Bespoke’s Morning Lineup – 1/29/26 – Energized Energy

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You can fool some of the people some of the time — and that’s enough to make a decent living.” – W.C. Fields

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It was only a 0.01% decline, but the S&P 500’s drop yesterday ended a streak of five straight gains. The Nasdaq managed to finish up 0.17%, extending its winning streak to six. This morning, both indices are trading higher, so for the Nasdaq will today be lucky number seven? While Meta (META) and Tesla (TSLA) are doing their part to extend the Nasdaq’s streak, Microsoft (MSFT) is trading the other way after weak margin guidance has that hyperscaler trading down a not so lucky 7% this morning.

Outside of treasuries, the 10-year US Treasury yield is basically unchanged at 4.25%, while the dollar is little changed after a volatile few days to start the week. Precious metals continue to get more precious this morning, with gold up over 4% and breaking through $5,500 per ounce. Silver is up over 5%, platinum is up nearly 5%, and copper is also at a record, trading up close to 7%. For all three metals, their year-to-date gains are leaving equities in the dust.

In Asia overnight, the Nikkei was basically unchanged, but South Korea rallied another 1% as SK Hynix reported strong Q4 results. Hong Kong, China, and India were also higher on the session, while Australia had a marginal decline.

European stocks are mostly higher this morning as the STOXX 600 gains 0.5%, but Germany has been a major outlier with a decline of nearly 1% as earnings results from SAP weigh on the DAX. A January survey of Business and Consumer sentiment came in stronger than expected, showing an unexpected increase relative to December.

With the Federal Reserve behind us, investors will now turn back to earnings and economic data. Earnings this morning have been OK, with EPS and revenue beat rates for the morning coming in at about 67%. The economic calendar is also busy with Non-Farm Productivity, Unit Labor Costs, and jobless claims at 8:30, followed by Factor Orders and Wholesale Inventories at 10 AM.

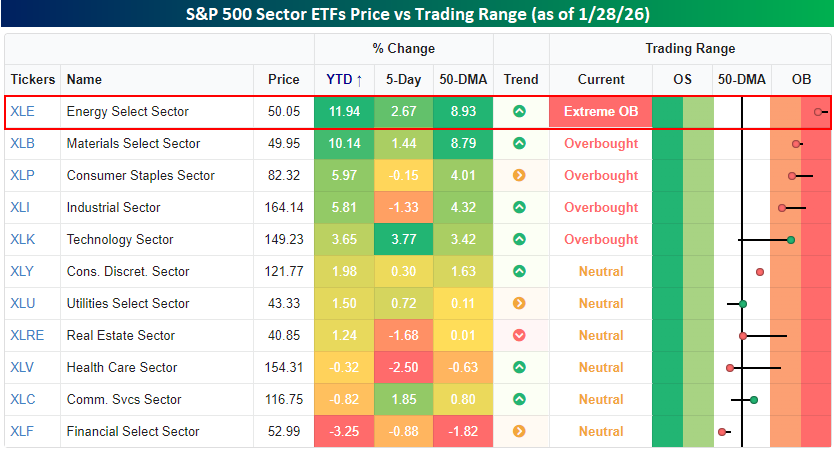

In yesterday’s note, we highlighted the strength in the Energy and Materials sectors and how they were leading all other sectors in terms of year-to-date returns. Through yesterday’s close, Energy and Materials were still leading the performance derby, but Energy is the only sector that remains in ‘extreme’ overbought territory (more than two standard deviations above its 50-DMA). Behind Technology, which has had a run this week, Energy is also the best-performing sector over the last five trading days.

