The Closer – Venezuela Fallout, FX, Energy Surge – 1/5/26

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a review of the latest ISM data (page 1) followed by a checkup on crude term structure following the happenings in Venezuela this weekend (page 2). We also checkup on emerging market FX (page 3) and the surge in Energy sector stocks (page 4). We finish out with an updated look at the Commitments of Traders report (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 1/5/26

Chart of the Day: Latin America

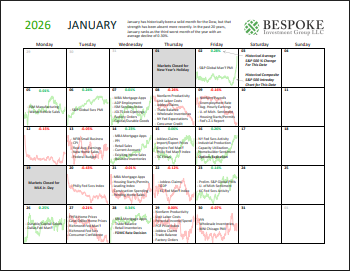

Bespoke Market Calendar — January 2026

Please click the image below to view our January 2026 market calendar. This calendar includes the S&P 500’s historical average percentage change and average intraday chart pattern for each trading day during the upcoming month. It also includes market holidays and options expiration dates plus the dates of key economic indicator releases.Click here to view Bespoke’s premium membership options.

Fed Credibility and Powell’s Performance

In mid-December, we sent Bespoke’s client base a survey to capture the current thinking of experienced investors on markets, the economy, policy shifts, and portfolio positioning heading into 2026 and beyond. Last week, we published our 2026 Investor Sentiment report with a detailed summary of the survey’s results. If you aren’t currently a client, you can start a trial here to view the full report and start receiving everything else we publish on a daily basis.

The Federal Reserve has been front and center in investors’ minds for a few years now, and President Trump’s open call for Chair Powell to resign (or be fired) hasn’t helped. We don’t think the Fed helps its cause, though, with so much “Fedspeak” all the time.

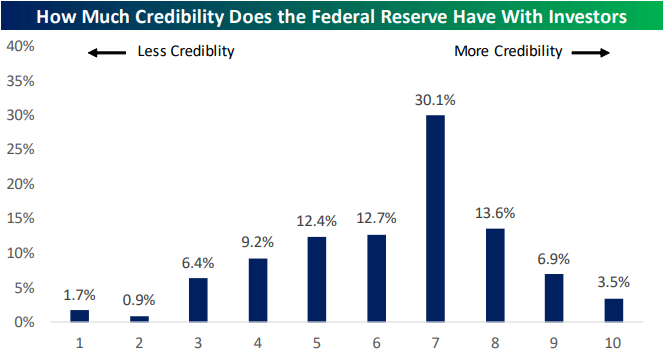

In our 2026 Investor Survey, we asked respondents to rate how much credibility the Fed has with investors on a scale of one to ten with one being no credibility and ten being full credibility.

As shown below, investors still think the Fed has more credibility than not. On a scale of one to ten, seven was the highest response rate at 30.1%, while less than 10% of respondents rated Fed credibility a three or less.

