking and everybody shakin’”, but after the smoke cleared, that wasn’t Tony Manero on the dance floor striking the Disco Finger. No, that was the bull market hitting new highs and “ah, ah, ah, ah, stayin’ alive, stayin’ alive”.

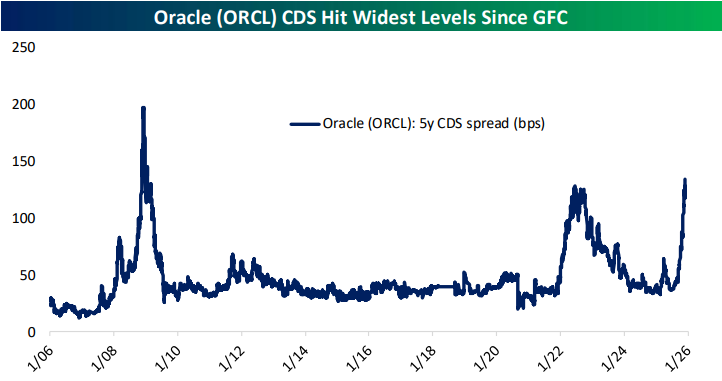

The Closer – Oracle Credit Spreads, Trade, Postings – 12/11/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a dive into the surge in Oracle (ORCL) credit spreads in addition to an update on Fed appointments and some earnings recaps (page 1). We then pivot the latest jobless claims data (page 2) followed by trade balance figures (pages 3 and 4). We close out by recapping the latest job postings data from Indeed (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q3 2025 Earnings Conference Call Recaps: Vail Resorts (MTN)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Vail Resorts’ (MTN) Q1 2026 earnings call.

![]()

Vail Resorts (MTN) is the world’s premier mountain resort operator, managing 42 destinations, like Vail, Whistler Blackcomb, and Park City, across three continents. It revolutionized the industry with the Epic Pass, stabilizing revenue against weather volatility by locking in skiers before the season starts. With millions of global guests, MTN provides insight into high-end leisure travel and the economic impact of climate variability on outdoor recreation. On the earnings call, management reiterated full-year guidance despite a “slow start” due to snowfall down nearly 60% in key western regions. While pass units fell 2%, revenue grew 3% thanks to pricing power and a mix shift toward premium unlimited products. CEO Rob Katz discussed aggressive lift ticket discounting, specifically a new 30% discount for 30-day advance purchases, to capture price-sensitive vacationers who missed pass deadlines. The company is also modernizing marketing by moving spend from traditional email to social and influencer channels. Finally, MTN confirmed its “Resource Efficiency Transformation” is outpacing targets, expecting over $100 million in annualized savings to offset inflation and tariffs impacting its $215–$220 million capital plan. The company missed EPS and revenue estimates, but investors overlooked that news and focused on a more optimistic outlook as the stock rallied as much as 8% on 12/11…

Continue reading our Conference Call Recap for MTN by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

