Bespoke’s Weekly Sector Snapshot — 3/16/23

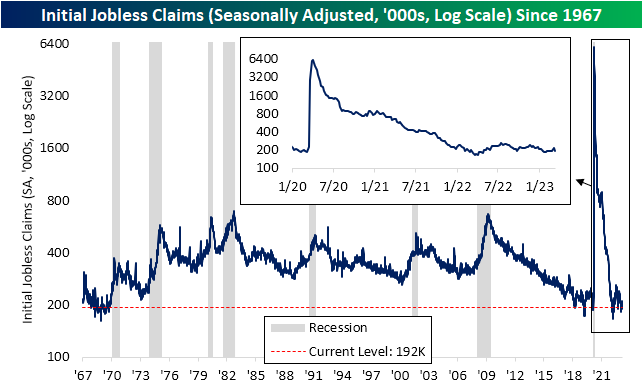

Claims Come in Strong

After disrupting the trend of lower readings last week, this week’s reading on initial jobless claims returned to improvements as the print totaled 192K. That means eight of the last nine weeks have seen claims come in below 200K as the indicator continues to show a historically healthy labor market.

Before seasonal adjustment, claims are sitting at 217.4K. That marked a slight decline from 238.8K the previous week and little change versus the comparable week last year. From this point of the year, based on seasonal patterns claims are likely to continue falling through the spring albeit at a slower rate than what has been observed over the past few months.

Not only were initial claims strong, but so too were continuing claims. The seasonally adjusted number fell back into the 1.6 million range after topping 1.7 million (the highest level since mid-December) last week. Like initial claims, continuing claims remain at healthy levels consistent with the few years prior to the pandemic. Click here to learn more about Bespoke’s premium stock market research service.

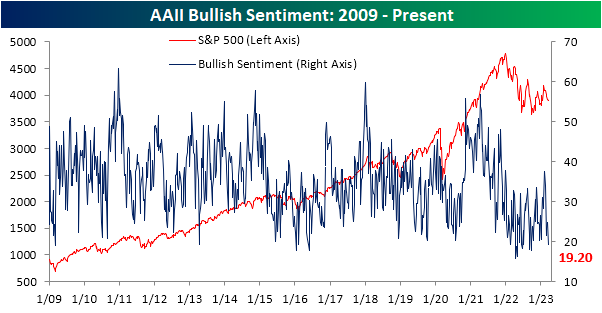

Bulls Back Below 20%

The fallout from bank failures over the past week has put a major dent in investor sentiment. Since the week of February 23rd, optimism has been muted with less than a quarter of respondents to the weekly AAII sentiment survey having reported as bullish. That includes a new low of 19.2% set this week. That is the least optimistic reading on sentiment since September of last year.

The drop in bullishness was met with a corresponding jump in bearish sentiment. That reading climbed from 41.7% up to 48.4%, the highest level since the week of December 22nd. While close to half of respondents are reporting as bearish, that remains well below the much higher readings that eclipsed 60% last year.

Last month saw the end to a record streak in which bearish sentiment outweighed bullish sentiment. However, the bull bear spread has now been negative for four weeks in a row once again. In fact, this week was the most negative reading in the spread since late December.

Factoring in other sentiment readings like the Investors Intelligence survey and the NAAIM Exposure Index—both of which similarly saw sentiment pivot toward more bearish tones this week—our sentiment composite is once again below -1, meaning the average sentiment indicator is reading extremely bearish sentiment. While prior to 2022 such depressed levels of sentiment were not commonplace, it has been the norm over the past year or so. Click here to learn more about Bespoke’s premium stock market research service.

Chart of the Day: $550bn Global Bank Wipeout

Bespoke’s Morning Lineup – 3/16/23 – Better Data Ahead of ECB

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The Federal Reserve, in close consultation with the Treasury, is working to promote liquid, well-functioning financial markets, which are essential for economic growth.” – Ben Bernanke 3/16/2008

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

The quote above could have easily been made this week, but it was actually fifteen years ago today when Bear Stearns, the fifth largest US investment bank, avoided bankruptcy in what was an arranged sale to JP Morgan for $2. While a number of other smaller players in the subprime housing business had already folded, Bear was the first of the major dominoes to go. The emergency takeover of Bear staunched the wound for a time, but it was only a matter of weeks before the cockroaches on bank balance sheets came out from the walls. We all know what happened from there. 15 years to the day later, the question every investor is trying to answer is whether SVB Bank is this generation’s Bear Stearns or just a headline that most will forget all about a year from now.

Futures are mixed this morning as the S&P 500 and Dow are indicated modestly lower while the Nasdaq is in positive territory. European stocks are bouncing ahead of the ECB decision at 9:15 Eastern and on the news that Credit Suisse has taken a $54 billion loan from the Swiss National Bank to improve its liquidity position. US equities aren’t seeing the same lift since they rallied after Europe’s close yesterday on rumors of the SNB loan that European stocks are rallying on now.

The economic calendar is busy this morning as Jobless Claims, Import Prices, Housing Starts, Building Permits, and the Philly Fed all just hit the tape. Jobless Claims on both an initial and continuing basis were lower than expected, Import Prices dropped less than expected, and Building Permits and Housing Starts both came in significantly better than expected. The only report that missed forecasts was the Philly Fed manufacturing which came in at -23.2. Surprisingly, there has been little reaction (so far) in equity futures or the treasury market as attention will now shift to the ECB decision.

What started as a bank run on a regional bank in California last week quickly spread to regional and money center banks around the country and then this week across the Atlantic to European banks. But the weakness in equities hasn’t been confined to just the Financials sector. In the US, the Financials sector is down just over 10% over the last five trading days, but other cyclical sectors have also been pounded as Energy is down 9%, Materials is down 7.5%, and the Industrials sector is down over 5%. Around the world too, equities are down over the last week.

The snapshot below from our Trend Analyzer shows the performance of international regional ETFs. Over the last week, every single one of them is down with declines ranging from a loss of 1.42% for the Global 100 ETF (IOO) to a loss of 7.6% for the Latin America 40 ETF (ILF). Over the last three years, we’ve become all too familiar with the process of disease and virus transmission, and what we’ve seen over the last week is the very definition of contagion. Whether or not it’s just a cold or something worse like the flu will become more apparent in the coming weeks.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 3/15/23

The Bespoke Triple Play Report — 3/15/23

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with above-expectations results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 18 stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Baskets Update — March 2023

Chart of the Day – Fed and Market Diametrically Opposed

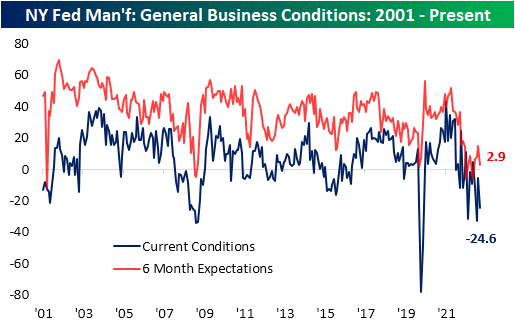

Fall of the Empire Fed

Among the bad news this morning was disappointing economic data in the form of the New York Fed’s Empire Manufacturing report. The report was expected to remain in contraction falling to -7.9 versus a reading of -5.8 last month. Instead, the index plummeted to a much weaker reading of -24.6. Although that is not a new low with even weaker readings as recently as January and last August, the report indicated a significant deterioration in the region’s manufacturing sector, and whereas weather in January was an easy scapegoat for the weakness, that’s not the case for the March report.

Given the large drop in the headline number, breath was equally bad with many other significant declines. Like the headline number’s 5th percentile reading and month-over-month decline, New Orders and Shipments both saw double-digit declines into bottom decile readings. In the case of Shipments, that low reading comes after an expansionary reading last month. Inventories was the only other current conditions index to move from expansion to contraction leaving Prices Paid and Prices Received as the last expansionary categories.

As mentioned above, demand appears weak as New Orders and Shipments are the two most depressed categories from a historical perspective with each index coming in the bottom 3% of all months since the start of the survey in the early 2000s. Six-month expectations are equally low. Unfilled Orders were one of two categories to see a higher reading month over month with the 2.5 point increase much smaller than the move in expectations. Unfilled Orders expectations surged by 12.1 points, ranking in the 95th percentile of all monthly moves on record. That would indicate the region’s firms expect unfilled orders to rise at a rapid pace in the months ahead, likely as a result of weakened sales. That does not mean the area’s firms are expecting inventory build-ups, though. Inventory expectations saw a modest 1.4-point increase month over month in March, but that remains one of the lower readings of the past decade.

The only other current conditions index to move higher month over month was delivery times. Even though it moved higher, the index continues to indicate lead times are rapidly improving and expectations are calling for those improvements to continue.

Next to the dampened demand picture, employment metrics were perhaps the next most jarringly negative. Hiring is falling precipitously with the Number of Employees index hitting a new cycle low of -10.1. Average Workweek also is reaching new lows. At -18.5 it has only been as low during the spring of 2020 and during 2008 and 2009. Click here to learn more about Bespoke’s premium stock market research service.