Q4 2025 Earnings Conference Call Recaps: Taiwan Semiconductor (TSM)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Taiwan Semiconductor’s (TSM) Q4 2025 earnings call.

![]()

Taiwan Semiconductor Manufacturing (TSM) is the world’s leading pure-play semiconductor foundry, manufacturing the most advanced logic chips used in smartphones, high-performance computing, AI accelerators, automotive systems, and IoT devices. It does not design chips itself, but instead, it builds them at scale for customers like Apple, Nvidia, AMD, and major cloud providers. TSM closed 2025 with blockbuster results, driven by AI demand that management repeatedly emphasized is “real,” not speculative. Q4 revenue reached $33.7B with gross margin of 62.3%, while full-year revenue jumped 36% to $122B. AI accelerators accounted for a high-teens percentage of revenue in 2025, and management guided AI revenue growth at a mid-to-high-50% CAGR through 2029. Capacity remains extremely tight through 2026–27 despite $52–$56B of planned 2026 CapEx, as new fabs won’t meaningfully add supply until 2028–29. TSMC acknowledged margin dilution from overseas fabs and the N2 ramp but reaffirmed confidence in sustaining 56%+ gross margins long term. Management also downplayed AI “bubble” fears, citing direct validation from hyperscalers and persistent wafer shortages as the true bottleneck, not power or data centers. TSM shares rose as much as 7% on 1/15…

Continue reading our Conference Call Recap for TSM by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke’s Weekly Sector Snapshot — 1/15/26

Q4 2025 Earnings Conference Call Recaps: H.B. Fuller (FUL)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers H.B. Fuller’s (FUL) Q4 2025 earnings call.

![]()

H.B. Fuller (FUL) is a global specialty chemicals company focused almost entirely on adhesives, sealants, and coatings used in everyday and industrial applications. Its products are important, but they are small-dollar components in customers’ end products in the spheres of everything from packaging, hygiene, and construction materials to automotive, electronics, aerospace, medical devices, and energy infrastructure. The company offers insight into global manufacturing health, packaging and construction demand, automotive and electronics cycles, and how industrial firms are navigating tariffs, inflation, and regional supply-chain shifts. FUL delivered organic revenue down 1.3%, volumes down 2.5%, but double-digit EPS growth despite weak global manufacturing demand, offset by 1.2% pricing gains across all segments. Engineering Adhesives was the clear standout, posting about 7% organic growth excluding solar, with strong momentum in automotive, electronics, and aerospace. Management reaffirmed that 2026 assumes no macro help, with profit growth driven by self-help actions, including $35 million of pricing/raw material benefits and incremental “Quantum Leap” savings, while deliberately shrinking solar exposure. FUL’s results were mixed as revenue missed and EPS came in better-than-expected, and shares fell about 1.5% on 1/15…

Continue reading our Conference Call Recap for FUL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q4 2025 Earnings Conference Call Recaps: Citigroup (C)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Citigroup’s (C) Q4 2025 earnings call.

![]()

Citigroup (C) is one of the world’s largest financial institutions, serving consumers, corporations, governments, and institutional clients across nearly 100 countries. The bank operates across Services (payments, treasury, custody), Markets (trading and financing), Investment Banking, Wealth Management, and US Personal Banking. Citi closed 2025 with adjusted EPS of $1.81 and adjusted RoTCE (Return on Tangible Common Equity) of 7.7%, with full-year adjusted net income surpassing $16 billion and revenues up 7%, its strongest growth in over a decade. Services continued to anchor results, with cross-border transaction values up double digits and assets under custody and administration up 24%, while Investment Banking posted a record year, highlighted by M&A fees up 84% in the quarter. Management emphasized that over 80% of Citi’s multi-year transformation is at or near the target state. Macro commentary centered around easing global inflation, resilient US consumers, strong tech capex, and improving capital markets activity, balanced against regulatory uncertainty around consumer credit. While reported EPS beat estimates, revenue missed, and shares fell 3.4% on 1/14…

Continue reading our Conference Call Recap for C by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: Wall Street Winning

Bespoke’s Morning Lineup – 1/15/26 – Is That Chirping We Hear?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Nothing makes a man so adventurous as an empty pocket.” – ― Victor Hugo, The Hunchback of Notre Dame

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are higher this morning, with the S&P 500 indicated to open 0.4% higher while the Nasdaq, driven by strong earnings from Taiwan Semiconductor (TSM), looks to open up nearly 1%. After weak reactions to earnings from the major banks over the last two days, Goldman Sachs (GS) and Morgan Stanley (MS) reported better-than-expected results but are experiencing muted to modestly negative reactions in their stocks.

Treasury yields are little changed, but at 4.14%, the 10-year yield is very well behaved. After surging above $62 per barrel yesterday as a strike on Iran seemed like a certainty, WTI is down over 4% and back below $60 this morning. Gold and other precious metals are also pulling back, but by much more modest amounts.

In Europe this morning, the STOXX 600 is up 0.5% as shares of ASML rallied more than 5% and saw their market cap exceed half a trillion dollars. Asian stocks were mixed overnight, with the Nikkei falling 0.4% (it can’t go up every day) while China was down a more modest 0.3%. South Korea, however, bucked the trend and rallied 1.6% (apparently, it can seemingly rally every day).

We just got a flurry of economic data, and the results were all stronger than expected. Both the Philly Fed and Empire Manufacturing reports topped expectations, and jobless claims were lower than expected on both an initial and continuing basis. Initial claims were even below 200K. The only fly in the ointment was Import Prices, which rose 0.1% m/m versus forecasts for a decline of 0.2%. In reaction the reports, yields ticked a little higher, and equity futures improved modestly.