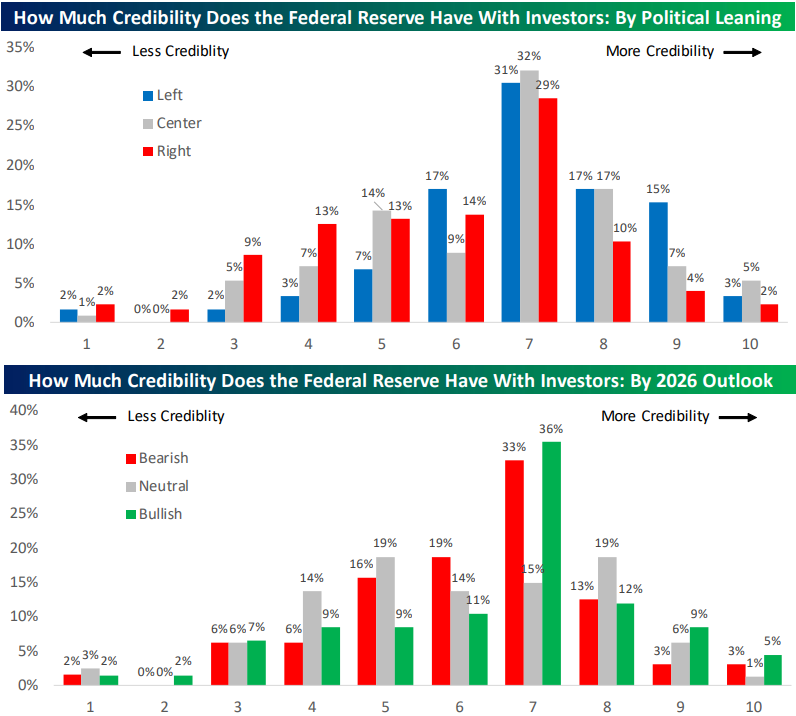

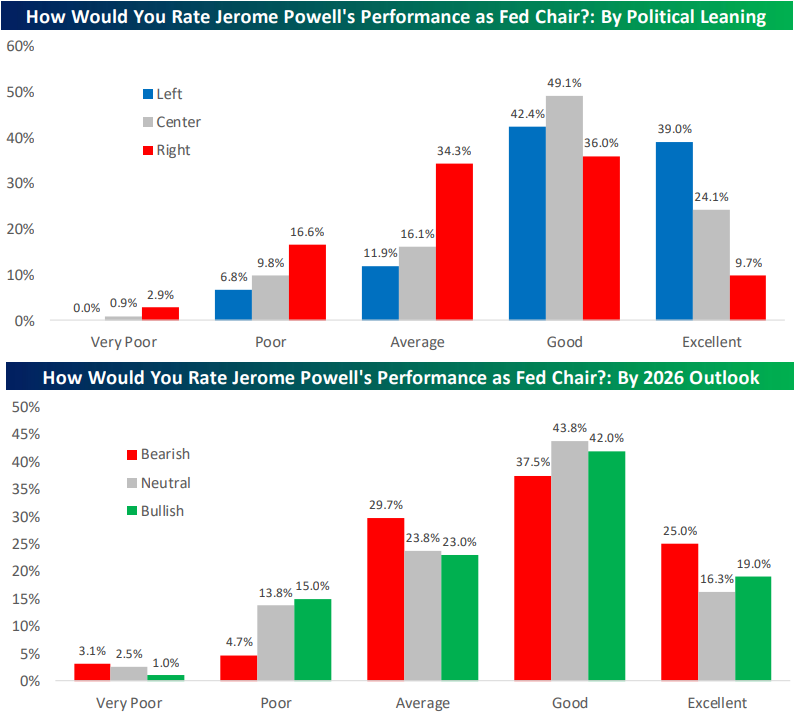

Those that lean left in our survey think the Fed has more credibility than those that lean right, but there’s not too big of a difference by political leaning either way.

Those that are more bearish on markets in 2026 rated the Fed slightly less credible than those that are bullish, although again, the differences are small.

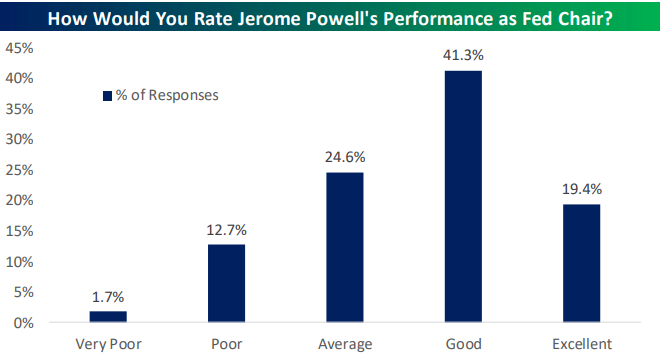

When it comes to Fed Chair Powell specifically, 60.7% of investors rate him as a Good or Excellent Fed Chair, while 24.6% say he’s been average, and just 14.4% rated him as Poor or Very Poor.

Those who lean left are much more likely to rate Powell as “Excellent” than those who lean right, while investor opinions on the stock market in 2026 had little impact on their views of Powell.

While a small minority views Powell and the Fed as captured or no longer having credibility, our survey results show that investors generally think the Fed is doing fine and as not anything to be too concerned about as it relates to market performance.

Not a Bespoke client? We’d love for you to give our equity research platform, Bespoke Premium, a try. You can sign up for complimentary access for 14 days at this link to read our full 2026 Investor Sentiment report and start receiving our daily research emails today!

What’s Your Investment Philosophy?

In mid-December, we sent Bespoke’s client base a survey to capture the current thinking of experienced investors on markets, the economy, policy shifts, and portfolio positioning heading into 2026 and beyond. Last week, we published our 2026 Investor Sentiment report with a detailed summary of the survey’s results. If you aren’t currently a client, you can start a trial here to view the full report and start receiving everything else we publish on a daily basis.

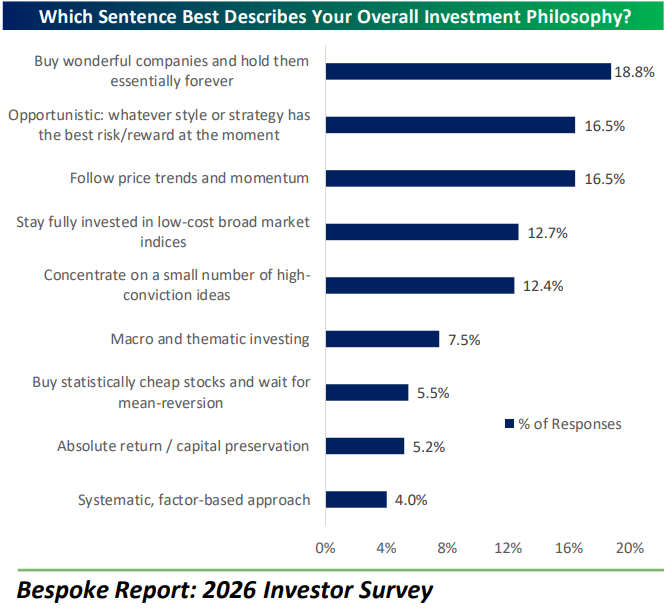

There were a number of fascinating findings across our entire survey about investor positioning, but one of the more basic questions we asked was for participants to “choose which sentence best describes your overall investment philosophy.”