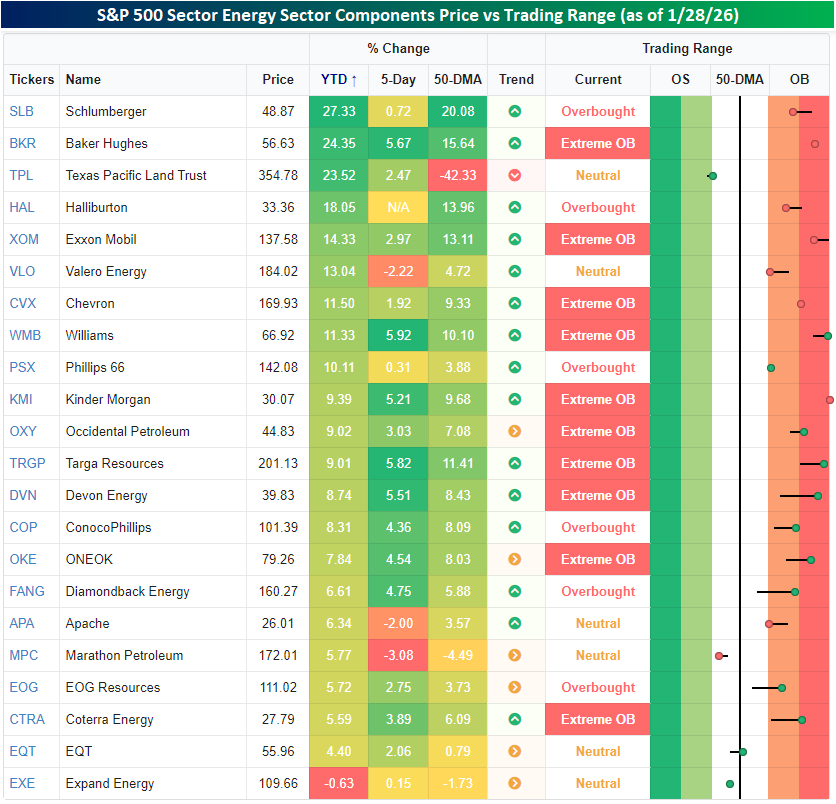

Crude oil prices are up over 12% this year, and natural gas enjoyed a surge during the cold snap, although the contract roll has brought front-month futures prices back down to a three-handle this morning. You don’t have to look any further than these moves in the underlying commodities to understand why energy stocks are doing so well, but strength within the sector, while broad-based, hasn’t been uniform.

As shown in the snapshot below, all but one of the sector’s 20+ components are up YTD. The only outlier is Expand Energy (EXE), which is fractionally lower for the year. On the upside, the two leading stocks in the sector this year have been Schlumberger (SLB) and Baker Hughes (BKR), with gains of more than 20%. Both stocks gapped sharply higher following the early January arrest of Maduro in Venezuela and basically haven’t looked back since. Of the nine stocks in the sector up at least 10%, though, there’s been a smorgasbord of exploration companies, integrated oil companies, and even refiners.

The Closer – Heavy Earnings, FOMC, Sovereign Samba – 1/28/26

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a quick recap of today’s FOMC meeting (page 1) followed by a review of the big earnings slate (pages 1 – 3). We then close out with some notes on Brazilian financing (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 1/28/26

Q4 2025 Earnings Conference Call Recaps: Union Pacific (UNP)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Union Pacific’s (UNP) Q4 2025 earnings call.

![]()

Union Pacific (UNP) operates one of North America’s largest freight rail networks, spanning 23 states across the western two-thirds of the United States. The company moves coal, grain, chemicals, intermodal containers, automotive products, and industrial materials, serving as a critical link in American supply chains. UNP’s performance can speak to the health of the US industrial economy, agricultural exports, energy markets, and truck-to-rail transportation. UNP reported record full-year results with EPS of $11.98 (up 8%), despite 4% volume decline in Q4. The company set best-ever records across safety, freight car velocity (239 miles/day), and terminal dwell (19.8 hours), the average time a railcar sits idle between trips. However, management issued conservative 2026 guidance with mid-single-digit EPS growth, citing 4%+ rail inflation, weak pricing power in agricultural and domestic intermodal markets, and deteriorating macro indicators. The pending $85 billion Norfolk Southern merger dominated the discussion. The STB requested additional information, including walk-away terms, delaying the application but not changing the first-half 2027 closing target. Management expressed confidence in approval, emphasizing competitive benefits and customer optionality. Reporting in-line EPS on a revenue miss, UNP shares rose 0.7% on 1/27…

Continue reading our Conference Call Recap for UNP by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q4 2025 Earnings Conference Call Recaps: ASML (ASML)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers ASML’s (ASML) Q4 2025 earnings call.

