Chart of the Day – Bitcoin’s Rebound

Bespoke’s Morning Lineup – 1/14/26 – Nikkei’s Record Start

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“While any number of risks continue, we are bullish on the U.S. economy in 2026.” -Brian Moynihan

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Bespoke’s Paul Hickey appeared on Making Money with Charles Payne yesterday to discuss the markets in the post-Covid world and what to expect in 2026. To view the segment, click on the image below.

After a modestly negative Tuesday, futures are trading on the back foot once again this morning. S&P 500 futures are down 0.36% while the Nasdaq is even weaker, indicated to open down by 0.5%. Oil prices are higher as traders eye the simmering tensions in Iran and anticipate a possible disruption to supplies from the country. That’s also translated to a flight to safety trade in gold and other precious metals. Gold is up 1%, silver is up over 5%, while platinum is up 3%. A few weeks ago, a lot of traders thought these moves were getting long in the tooth, but those teeth now look like fangs. Even crypto assets have caught a bid in recent days as Bitcoin is back above $95K and Ether is up near 3,300.

After yesterday’s tame CPI, we just got PPI along with Retail Sales. PPI was a strange report as the m/m numbers were either inline with or weaker than expected, but the y/y readings came in much higher than expected at 3% compared to forecasts for 2.7%. These are hotter than expected inflation readings, but PPI is a volatile report. Retail Sales, also released at 8:30, were better than expected. The only other report on the calendar is Existing Home Sales at 10 AM, and given the lower mortgage rates recently, we could see some strength in that report.

The pace of earnings is also starting to pick up as Bank of America (BAC), Citigroup (C), and Wells Fargo (WFC) all reported results this morning. All three companies exceeded bottom-line forecasts, while WFC was the only one to report weaker sales. As a result of its revenue miss, WFC is trading down about 2% while the other two stocks are hugging the flat line.

In Asia overnight, it was a mixed session. Japan extended its streak of 1%+ daily moves to seven with a gain of 1.5%. China was down modestly (-0.3%), while South Korea was up 0.7%. In Europe, there’s been little movement so far this morning. The STOXX 600 is basically unchanged as most major benchmarks in the region are marginally higher, but modest weakness in Germany weighs.

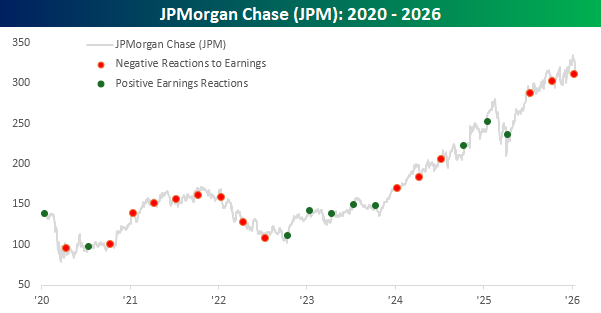

Yesterday’s 4%+ decline in shares of JPM ranked as the eighth most negative reaction to earnings for the stock since at least 2001 and the weakest since April 2024. The stock’s negative reaction to earnings raised some concerns surrounding the stock as well as the broader market, but as we noted in yesterday’s COTD, JPM’s reaction to earnings isn’t exactly a great bellwether for broad market. They’re not even a great bellwether for the stock’s future performance.

The chart below shows the stock’s performance since the start of 2020, and the red and green dots represent each of the company’s earnings reports since then. Red dots indicate days when the stock had a negative one-day reaction to earnings, while green dots indicate positive reactions. Yesterday was the third straight quarter that JPM had a negative reaction to earnings, but as the chart illustrates, the prior two weak reactions weren’t an especially ominous signal as the stock hit new all-time highs following each of them. JPM had a similar streak in 2024, and once again, between each of them, the stock hit all-time highs. From late 2020 through mid-2022, there was another extended streak of eight straight negative reactions, and while the stock held up well early on in that streak, towards the later stretch of that streak, the stock finally rolled over. All in all, though, a weak one-day reaction has tended to be a weak one-day reaction and nothing more.