As shown below, while “buy wonderful companies and hold them essentially forever” ranks as the single most popular philosophy, it still captures less than one-fifth of respondents, and no single approach dominates. Opportunistic strategies, trend and momentum following, passive indexing, and concentrated high-conviction investing all cluster closely together, each attracting a meaningful share of investors.

Even approaches like macro and thematic investing, deep value/mean reversion, absolute return, and systematic factor-based strategies are well represented.

We think the dispersion in responses is the key takeaway here: investors don’t converge around one unified framework, but instead express a wide range of beliefs about how risk and return are best managed. Every trade reflects a difference in opinion, time horizon, or risk tolerance, and there is no single “right” way to invest. Different strategies work at different times, and markets function because participants bring varied views and approaches to the table.

This mix of philosophies is what drives liquidity, price discovery, and ultimately “makes a market.”

Not a Bespoke client? We’d love for you to give our equity research platform, Bespoke Premium, a try. You can sign up for complimentary access for 14 days at this link to read our full 2026 Investor Sentiment report and start receiving our daily research emails today!

Bespoke’s Morning Lineup – 1/5/26 – First Impressions Aren’t All They’re Cracked Up to Be

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“What can a first impression tell us about anyone? Why, no more than a chord can tell us about Beethoven, or a brushstroke about Botticelli.” – Amor Towles

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Asian markets were the first to react to the Venezuela news from Saturday, and the response was positive. Japan’s Nikkei rallied 3% while China’s Shanghai Composite tacked on 1.4%, and South Korea surged 3.4%. India was a notable laggard in a sea of green as IT firms in the country declined after some cautious comments regarding the sector from Citi.

In Europe, the tone to start the week has been more subdued. The STOXX 600 is up 0.3% on modestly negative breadth. Germany is leading the way higher with a gain of 0.6% while Spain is fractionally lower.

In the US, S&P 500 futures are up nearly 0.30% while the Nasdaq is doing much better with a gai of over 0.6%. Treasury yields are little changed, and surprisingly, crude oil is only up fractionally. Gold is surging more than 2% while other metals prices are all up by at least twice that. Even crypto is catching a bid as Bitcoin is up over 1.5% and near $93K. If you’re a bull, it’s nice to see a positive reaction to the weekend news on the first real full trading day of the year, but we’ll be watching to see if the gains can be held through the trading session, which is a job the market has had a tougher time of doing in recent weeks.

With the start of every new year, investors tend to pay a lot of attention to first impressions. A strong start to the year raises hopes of a strong year, while weakness out of the gate causes investors to ask whether the market knows something for the year ahead. With the S&P 500 trading higher on Friday, the logic says that it should bode well for the rest of the year. Right?

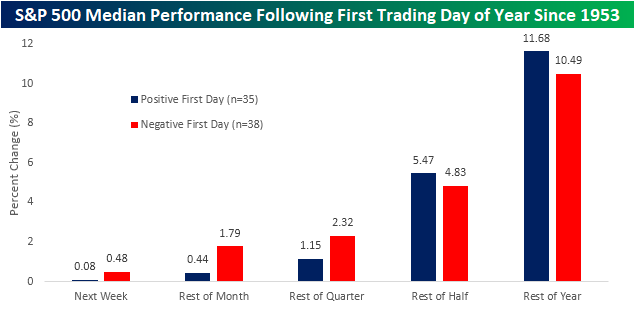

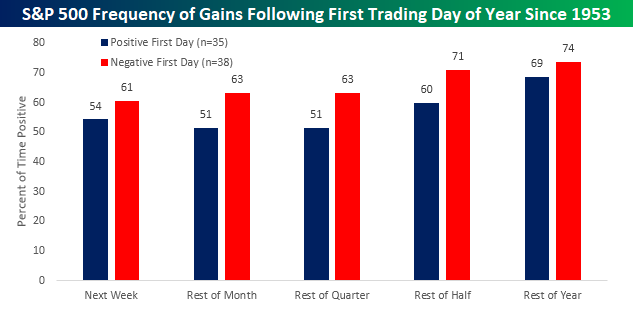

Whether stocks trade up or down to start the year is basically meaningless in the grand scheme of things. Going back to 1953, which was the first full year of the five-day trading week in its current form started, we looked to see how the S&P 500 performed on the first trading day of the year and then compared it to how it performed over the next week, the rest of January, the rest of the quarter, the rest of the half, and the rest of the year.