![]()

ASML (ASML) is the world’s sole provider of Extreme Ultraviolet (EUV) lithography machines, massive, €350 million rigs that use plasma-generated light to etch circuits onto silicon at the atomic scale. By serving giants like TSMC, Intel, and Samsung, ASML gives insight into the global tech roadmap. Without their systems, the advanced chips powering AI, 5G, and high-performance computing simply cannot be built. ASML concluded 2025 “with a bang,” reporting record Q4 net bookings of €13.2 billion, more than doubling year-over-year. This is fueled by the AI arms race, as customers accelerate transitions to 3nm and 2nm nodes. Management raised its 2026 revenue guidance to a range of €34 billion to €39 billion, citing a perfect storm of demand for AI logic and high-bandwidth memory (HBM). To sharpen its competitive edge, ASML announced a streamlining of 1,700 positions to focus on engineering innovation. EPS of $7.35 missed the $7.58 estimate on better-than-expected revenue, and shares fell roughly 2% on 1/28…

Continue reading our Conference Call Recap for ASML by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q4 2025 Earnings Conference Call Recaps: Starbucks (SBUX)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Starbucks’ (SBUX) Q1 2026 earnings call.

![]()

Starbucks (SBUX) is the world’s largest premium coffeehouse chain. The company sells handcrafted coffee and espresso beverages, teas, food, and ready-to-drink products, while also running one of the most sophisticated loyalty ecosystems in retail with over 35 million active US Rewards members. Starbucks serves daily ritual-driven consumers, from commuters to afternoon social customers, and offers insight into global consumer demand, pricing power, labor dynamics, commodity inflation (coffee), and urban real estate trends. Starbucks delivered a clear turnaround inflection in Q1, with global comps up 4% and US transactions growing year-over-year for the first time in eight quarters, driven by both rewards and non-rewards customers. Revenue rose 5% to $9.9B, while operating margin fell 180 bps to 10.1% due to labor investments, tariffs, and elevated coffee costs, which management expects to ease in the back half of FY26. The Green Apron service model improved throughput and customer satisfaction, while menu simplification and protein-driven innovation supported traffic. International comps rose 5%, with China comps accelerating to 7%. Starbucks also outlined its China joint venture with Boyu Capital. While missing EPS estimates, revenue came in better-than-expected, and SBUX shares opened 6.6% higher on 1/28, though lost momentum through the session…

Continue reading our Conference Call Recap for SBUX by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: Another 1,000 Points

3rd to Last Powell Fed Day

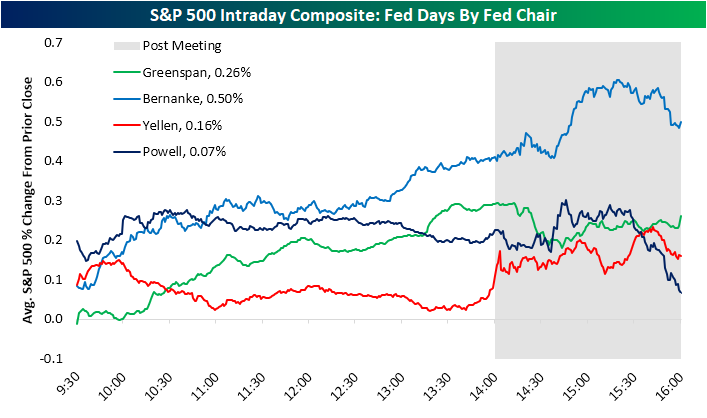

Today will be the 65th Fed Day (FOMC day) of Chair Powell’s tenure, dating back to early 2018 when he first took the helm. The US stock market has more than doubled since Powell became Fed Chair, so his tenure has been a big success in that regards even though stock market gains are not part of the Fed’s mandate.