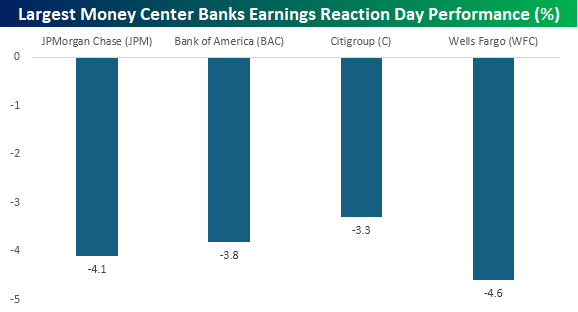

While large brokerage/investment banking-centric firms like Goldman Sachs (GS) and Morgan Stanley (MS) are seeing modest reactions to earnings, the same can’t be said for the largest money center banks, which reported this week. Bank of America (BAC), Citigroup (C), JPMorgan Chase (JPM), and Wells Fargo (WFC) all traded down at least 3% on their reaction days this week. For most, it was their worst earnings reaction day performance in over a year, and for BAC, it was the worst since October 2020!

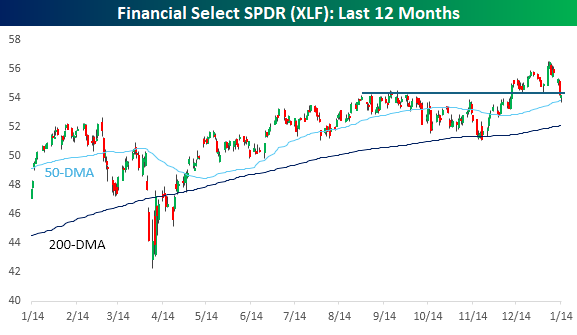

The weakness in the stocks has been a disappointment and a drag on the market this week, but keep in mind that these stocks were trading at record highs last week. They’ve also had to contend with the President’s call for a 10% cap on credit card interest rates. After the initial weakness yesterday, the Financial sector found some support at its 50-day moving average and ended up finishing the day right near the prior highs from last Fall. Provided the weakness eases from here, it’s nothing more than some consolidation.

The major banks are the first companies to report earnings every quarter, so their results and how their stocks react tend to get a lot of investor focus. Therefore, with all four reacting negatively to earnings, it raises the question of whether it’s a flock of canaries warning of bigger problems ahead.

The chart below shows the performance of the SPDR Financial Sector ETF (XLF) since 2000, and the blue dots indicate every time that all four money center banks declined on their earnings reaction days in the same earnings season, while the red dots indicate each time all four stocks declined at least 1%. There have been 14 other times that all four stocks declined on their earnings reaction day in the same earnings season, but there have only been three earnings seasons when all three declined 1%. Of those three, the only time all four stocks declined more than 3% was in April 2020 when the economy was shutdown from Covid! So, it’s uncommon to see all four stocks simultaneously react so poorly to earnings.

The Closer – Tin, Beige Book, Big Data Day – 1/14/26

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a review of the rapid rise of tin prices (pages 1 and 2). We then give a quantitative look at the Beige Book (page 3), and follow up with recaps of all other data of the day including the current account and retail sales (page 4), existing home sales (page 5), and PPI (page 6). We finish out with Brookings Institute estimates for immigration (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q4 2025 Earnings Conference Call Recaps: Wells Fargo (WFC)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Wells Fargo’s (WFC) Q4 2025 earnings call.

![]()

Wells Fargo (WFC) is one of the largest US banks, serving tens of millions of consumer, small business, commercial, and corporate clients across banking, lending, markets, and wealth management. The firm spans consumer banking (checking, credit cards, auto, mortgages), commercial and corporate banking, investment banking and trading, and a sizable wealth and investment management franchise. WFC reported net income of $21.3 billion and ROTCE (Return on Tangible Common Equity) reaching 15%, up from 8% in 2020, while setting a medium-term target of 17–18%. With its asset cap lifted by the Fed, assets grew 11% YoY, loans expanded across consumer and commercial segments, and trading-related assets rose 50% to support client activity. Credit remained solid as net charge-offs fell 16% YoY, consumers showed resilience across checking and payment data, and commercial real estate office losses were described as manageable and non-systemic. The bank guided to roughly $50B of net interest income in 2026, assuming two to three Fed rate cuts, with loan and deposit growth offsetting rate headwinds. WFC missed on the top-line but beat EPS estimates as shares fell as much as 5.5% on 1/14…

Continue reading our Conference Call Recap for WFC by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q4 2025 Earnings Conference Call Recaps: Bank of America (BAC)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Bank of America’s (BAC) Q4 2025 earnings call.

![]()

Bank of America (BAC) is one of the world’s largest financial institutions, serving consumers, small businesses, corporations, governments, and institutional investors through consumer banking, wealth management, commercial banking, investment banking, and global markets. The company operates at an enormous scale, with roughly $3.4 trillion in assets and over $6.5 trillion in client balances. The company reported $7.6 billion in net income (+12% YoY), EPS of $0.98 (+18%), and 7% revenue growth driven by 10% NII growth to $15.9 billion. Management highlighted resilient US consumer spending (+5%), improving credit trends with net charge-offs down to 44 bps, and stabilizing deposit growth, particularly in Consumer Banking. AI and digital initiatives are producing tangible cost savings, including a 30% productivity gain in coding workflows. Investment banking activity improved as tax and tariff uncertainty eased, while management flagged regulatory risks around stablecoins and proposed credit card rate caps. Shares fell roughly 3.5% on 1/14 despite better-than-expected results…

Continue reading our Conference Call Recap for BAC by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below: