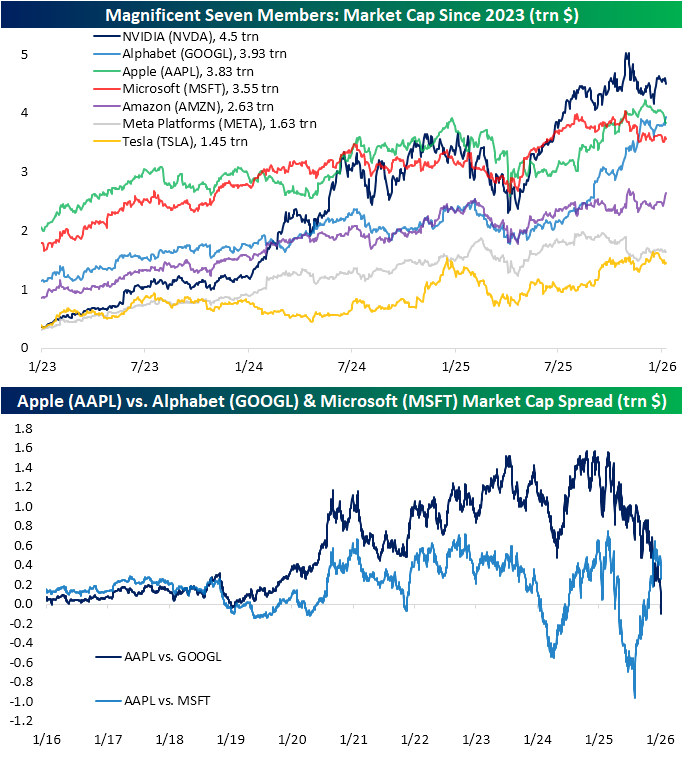

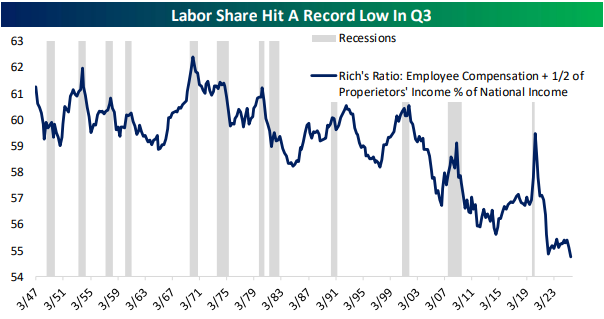

Trillion Dollar Market Cap Changing of the Guard

For the past several months, NVIDIA (NVDA) has held the title of the world’s largest stock by market cap. While NVDA has pulled back from a peak market cap just above $5 trillion in late October/early November to $4.5 trillion today, there’s still a significant gap versus the next largest stock: Alphabet (GOOGL).

GOOGL in the #2 spot is a new development. As shown below, it has typically been either Apple (AAPL) or Microsoft (MSFT) holding that position in recent years, however, both of those stocks have pulled back as GOOGL has pressed to new highs. As shown in the second chart below, this is the first time that AAPL is smaller than GOOGL since January 29, 2019. Additionally, we would note that AAPL is currently larger than Microsoft (MSFT), but that gap has also been narrowing. In the past several years, the two stocks have repeatedly gone back and forth for the larger market cap of the two.

Bespoke’s Morning Lineup – 1/9/26 – Here Comes the Data

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“When the President does it, that means that it is not illegal.” – Richard Nixon

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Asian stocks finished the week on a positive note, and, in most cases, extended their gains for the week. Japan was up 1.6% to finish the week up 3.2%, while China was up even more as its 0.9% rally took the weekly gain to 3.8%. The real action, though, was in South Korea, where the KOSPI rallied 0.8% to finish the week up 6.4%. It’s now up an incredible 8.8% YTD and has traded higher on all six trading days this year. For some perspective on the KOSPI’s gain, it’s now up more YTD than its median annual performance!

Like Asia, European stocks are higher to close out the week, finishing an already positive week on a good note. The STOXX 600 is up 0.6% and nearly 2% on the week, while Germany is on pace to finish the week up 2.8%. Spain is the only major European country lower on the day (-0.4%), and it’s also the biggest laggard for the week. That underperformance, though, comes after it was the best-performing major country in the region last year. This morning’s strength in Germany comes after industrial production in the country unexpectedly grew 0.8% versus expectations for a decline of 0.6%.