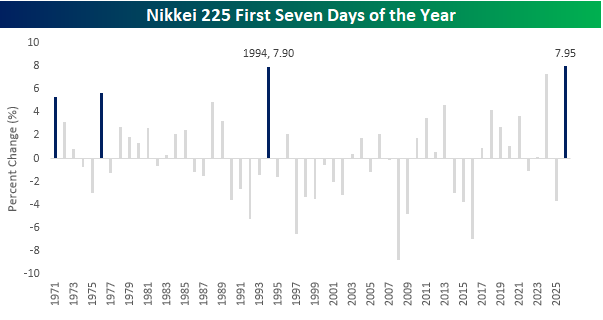

Moving on from JPM to Japan, last night’s rally in the Nikkei extended an impressive run to start the year. After just seven days of trading, the Nikkei is up 7.95%, which ranks as the best start to a year for that index since at least 1971. Before this year, the record was in 1994 when it rallied 7.9% in the first seven trading days. Besides 1994, the only other years that the Nikkei rallied more than 5% in the first seven trading days of the year were 1971, 1976, and, most recently, in 2024.

The Closer – CPI Comes In, Staples Surge – 1/13/26

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start with a rundown of the latest CPI release (pages 1 and 2) followed by a checkup on new home sales (page 3). Next up, we take a peak at the performance of the US dollar and Oracle (ORCL) (page 4) before finishing with a look at the surge in Consumer Staples stocks (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 1/13/26

Q4 2025 Earnings Conference Call Recaps: JPMorgan Chase (JPM)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers JPMorgan Chase’s (JPM) Q4 2025 earnings call.

![]()

JPMorgan (JPM) is the largest US bank and one of the most influential financial institutions globally, spanning consumer banking, credit cards, payments, investment banking, markets, asset management, and commercial lending. It serves tens of millions of households, small businesses, corporations, institutional investors, and governments worldwide. JPM reported revenue up 7% YoY to $46.8 billion, driven by strong markets performance, asset management fees, and card balances. Management emphasized a notable disconnect between weak consumer sentiment and resilient real-world behavior, with debit and credit spending up 7% and 1.7 million net new checking accounts added in 2025. Markets and equities trading were standout performers, while investment banking fees lagged due to deal timing shifting into 2026. The firm addressed major regulatory risks around potential credit card APR caps, warning they could reduce consumer access to credit, and also outlined heavy ongoing investment in technology, AI, branches, and payments, framing higher expenses as necessary to stay competitive. JPM shares slid more than 4% on 1/13 after posting weaker-than-expected EPS and revenue results…

Continue reading our Conference Call Recap for JPM by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Weird Breadth from Small Businesses

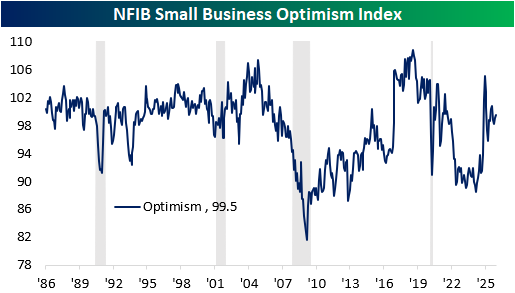

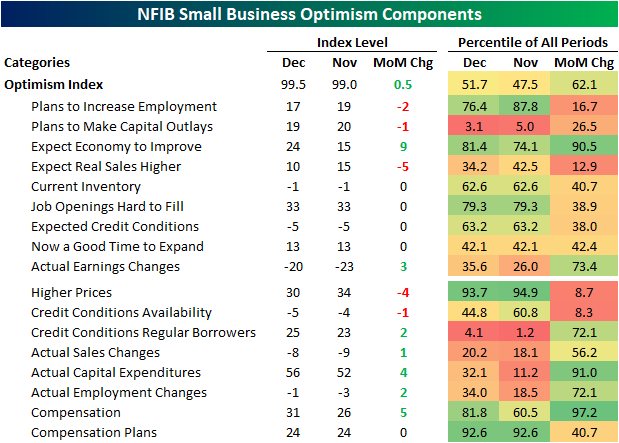

This morning’s release from the NFIB indicated a modest uptick in small business optimism to end 2025. The headline index rose from 99 to 99.5, which is just above the historical median reading.