The chart below shows the S&P 500’s median performance following days when it was positive on the first trading day of the year (blue bars) and negative (red bars). Over the following week as well as the rest of the month and quarter, the S&P 500’s median performance was actually better following a down day to start the year than after a positive start. For the rest of the half and the rest of the year, though, performance was better following a positive start to the year. In both cases, though, the difference in returns was modest.

In terms of the consistency of gains based on first-day performance, the S&P 500 has been positive on a slightly more consistent basis following a negative start to the year, versus a positive start. Once again, though, the differences are modest at best.

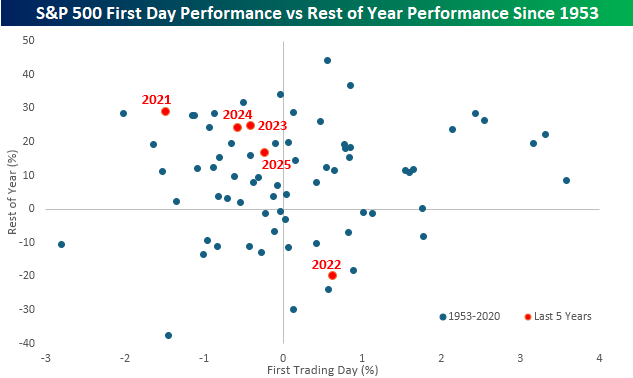

Not only have first impressions had little bearing on how the market performed going forward, but in recent years, it’s been the opposite. The scatter chart below compares the performance of the S&P 500 on the first trading day of the year (x-axis) to its performance for the rest of the year (y-axis). The random scattering of the dots provides another illustration of the lack of correlation.

One exception, however, has been the last five years (red dots). From 2021 through 2025, the S&P 500 traded down on the first trading day of the year four out of five times. 2022 was the only year that the first trading day was positive, when the S&P 500 traded up 0.64% to kick off the year. From the close on that first day through year-end, the S&P 500 dropped 19.95%. In the four other years when the S&P 500 traded down on the first trading day of the year, the S&P 500 rallied anywhere between 16.7% and 28.8% for the rest of the year. You would never base a prediction for the outcome of a baseball game on whether the first pitch was a ball or a strike, so don’t base your outlook for the year on which way the market trades on a day when most people were out of the office anyway. Even if it was higher.

Brunch Reads – 1/2/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Calling Your Own Election: On January 4, 1989, Vice President George H.W. Bush presided over the Joint Session of Congress that formally counted and certified the Electoral College votes of the 1988 presidential election, which confirmed his own election victory. While vice presidents routinely preside over the electoral vote count, only a handful have ever done so knowing the tally would elevate them to the presidency. Before George H.W. Bush, you’d have to go all the way back to Martin Van Buren in 1837, when he confirmed his own victory during Andrew Jackson’s presidency. The only others are Thomas Jefferson in 1801 (John Adams’ VP) and John Adams in 1797 (George Washington’s VP). Jefferson oversaw his tie with Aaron Burr, which was ultimately resolved by the House, leading to the twelfth amendment. Adams confirmed his election under the original electoral system, where the runner-up became VP. It is a scene that captures something special about the American system that allows for the peaceful transfer of lawful power. As such, Bush did not celebrate, posture, or editorialize. He followed the script, showing that the office mattered more than the individual to occupy it.

By the time he reached the podium that day, Bush had built quite the résumé. He was a decorated World War II naval aviator, oilman, congressman, ambassador to the United Nations, envoy to China, CIA director, and two-term vice president during the Reagan presidency. Bush’s presidency would reflect that background. He led the United States through the peaceful end of the Cold War, managed German reunification, and assembled a broad international coalition to repel Iraq’s invasion of Kuwait during the Gulf War. His son, George W. Bush, would go on to become POTUS in the 2000 election against Al Gore. H.W. joined another very short list as one of the only presidents to see his son take the office, joining John Adams, whose son, John Quincy Adams, became the sixth president.

You can click the image below to watch the Vice President confirm the results the election.

Markets & Investing

‘Grift’ ETF Tied to Washington Access in Trump Era Hits a Wall (Bloomberg)

Wall Street’s ETF boom has embraced leverage, crypto, and increasingly niche strategies, but an idea built around monetizing political access has stalled despite clearing regulators. A proposed fund meant to track companies seen as benefiting from Washington ties has been effectively frozen after major exchanges declined to list it, citing concerns that appear tied to reputational and regulatory risk rather than technical rules. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.