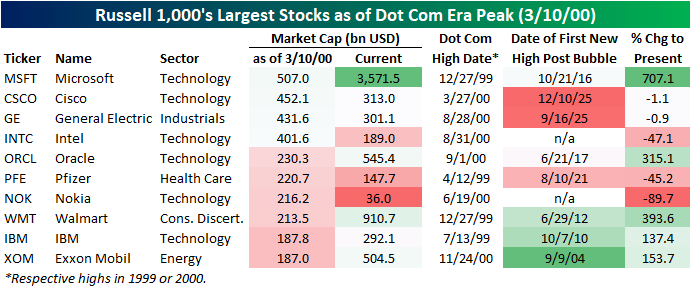

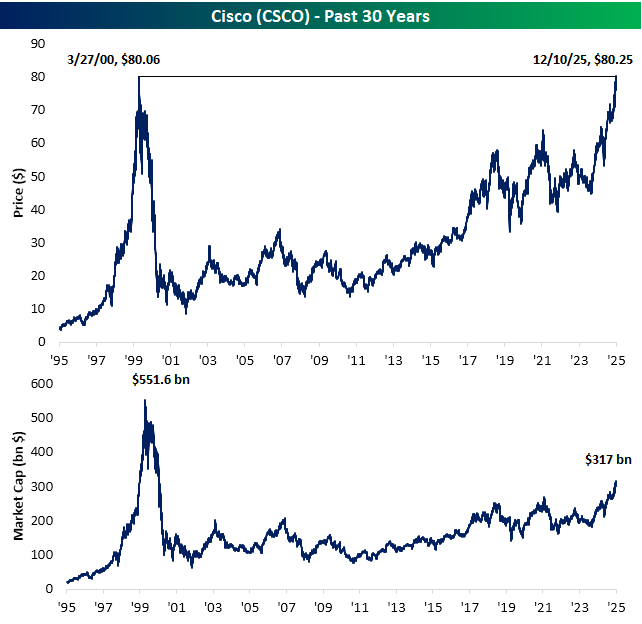

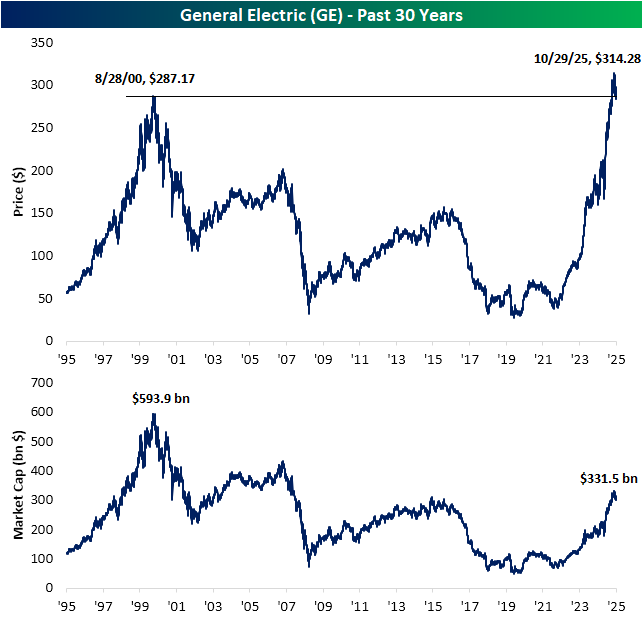

Cisco (CSCO) Returns to Dot Com Highs

At yesterday’s close, something happened that hasn’t in over a quarter of a century: Cisco (CSCO) closed at a record high. As shown below, the stock’s Dot Com era peak of $80.06 had stood in place for more than 25 years. While a hypothetical investor who bought right at the 2000 peak may finally see their share price in the green, we would note that the company’s valuation as of yesterday’s close is far smaller than it was back then (a $317 billion market cap versus $550 billion in 2000).

Cisco is not the only mega-cap of yesteryear to have recently touched fresh records. Back in September, General Electric (GE) finally eclipsed its August 28, 2000 high of $287.17. The stock continued to rally up through late October when it stalled out at $314.28 and today is back in the $280 price range. Again, like CSCO, General Electric may finally be in the green on a price basis, but its market cap remains a couple hundred billion dollars less from where it was in the year 2000. In fact, it’s not even back to levels it stood at during the Financial Crisis. This comes as GE has undergone a number of restructurings, divestures, and the likes in the past couple of decades. Whereas the company in the 2000s was an enormous industrial conglomerate, today GE is primarily its aerospace business. In other words, it is hard to compare GE of today to GE from 2000.

The Dot Com Era’s peak came in March 2000 when the tech-heavy Nasdaq hit its high. Using 3/10/2000 as the reference point, below we show the 10 largest stocks in the Russell 1,000 from that time. At the top of the list, the name should look familiar given it remains one of the world’s largest companies today: Microsoft (MSFT). This dominant stock has rallied over 700% since its late 1999 high although it had been in the red versus that peak up until October 2016. The next two largest stocks from back then are also the two that most recently returned to prior highs: CSCO and GE. Given this development, there are now only two former top 10 stocks that have yet to return to their 1999/2000 highs: Intel (INTC) and Nokia (NOK).