In the table below, we show each of the nine components that are inputs to the Optimism Index in addition to the eight other indices included with the report. As shown, the increase in the headline number was despite negative breadth among its inputs. Only two indices rose versus three that declined, however, the gainers were oversized including a 9-point jump in expectations for the economy to improve. That was a top decile monthly gain for that index, and brings it into the top quintile of readings historically. As for the indices that are not inputs for the headline number, breadth was much stronger as only two indices fell versus five that rose. That includes multiple strong readings from indices that track observed changes rather than expectations.

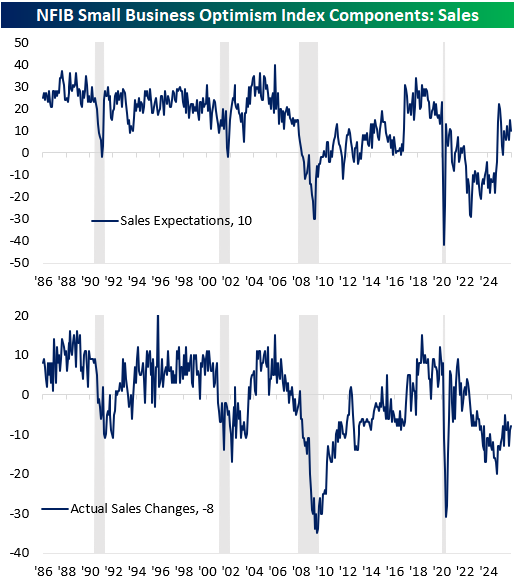

The largest negative impact on overall optimism in December was expectations for real sales to be higher. That index fell 5 points month over month, which is not anything too catastrophic. As shown below, readings remain net positive, and the December print is in the middle of the past several month’s range. Actual sales changes, on the other hand, remains net negative. In other words, more firms continue to report falling instead of rising sales, however, the one point jump in December on top of a four point increase in November marks some improvement in recent months.

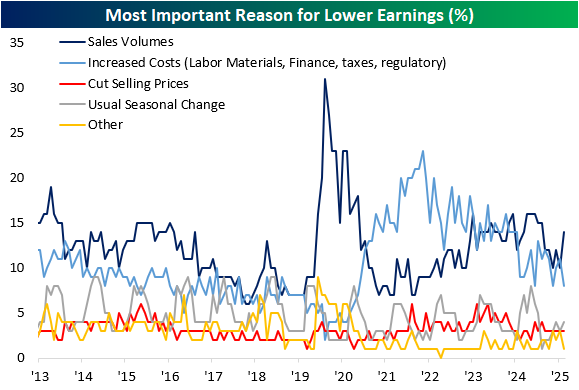

Like actual sales changes, observed earnings changes also remain in net negative territory. Granted, December also saw improvement in this category. For those reporting lower earnings, sales volumes receive the bulk of the finger pointing. That reading ticked up to 14%, which was the highest share of responses since June. Meanwhile, higher costs revisited the low end of the past few year’s range. In other words, it appears weaker demand was the cause for lower earnings.

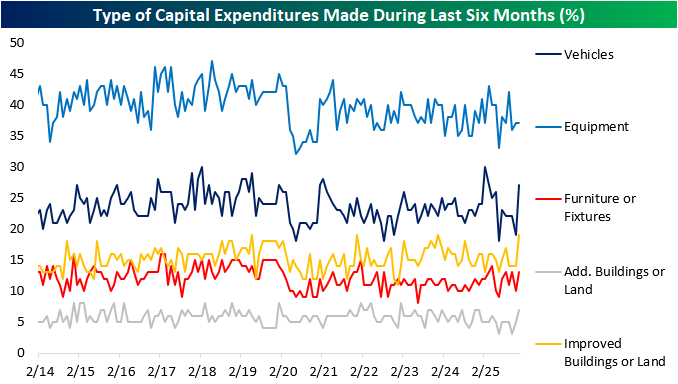

Firms reported an increase in capital outlays in the December report as that reading ended the year at one of the higher levels of the second half. The report offers insights into what companies are putting those expenditures towards, and as shown below, there was an increase in spend across categories save for equipment. Vehicles saw the biggest jump as that category registered the highest reading since the first quarter. Buildings and land typically get a seasonal bump in December, and last month’s reading of 19% was the highest since December 2023, which tied the record high in data going back over a decade.

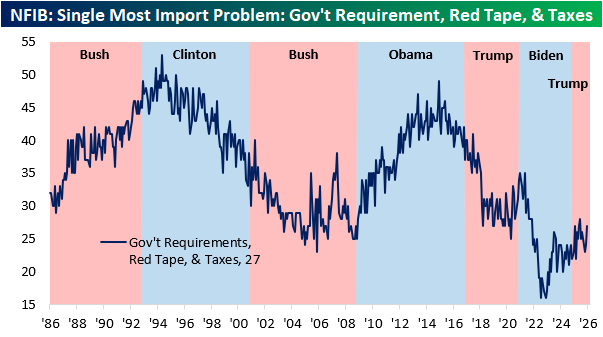

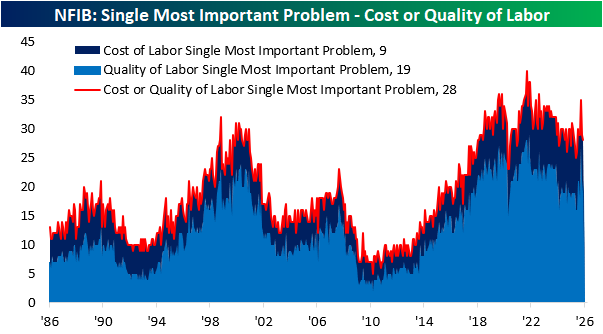

Turning over to the most important problems, the single largest concern is a combination of labor quality and costs. Only one point behind it is government related concerns (taxes combined with requirements and regulations). As shown below, those government concerns have risen steadily over the past few years as inflation has gone by the wayside, and December saw a combined 3 percentage point jump, which is the largest one month increase since the start of the Tariff turmoil of the spring.

As for labor concerns, there was a huge surge in those reporting quality of labor as their biggest issue in October (the reading went from 18% to 27%), but since then, that reading has almost completely reversed as it came in at 19% in December. Cost of labor pulled back one percentage point to 9% in December, which is basically inline with the past year’s readings.

Q4 2025 Earnings Conference Call Recaps: Delta Air Lines (DAL)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Delta Air Lines’ (DAL) Q4 2025 earnings call.

![]()

Delta Air Lines (DAL) is one of the world’s largest global airlines, operating a premium-focused network across domestic and international markets. Beyond passenger flights, Delta generates meaningful profit from its SkyMiles loyalty program (anchored by its American Express co-brand partnership), cargo, and a fast-growing Maintenance, Repair & Overhaul (MRO) business that services third-party airlines. Delta primarily serves business and higher-income leisure travelers, and its results offer insight into consumer travel spending, corporate confidence, premium demand trends, and broader industry capacity discipline. Delta closed 2025 with record revenue of $58.3 billion, a 10% operating margin, and $4.6 billion in free cash flow, using that to reduce debt by $2.6 billion. Management highlighted accelerating demand entering 2026, with January setting an all-time booking record and March-quarter revenue expected to grow 5–7%, driven by premium and corporate travel, while main cabin demand has yet to fully inflect. Loyalty revenue remained a standout, with American Express remuneration up 11% to $8.2 billion. International trends improved sharply, supported by transatlantic and Pacific demand, and Delta announced an order for 30 Boeing 787-10s to boost long-haul margins and premium capacity. After beating EPS and revenue estimates, DAL shares fell as much as 4% on 1/13 on a disappointing outlook…

Continue reading our Conference Call Recap for DAL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day – Watch Taiwan (Semi)

The Year In Headlines: 2025

Bespoke’s Morning Lineup – 1/13/26 – Staples Lead

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There’s nothing more dangerous than someone who wants to make the world a better place.” – Banksy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s a banksy type of morning in the US as some of the largest financial institutions in the world start to release Q4 results. JP Morgan (JPM) missed on the top and bottom line, but there werecharges included in the results, and the stock is trading marginally higher. BNY Mellon (BK) reported better-than-expected EPS and sales, and its stock is fractionally lower. The only other major report of the morning was Delta (DAL), which also reported better-than-expected top and bottom-line results, but its stock is down over 3% in the pre-market. So, it’s not necessarily how you report versus expectations that matters.

Drama surrounding Fed Chair Powell and the subpoenas issued has subsided this morning as Jeanine Pirro softened her stance towards the issue, and the White House says they were not made aware of the actions beforehand. For now, it appears as though the story will be one more in a litany of ‘shocking’ headlines that don’t amount to anything.

The big news of the morning was the December CPI, and after questions surrounded the lower-than-expected November print, many were expecting a hot print for December as the integrity of the data that makes up the report improved. They were wrong. Headline CPI was right in line with forecasts while the core reading came in a tenth weaker than expected on both a m/m and y/y basis. In response to the report, futures experienced a modest bounce and are now firmly in positive territory, while Treasury yields are lower. Crude oil is up another 1% this morning as WTI trades back above $60, while gold is basically flat, as other precious metals trade modestly higher. Finally, bitcoin is higher again this morning and trading back above $92K. The gains also follow reports that a Strategy director purchased 5,000 shares of the company’s stock for just under $800K.

In Asia, it was a mixed session. While Japan returned from Monday’s holiday with a monster 3.1% rally, other indices in the region didn’t fare as well. It’s not often that South Korea is a laggard on an up day, but with a gain of ‘only’ 1.5%, it was up less than half as much as Japan. Hong Kong was up just under 1% while China’s Shanghai Composite fell 0.6%. Japanese PM Takaichi plans to hold snap elections next month to solidify her party’s position in parliament, but outside of that, it was a relatively quiet session for news.

In Europe, stocks are modestly lower across the board, with the STOXX 600 down 0.2%. France is leading the way lower but is still down less than 0.5%, while Germany hangs on to the flatline.

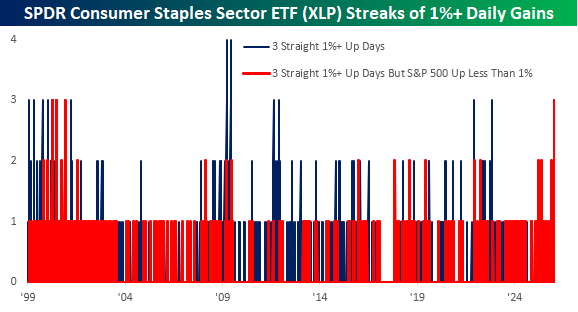

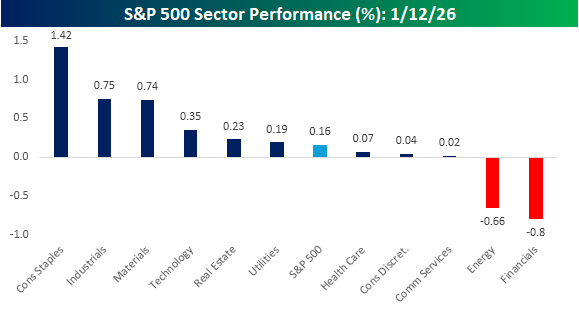

While the banks are the focus of the market’s attention this morning, the standout sector for the last few days has been Consumer Staples, even as the S&P 500 has rallied to new highs. As shown in the chart below, Consumer Staples rallied 1.42% yesterday, which was nearly twice the gain of the next two closest sectors – Industrials and Materials.

Yesterday’s rally for the sector was the third straight day that it has rallied more than 1% in a single session. The chart below shows prior streaks of 1%+ for the SPDR Consumer Staples sector ETF (XLP), and while there have been plenty of other periods where the ETF rallied at least 1% for three straight sessions, the only streaks that were longer occurred in March and June 2009, coming out of the Financial Crisis lows.

What makes the current streak unique, though, is that all three days of gains have occurred on days when the S&P 500 didn’t rally 1%+. It’s one thing to rally 1% when the broader market is also up at least 1%, but to rally that much when the market isn’t up that much is much more significant. As the red bars in the chart illustrate, the only other times that XLP rallied 1%+ for three days in a row when the S&P 500 wasn’t up 1%+ on any of those three days was back in early 2000, right around and after the dot-com peak. Gulp.