Q4 2025 Earnings Conference Call Recaps: Intel (INTC)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Intel’s (INTC) Q4 2025 earnings call.

![]()

Intel (INTC) is a semiconductor leader transitioning into a dual-threat design and foundry company. It produces essential microprocessors for PCs and data centers, alongside custom ASICs and advanced packaging solutions. Intel is the only firm developing and manufacturing leading-edge nodes on US soil, serving massive tech ecosystems and government defense programs. INTC beat earnings expectations, but is struggling to meet a massive surge in AI-driven demand. Management is pivoting capacity away from low-end PCs to prioritize high-margin Xeon server chips, causing a supply trough in early 2026. Despite $13.7 billion in revenue, depleted inventory buffers mean the company is currently “hand-to-mouth” on wafer supply. Investors are focused on the successful ramp of the 18A process and the 14A roadmap, which has already garnered industry-standard PDK status. Other highlights included a $5 billion investment from NVIDIA and a custom ASIC business that hit a $1 billion annual run rate, signaling Intel’s growing role in the specialized AI hardware market. The stock got decimated on 1/23, down 17% on the day…

Continue reading our Conference Call Recap for INTC by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

The Closer – Technicals, 5 Fed, Positioning – 1/26/26

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a look at the S&P 500’s technical outlook in addition to some commentary regarding Medicare and private credit (page 1). We then pivot into the latest earnings (page 2) followed by an update of our Five Fed Manufacturing Composite (page 3). We also review durable goods data (page 4) before closing out with a rundown of the latest moves in positioning data (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 1/26/26

Q4 2025 Earnings Conference Call Recaps: Intuitive Surgical (ISRG)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Intuitive Surgical’s (ISRG) Q4 2025 earnings call.

![]()

Intuitive Surgical (ISRG) is the global pioneer of robotic-assisted surgery, primarily known for its da Vinci surgical systems. The company manufactures advanced robotic platforms, 3D high-definition imaging systems, and proprietary instruments that allow surgeons to perform complex procedures through tiny incisions. By serving hospitals and ambulatory surgery centers (ASCs), Intuitive provides insight into the modernization of healthcare. Intuitive reported revenue climbing 19% to $2.87 billion and annual procedures growing 18%. The call centered on the transition to the da Vinci 5, which now represents over 50% of new placements. While international growth was strong at 23%, pricing intensity and local competition in China remain key headwinds. Notably, ISRG just secured FDA clearance for cardiac procedures on the da Vinci 5, opening a new vertical. However, 2026 guidance was cautious (13–15% growth) due to potential US Medicaid/ACA subsidy changes and a 120-basis-point tariff headwind. ISRG beat EPS and revenue estimates but finished trading on 1/23 slightly in the negative…

Continue reading our Conference Call Recap for ISRG by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q4 2025 Earnings Conference Call Recaps: Capital One (COF)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Capital One’s (COF) Q4 2025 earnings call.

![]()

Capital One (COF) is now the largest US credit card issuer by balances following its $35 billion acquisition of Discover in 2025. It owns one of the world’s few global payment networks, positioning it to challenge the Visa/Mastercard duopoly. The company made a surprise $5.15 billion acquisition of Brex, an AI-native B2B payments platform, accelerating its push into corporate liability and national small business banking. Financially, the results were mixed. Adjusted EPS of $3.86 missed estimates, pressured by a $4.1 billion provision for credit losses and a 41% spike in marketing ($1.9 billion). Management noted that while charge-offs rose to 4.93%, credit is settling out near pre-pandemic levels. CEO Rich Fairbank warned that proposed 10% interest rate caps would “immediately slash credit lines,” potentially triggering a recession. With the earnings miss, COF shares fell 7.9% on 1/23…

Continue reading our Conference Call Recap for COF by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: Growth vs. Value

Bespoke’s Morning Lineup – 1/26/26 – Digging Out

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I skate to where the puck is going to be, not where it has been.” – Wayne Gretzky

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As much of the country digs and/or scrapes out from the snow and ice over the weekend, it’s a very lackluster morning for US equity futures. The S&P 500 looks to open 6 bps lower, while the Nasdaq is down slightly more at 19 bps. It’s worth noting, though, that both indices are well off their overnight lows. Treasury yields have a downward bias, with the 10-year yield trading down to 4.22%. Crude oil is slightly lower at just under $61 per barrel, but natural gas is surging more than 10% as it has nearly doubled in price over the last ten days as the US continues to fall into the grip of a severe cold snap. Everything is hot in the metals space, though, as gold now trades above $5,000 per ounce, while silver rallies 8% and platinum gains another 4%. Crypto continues to sit this rally out, though. While it’s higher this morning, those gains follow weakness over the weekend.