In the US, equity futures are on hold with very modest gains ahead of a busy slate of economic data coming at 8:30 with non-farm payrolls, building permits, and housing starts. Then, at 10 AM, we’ll get an update on sentiment from UMich. We’ll also be on the lookout later today for a possible SCOTUS decision related to the Trump tariffs. The consensus view is that they will be struck down in some form, but echoing the sentiment of Richard Nixon, President Trump hopes that since he did it, the court will find the tariffs to be legal.

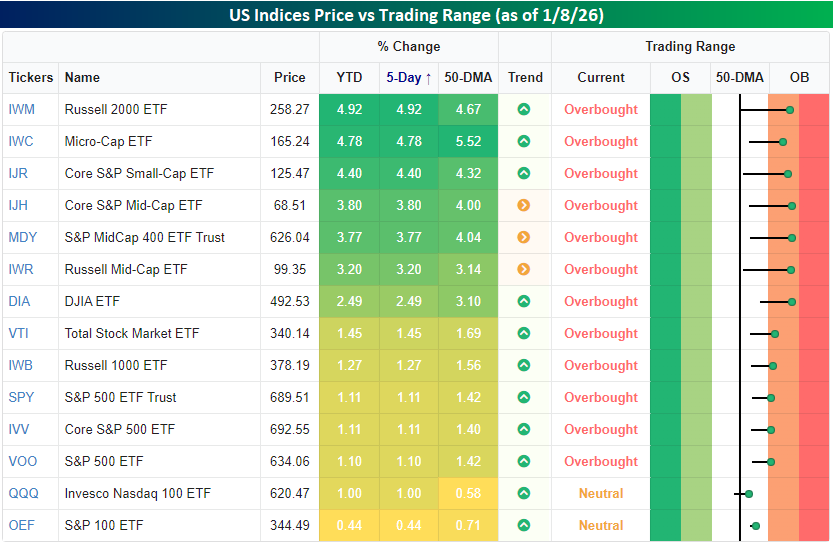

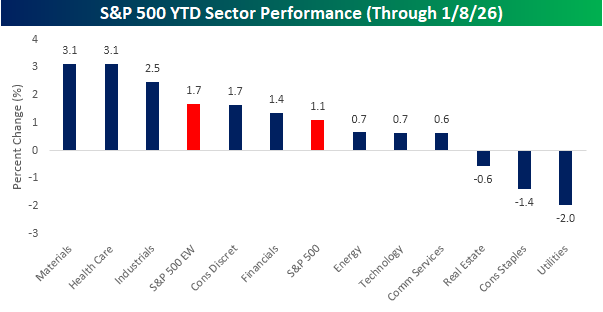

Today is a fun day when it comes to our Trend Analyzer tool, as the YTD performance numbers match the 5-day performance numbers. Interestingly enough, though, since most US indices closed out last year right near their 50-DMAs, the spreads are also very similar to the performance numbers! As things stand after the first full-week of trading, every major index ETF is up YTD, and all but two are overbought. The only outliers are the S&P 500 (OEF) and the Nasdaq 100 (QQQ). At least in the early going, 2026 isn’t the year of the Megacaps. Small caps have been the leaders early on in the year as the Russell 2000 is already up close to 5%.

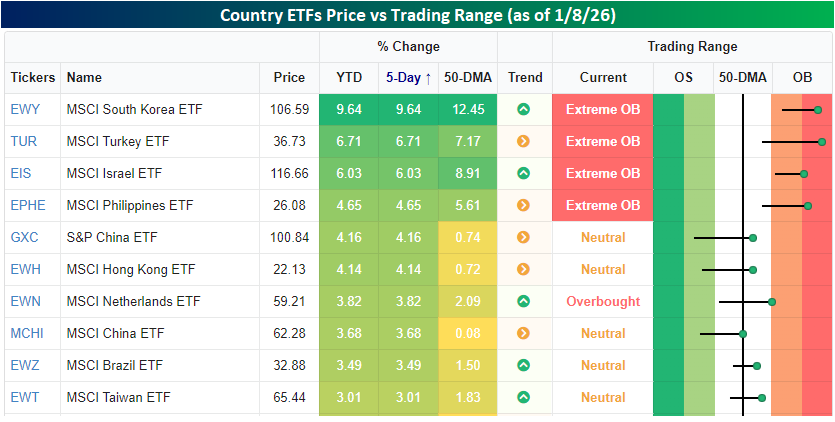

Outside of the US, the ten best country ETFs are listed in the table below. As mentioned above, South Korea has been a standout performer this year, and the MSCI South Korea ETF (EWY) is already up close to 10% YTD. Not surprisingly, the strong gains to start the year have put the ETF into extreme overbought territory, along with Turkey (TUR), Israel (EIS), and the Philippines (EPHE).

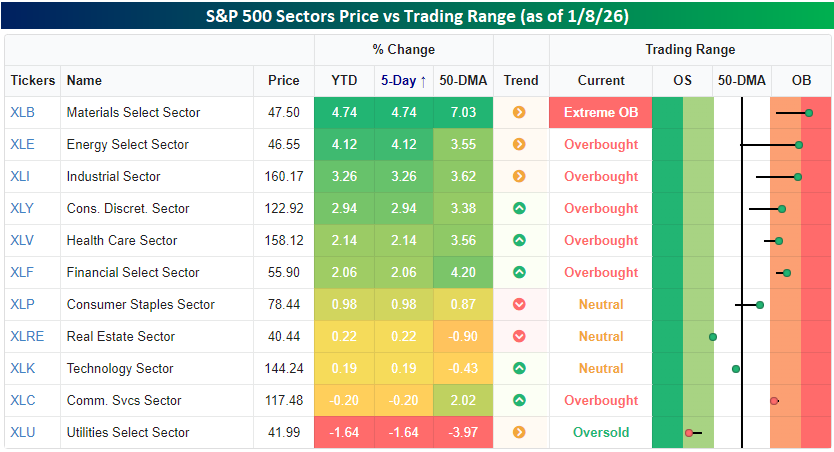

Shifting focus back to the US, this year’s rally so far has been led by commodities as Materials (XLB) and Energy (XLE) have both already rallied over 4%, followed by Industrials (XLI) and Consumer Discretionary (XLY) with gains of over 2.5%. On the downside, Utilities (XLU) have been a major laggard. After a 1.6% YTD decline, it’s the only oversold sector in the S&P 500, and one of just three sectors – Technology (XLK) and Real Estate (XLRE_ being the other two- below its 50-DMA.

The Closer – Productivity, Consumer Strength and Worry – 1/8/26

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we take an in depth dive into the unusually strong mid-cycle strength of productivity (pages 1 – 3). We then checkup on the latest trade data (pages 3 and 4) before pivoting into claims data and some corporate headlines regarding consumer strength (page 5). After that, we review the New York Fed’s Survey of Consumer Expectations (pages 6 and 7) before closing out with a rundown on some housing data from Realtor.com (pages 8 and 9).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Weekly Sector Snapshot — 1/8/26

Q4 2025 Earnings Conference Call Recaps: Constellation Brands (STZ)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Constellation Brands’ (STZ) Q3 2026 earnings call.

![]()

Constellation Brands (STZ) is a leading US beverage alcohol company best known for its high-end imported beer, including Modelo, Corona, and Pacifico, which together make it the largest beer supplier by dollar sales in the US. The company primarily serves US consumers, with an outsized connection to Hispanic drinkers. Beyond beer, the company retains optionality through its equity stake in Canopy Growth (a Canadian cannabis company) and exposure to evolving regulatory dynamics around cannabis and alternative beverages. This quarter’s call to discuss its quarter ending 11/30 centered on margin resilience and consumer pressure. Beer operating margins beat expectations despite volume declines, helped by cost-savings initiatives, pricing actions, and a temporary depreciation benefit. Management flagged margin headwinds from higher aluminum tariffs, mix shifting further toward cans, and seasonally weaker volume. Demand remains soft, especially among Hispanic consumers, with management citing widespread socioeconomic anxiety and state-by-state volatility tied to immigration policy. Pricing remains disciplined at 1–2%, supported by value-oriented pack architecture like seven-ounce formats, while major events like the 2026 World Cup are viewed as meaningful consumption catalysts. Despite a 9.8% YoY revenue decline, EPS and revenue estimates beat expectations, sending shares as much as 6.5% higher on 1/8…

Continue reading our Conference Call Recap for STZ by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: Health Care Heads To The House of Morgan On A Heater

Bespoke’s Morning Lineup – 1/8/26 – Another Whiff

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Tomorrow belongs to those who can hear it coming” – David Bowie

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It looks like a negative start to the Thursday session for equities, as the S&P 500 and Nasdaq both decline between 0.2% and 0.3%, while Treasury yields tick higher with the 10-year yield up to 4.16%. Oil prices bounced 1.5%, but WTI still trades below $57 per barrel. In the metals space, there’s broad-based weakness with gold down about 1%, copper down fractionally, while silver and platinum both fall 4%. After a rally to start the year that took its price over $90K, Bitcoin is back down below $90K. The only data on the economic calendar today are jobless claims at 8:30, along with Nonfarm Productivity and Unit Labor Costs at the same time.

The weakness in US futures follows a weak session in Asia, where Japan, Hong Kong, and India were all down 1%. Despite the declines, South Korea managed to outperform again, finishing unchanged on the session as Samsung Electronics reported better than expected results.

In Europe, stocks are also lower with the STOXX 600 trading down 0.4%, with Spain the only positive outlier. December Business and Consumer Confidence pulled back modestly more than expected as the headline index fell from 97.1 down to 96.7, versus forecasts for a level of 97.0.

We’re four trading days into the year, and already there have been some big individual stock winners. Within the S&P 500, 22 stocks are already up over 10% YTD, while none are down 10%, and only 25 are down by 5% or more. In total, breadth in the market has been positive as 316 of the index’s 500 components are up YTD. The positive breadth is also illustrated by the fact that the equal-weight S&P 500 index is up 1.7% YTD compared to a gain of 1.1% for the cap-weighted index.

At the sector level, five are outperforming the index YTD, while six lag. Leading the way to the upside, Materials and Health Care are both up 3.1%, followed by Industrials with a gain of 2.5%. Technology’s 0.7% gain modestly trails the index, and three sectors – Utilities, Consumer Staples, and Real Estate are all down after four days of trading.

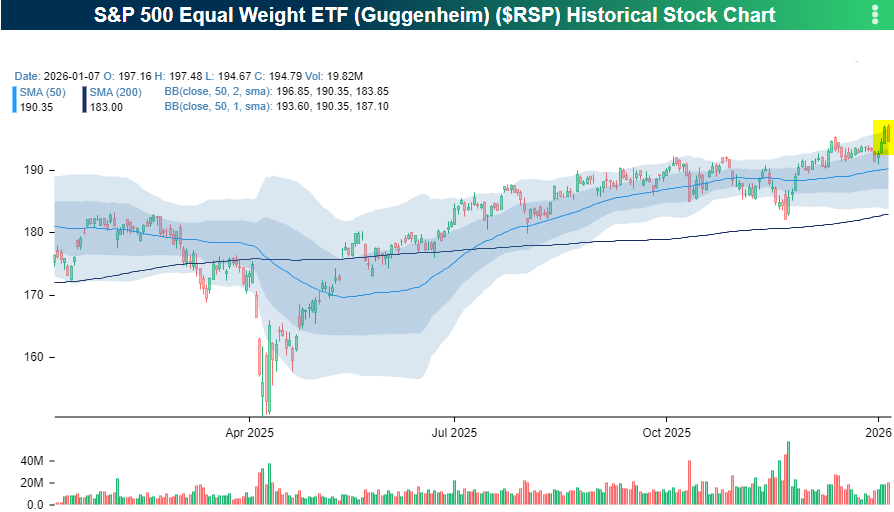

Before yesterday, breadth in the market was even stronger, but while the S&P 500 had a modest decline of 0.34%, the equal-weight index fell more than 1%. That decline also erased nearly all of what was looking like a breakout in the equal-weight index after a multi-month period of sideways trading. Every time it seems like the rally will broaden, Lucy goes in and swipes the football away.

The Closer – Intervention, Basket Rundown, Jobs – 1/7/26

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start note with a discussion on a slug of new credit market issuance and administration interventions on defense and homebuilding stocks (page 1). Next up, we check in on a variety of stock baskets including those based on the themes of: consumer lenders, AI picks and shovels, managed care, trucking, durable goods, and consumer goods (pages 2 and 3). We then turn over to the latest macro data including the ISM Services release (page 4), JOLTS report (page 5), and petroleum stockpiles (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!