Daily Sector Snapshot — 12/22/25

Chart of the Day: Dogs of the S&P

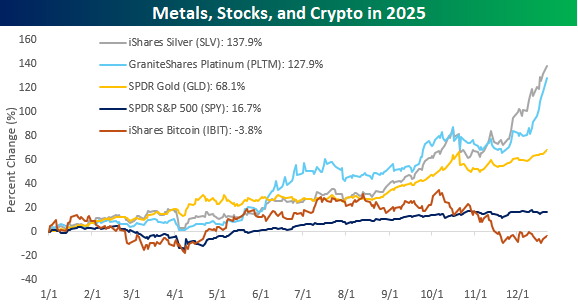

Hi Ho Silver!

Silver is usually thought of as the award for second place, but during the fourth quarter of 2025, it moved firmly into first place in the precious metals race. Based on prices this morning, the iShares Silver ETF (SLV) has now rallied nearly 138% YTD. For much of the first five months of the year, silver trailed gold and/or platinum. In early June, platinum surged past gold and silver for the lead, but in the last few weeks, silver has taken the lead again with a rally that platinum and gold haven’t been able to match.

In the chart below, we have also included the performance of the S&P 500 (SPY) and Bitcoin (IBIT). The S&P 500’s 16.7% YTD gain looks pedestrian relative to the metals, and Bitcoin’s performance has been an embarrassment. Earlier this year, there was so much hope for Bitcoin on the assumption that President Trump would be the most crypto-friendly President that the country has ever seen. It’s been less than a year so far, so there’s still plenty of time, but at this point, Bitcoin hasn’t lived up to the hype.

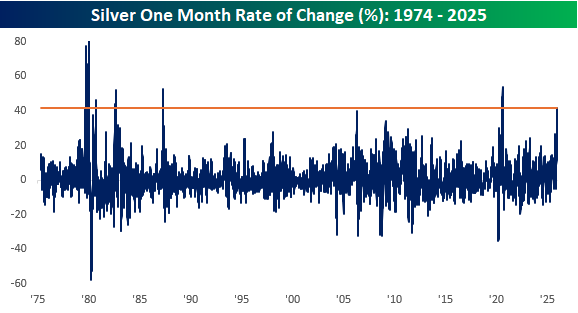

Looking at the chart above, silver prices have really surged over the last month, rallying more than 40%. That’s the largest one-month gain since August 2020. Before that, the only other times, outside of late 1979/early 1980 when the Hunt Brothers attempted to corner the market, that silver experienced similar or larger one-month rallies were in late 2025, early 1987, and September 1982.

Bespoke’s Morning Lineup – 12/22/25 – Christmas Cheer

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I think the one lesson I have learned is that there is no substitute for paying attention.” – Diane Sawyer

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The year is finally starting to wind down as the pace of economic data, earnings results, and analyst actions slows down to a trickle, if at all. This morning, traders are in a buying mood as S&P 500 futures trade 0.4% higher while the Nasdaq is up 0.65%. Bond yields are modestly higher as crude oil jumps 2% following reports that the US has seized another Venezuelan oil tanker. Even with that move, though, WTI still trades below $58 per barrel, so those sub=$3 gas prices should be safe for now.

The real action this morning, though, is coming from the metals markets. Gold and silver are trading to new highs with gains of 1.5% and 2.5%, respectively. Platinum prices are blowing those rallies out of the water, though, surging more than 5% to its highest level since 2008 and within 8% of its record high. Even crypto prices are joining in on the rally to kick off the week as Bitcoin is back above $90K.

Asian stocks had a rough go of it last week, but they’re in the holiday mood to start this week. South Korea led the way higher with a gain of 2.1%, followed by the Nikkei, which rallied 1.8%. Other major benchmarks in the region were also higher, but by less than 1%. Yields in Japan continue moving higher, but the Yen managed to rally.

In terms of holiday cheer, there isn’t much in Europe to start the week. The STOXX 600 is down fractionally, with the UK and France leading the way with losses of about 0.5%.

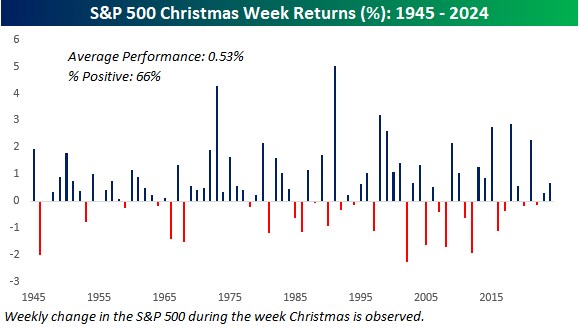

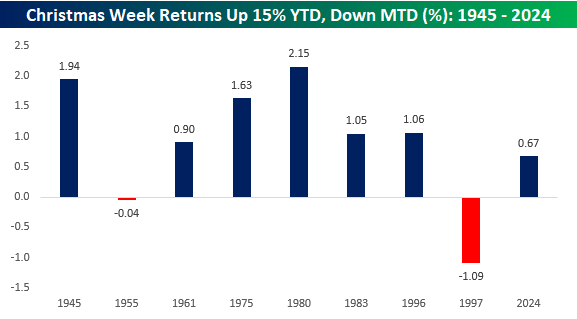

It’s called the most wonderful time of the year, but is it for the stock market? The chart below shows the S&P 500’s historical returns during Christmas week since 1945. For each year, we measure the S&P 500’s performance during the week when the Christmas holiday was observed. For all years since 1945, the S&P 500’s average gain was 0.53% with positive returns 66% of the time. For all one-week periods since 1945, the S&P 500’s average gain was 0.30% with gains 57% of the time, so Christmas week may not be the “most wonderful”, but it’s much better than average. The best Christmas week for the S&P 500 was in 1991, when it rallied just over 5%, while the worst Christmas week was in 2002 (-2.3%).

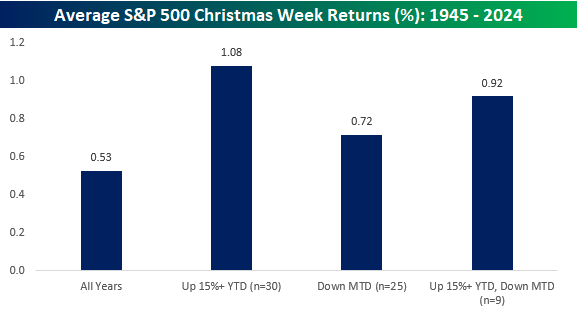

Looking at different scenarios applicable to this year, in the 30 years when the S&P 500 was up 15%+ YTD heading into Christmas week, the S&P 500’s average Christmas week rally was 1.08%, with gains 83% of the time. There have also been 25 years when the S&P 500 was down MTD heading into Christmas week, and in those years, the S&P 500’s performance was more muted at a gain of 72%, with gains just over two-thirds of the time. Together, there have been nine years when the S&P 500 was up 15%+ YTD and down MTD heading into Christmas week, and in those years, the average gain during the week was 0.92% with gains 78% of the time.

The chart below shows each of the nine other years that the S&P 500 was up 15%+ YTD and down MTD heading into Christmas week. The most recent occurrence was last year when the S&P 500 rallied 0.67% during Christmas week. Before that, the next most recent occurrence was way back in 1997.

Brunch Reads – 12/21/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Thirteen Rules and a Ladder: On December 21, 1891, in a YMCA gym in Springfield, Massachusetts, Dr. James Naismith, a PE instructor, found his rowdy group of students bored with the repetitive gym class marching drills and calisthenics they were made to participate in during the harsh New England winter. Naismith needed a high-energy game that could be played within the confines of four walls. After several failed attempts to adapt outdoor sports like football or soccer to an indoor setting, he sat at his desk and drafted thirteen basic rules for a brand-new game.

The equipment for this game was makeshift. Naismith approached the school janitor, Pop Stebbins, asking for two square boxes to use as goals. When Stebbins couldn’t find any, he offered two old peach baskets instead. Naismith nailed these baskets to the lower balcony railing of the gymnasium, which happened to be exactly ten feet above the floor, the height that remains the global standard to this day. Unlike the modern game, there was no specialized ball. The game began with a simple leather soccer ball.

When the eighteen students arrived for class on December 21, Naismith divided them into two teams of nine. The game was far from the fluid, high-scoring spectacle of the modern era. Because the original rules strictly forbade running with the ball, players were forced to stay relatively stationary and pass to teammates to advance. The court was incredibly crowded, and the game quickly devolved into a physical, chaotic scramble. Perhaps most frustratingly, the peach baskets still had their solid bottoms intact. Every time a shot was made, play had to be halted so a janitor could climb a ladder and manually retrieve the ball.

Despite the thirty minutes of play, the very first game ended with a score that seems impossible by today’s standards: 1–0. The lone basket was scored by a student named William R. Chase, who launched a mid-court shot that arched perfectly into the wooden basket. Within weeks, the game of “Basket Ball” spread through the YMCA network, beginning its journey from a Massachusetts gym to one of the biggest sports in the modern world.

Markets & Investing

Inside the Invitation-Only Stock Market for the Wealthy (WSJ)

Wealthy insiders are hoarding the most lucrative investment opportunities by keeping high-growth companies like OpenAI and SpaceX private for much longer than in previous decades. This creates a two-tier system where the general public can only buy shares of older, slower companies while the elite see their net worth skyrocket through exclusive early access. Federal regulators are now debating whether to tear down these barriers for everyday investors or keep them in place. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

Annual Outlook — 2026 Pros and Cons

Our Bespoke Report – 2026 Pros and Cons is now available for Bespoke subscribers. This report covers everything you need to know about the set-up for financial markets and the economy heading into 2026. If there’s ever a “must-read” Bespoke report, this is it!

You can read our 2026 Pros and Cons by signing up for our 2025 All Access Special that gets you the first two months of Bespoke Institutional access for just $20, or start a two-week trial to our Bespoke Premium plan. You can review our membership plans here to help make your decision.

Bespoke’s Morning Lineup – 12/19/25 – Sideways

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“What we obtain too cheap, we esteem too lightly: it is dearness only that gives every thing its value.” – Thomas Paine

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are limping into the last trading session of the week with the S&P 500 indicated up by a few basis points while the Nasdaq is indicated 0.15% higher. The 10-year yield is up 3 basis points, but still below 4.15%, and crude oil is up 1%, but still below $57 per barrel. Gold is essentially flat, putting it on pace for a gain of nearly 1% on the week, while Bitcoin is up over 3% as it attempts to erase some of the week’s sharp losses.

The only economic reports on the calendar this week are Existing Home Sales and UMich sentiment at 10 AM. While options expiration and a rebalancing in the S&P 500 could create some volatility, trading is likely to really slow down next week and into year-end

While it was a down week for stocks in Asia, they closed out the week on a positive note. The Nikkei rallied 1% but still finished down 2.6% for the week. China was up 0.4% and was unchanged on the week, while South Korea rallied 0.7% to soften its decline for the week to 3.5%. As expected, the BoJ raised rates 25 bps to 0.75%, which was the highest level in 30 years. While monetary policy in Japan is tightening, investors in China are speculating that the PBoC will loosen policy by lowering the reserve requirement early in the new year.

In Europe, the tone is less positive this morning as equity markets on the other side of the Atlantic snooze into the weekend. The STOXX 600 is down 0.1%, but still up over 1% for the week. Germany is poised to finish the week basically unchanged, while most other country benchmark indices are up over 1%. Inflation data in the region was mixed as German PPI for November was unchanged versus expectations for an increase of 0.1%, while French PPI increased 1.1%.

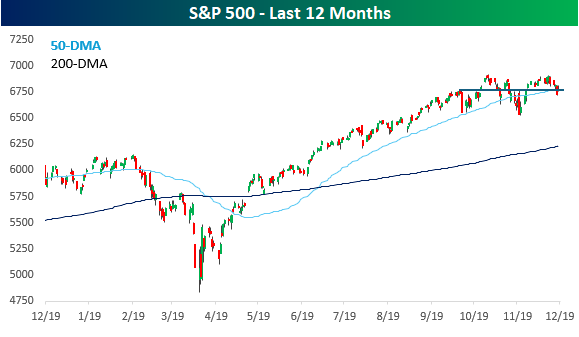

It’s hard to believe that the S&P 500 hit an all-time high a week ago yesterday, and yet as of yesterday’s close, it was barely above its 50-day moving average and essentially at the same levels it was at in early October. As Yogi Berra might say, the stock market is doing great. It’s just not going anywhere.

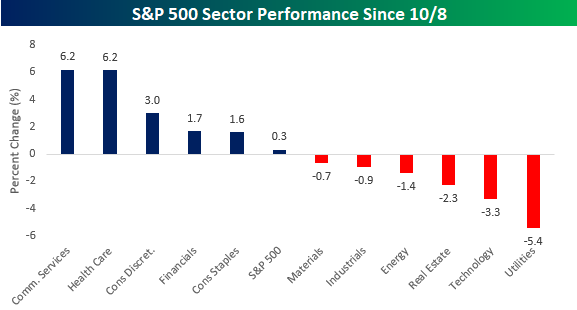

While the S&P 500 hasn’t really gone anywhere, sector performance has been disparate. Communication Services and Health Care are both up over 6%, and another three sectors have outperformed the S&P 500 gain of 0.3%. At the other end of the spectrum, Utilities is down over 5%, but right behind it, Technology has declined 3%. The fact that Technology, which makes up over a third of the S&P 500, has declined over 3%, and the market has treaded water, indicates a broadening of performance. It also illustrates how hard it is for the market to make headway without Technology participating.

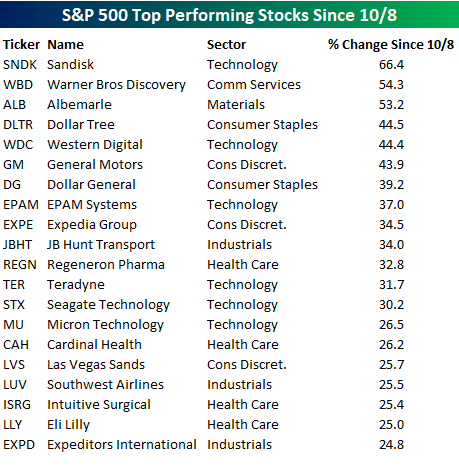

In terms of individual stock performance, of the twenty top-performing stocks in the S&P 500, 19 are up over 25%. Technology is the most heavily represented sector on the list with six, but the strength has been largely isolated to memory stocks, led by Sandisk (SNDK), which has rallied over 60% in just over two months! Besides Technology, six other sectors are represented, including Health Care with four, and Consumer Discretionary and Industrials with three each.

The Closer – ECB, CPI, Memory & Mining – 12/18/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a recap of the ECB decision and other central bank happenings (page 1). Next, we review the latest CPI release (pages 2 and 3). We then switch over to the performance of memory stocks and bitcoin miners turned data center stocks (page 4). We finish with looks at equity ownership (page 5) and the latest earnings reports (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!