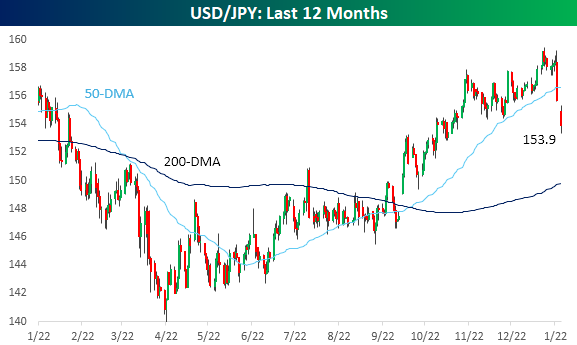

Although the Hang Seng managed a slight gain, most other Asian benchmarks were lower to start the week, although Australia and India were closed for a holiday. The Nikkei declined 1.8%, and even South Korea declined 0.8%. The declines in Japanese stocks came as the Yen followed through from Friday’s rally and rallied another 1% on speculation of a possible intervention on the horizon to halt the long-term slide in the currency (more on that below). Chinese stocks were only down fractionally, but there were some reports of possible disagreements between President Xi and one of his top generals, resulting in the removal of the general and other military members.

There’s not a lot going on in European markets as the STOXX 600 is basically unchanged, but most major individual indices are slightly higher.

On the US calendar, it’s a light day with Durable Goods at 8:30, and there’s no Fedspeak as the Federal Reserve is in its blackout period ahead of Wednesday’s meeting.

The rally in the yen on Friday took the dollar cross below its 50-day moving average for the first time since early October, and today’s rally has extended those gains to take the currency to its best levels versus the dollar since early November.

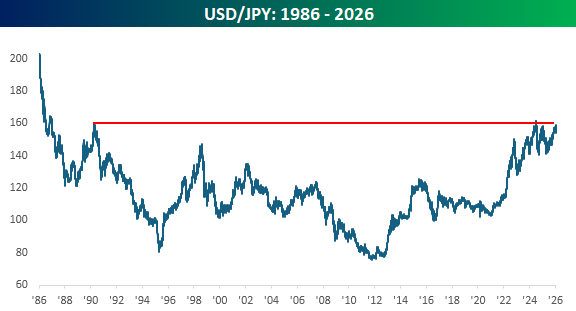

From a longer-term perspective, the rally in the yen has occurred at what is turning into a significant support/resistance level. In more recent history, levels around 160 have acted as support for the yen, and that level also coincides with a peak in the cross (low in the yen) from early 1990. And if you want to get creative, you could even make out what looks like an inverse head and shoulders.

We’ve seen a lot of huge moves in commodities over the last several months, and natural gas has started to get into the act over the last two weeks. Ten calendar days ago, on 1/16, natural gas closed at 3.10 MMBtu. This morning, prices are nearly twice as high, and earlier in the morning, they were double the level of the 1/16 close! Looking at the chart of natural gas and its history in terms of how the commodity has performed following prior short-term spikes, buying natural gas today feels a lot like skating to where the puck is rather than where it’s going. And happy 65th birthday to Wayne Gretzky!

Brunch Reads – 1/25/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Frozen in Time: On January 25, 1924,

in the small Alpine town of Chamonix, France, nestled beneath Mont Blanc, athletes from 16 countries gathered for what was officially called The International Winter Sports Week. It was the humble beginning of what we know today as the Winter Olympics.

The scene was modest by today’s standards. There were no flashing lights, no global TV audience, no corporate pageantry. Just skiers, skaters, and sledders competing on frozen lakes and snow-packed trails, representing nations still recovering from World War I. Events included speed skating, figure skating, ice hockey, Nordic skiing, and bobsleigh. Only later would the International Olympic Committee look back and retroactively designate the Chamonix games as the first Winter Olympics.

As for the winners of the games, Norway took home 17 medals (4 gold), Finland won 11 (4 gold), and Great Britain gathered 4 (1 gold). The US competed in the games, but won just one silver medal in speed skating. Obviously, in the early stages, before these games became as highly competitive as they are today, geography mattered a lot. The Nordic countries clearly carried the weight, while winter sports were still in their early stages in many of the countries competing in 1924.

Markets & Investing

Betting on Prediction Markets Is Their Job. They Make Millions. (NYT)

Prediction markets have turned into a full-time job for a small group of traders who treat real-world events like tradeable assets, using data analysis, obsessive research, and sometimes insider-like signals to find an edge. Platforms like Kalshi and Polymarket now host billions of dollars in wagers on everything from elections to pop culture, creating outsized profits for a tiny fraction of “sharps” while most users lose money. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

Daily Sector Snapshot — 1/23/26

The Bespoke Report — 1/23/26

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium.

Small-caps continued to widen their lead against large-caps this week, which we cover in detail in this week’s Bespoke Report newsletter along with macro coverage and updated earnings analysis. Give the full report a read by starting a trial here.