When it comes to stock market performance on Fed Days specifically, however, Powell’s tenure has been the weakest of the “modern” Fed era.

The “modern” Fed began in February 1994 when they first began announcing policy decisions on the day of FOMC meetings. Before 1994, the Fed didn’t announce interest rate decisions until weeks after their meetings, which forced investors to monitor the Fed’s open market trading desk activity in the meantime for any policy adjustments.

There have only been four Fed Chairs in the modern era, beginning with Alan Greenspan, who was Chair when the Fed first began announcing policy decisions on FOMC days. After Greenspan came Ben Bernanke in 2006, Janet Yellen in 2014, and Jerome Powell in 2018.

Below we’ve created a chart that shows the S&P 500’s average intraday path on regularly scheduled Fed Days since 1994.

As shown, Bernanke saw the best stock market performance on Fed Days with an average one-day gain of 0.50%, followed by Greenspan at 0.26% and Yellen at 0.16%. Powell currently ranks last of the four with an average one-day gain of just 0.07% on Fed Days during his tenure.

Notably, Powell has actually been the best Chair for the stock market in the first half-hour of trading on Fed Days. From there, though, the market has tended to trickle lower under Powell and then sell off sharply in the final hour of trading.

There have been many-a-Powell Fed Days that saw sharp market selloffs after Powell press conferences. Not every Powell Fed Day has seen a late-day selloff, of course, but the “average” tells the overall story.

Again, the stock market is up huge since Powell became Fed Chair, so buy-and-hold investors have nothing to complain about when it comes to late-day weakness on Powell Fed Days.

For short-term traders, though, the “post-Powell-presser-plunge” will soon become a distant memory once a new Chair takes the helm this spring.

Not a Bespoke client? We’d love for you to give our equity research platform, Bespoke Premium, a try. You can sign up for complimentary access for 14 days at this link to read our full 2026 Investor Sentiment report and start receiving our daily research emails today!

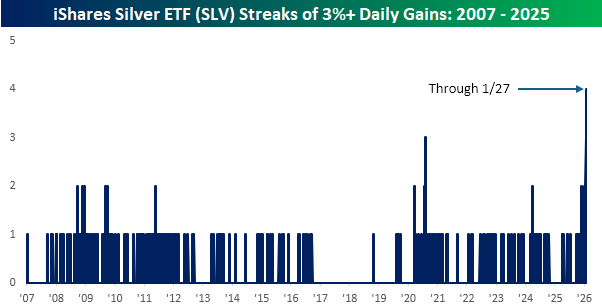

How Much More Precious Can They Get?

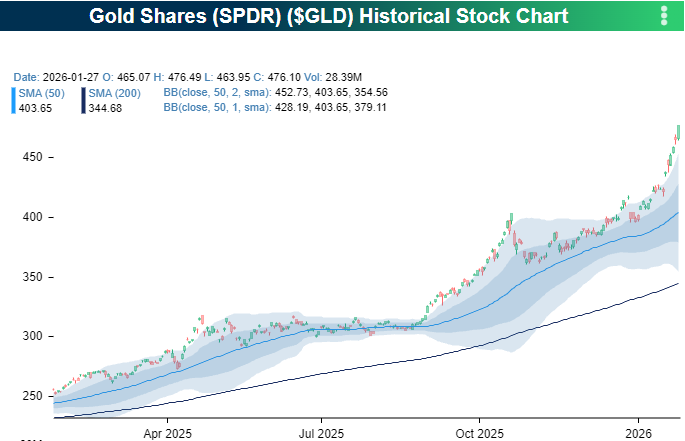

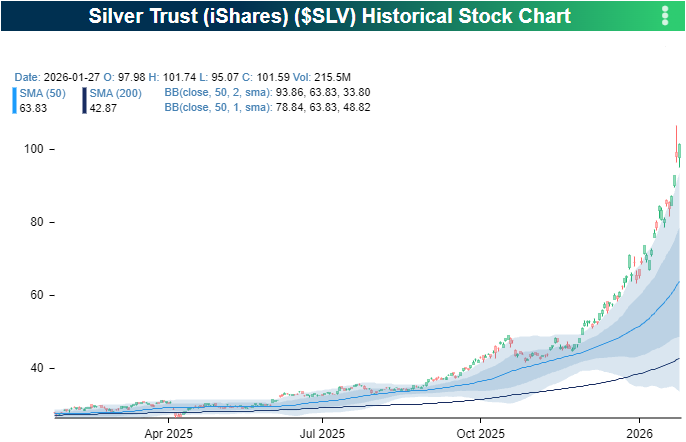

The moves in gold and silver have been getting crazy lately as the price charts of both precious (and getting more precious by the day) metals have turned parabolic in recent weeks. Through yesterday’s close, the SPDR Gold ETF (GLD) is already up over 20% YTD, while the iShares Silver ETF (SLV) has surged an unbelievable 62%. In normal times, these type of gains would be considered a great year!

The moves in GLD and SLV have left them extremely extended. GLD closed 38% above its 200-DMA yesterday, and SLV finished the session 137% above its 200-DMA. 137%!

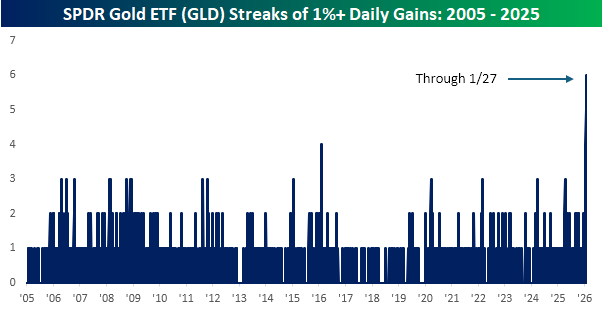

What makes the recent moves in both metals ETFs even crazier, though, is how persistent the gains have been. Through yesterday’s close, GLD traded more than 1% higher for six straight sessions. Before the current streak, the longest streak in the ETF’s existence since 2004 was only four days.

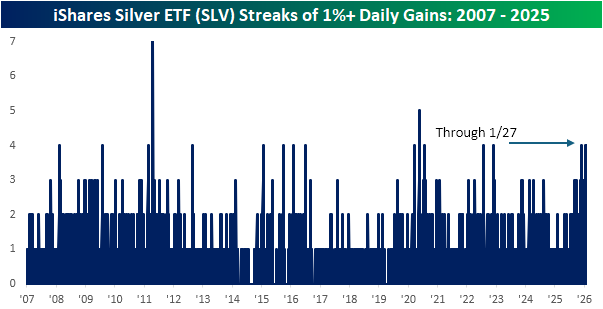

SLV’s streak of 1% daily moves has only been four trading days, and for a volatile commodity like silver, that’s peanuts. The current streak (through yesterday’s close) was actually the third four-day streak of 1%+ daily gains in the last two months! Since the ETF’s inception in late 2006, there have been several other four-day streaks, as well as a five-day streak that ended in 2020 and a seven-day streak ending in April 2011.

Silver (SLV) hasn’t just rallied 1%+ for four straight days, but rather 3%+ for four straight days. In SLV’s entire history, there was only one other streak that even lasted three trading days. If you own either of these ETFs or stocks exposed to them, it’s been a great ride, but just keep in mind that moves like these don’t last forever, and even if the ultimate peak for either metal is still on the horizon, the ride there won’t be smooth.

Not a Bespoke client? We’d love for you to give our equity research platform, Bespoke Premium, a try. You can sign up for complimentary access for 14 days at this link to read our full 2026 Investor Sentiment report and start receiving our daily research emails today!

Bespoke’s Morning Lineup – 1/28/26 – Broadening: The Word of 2026?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The future doesn’t belong to the fainthearted; it belongs to the brave.” – Ronald Reagan, 1/28/1986

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US equity futures are modestly higher again this morning, with the S&P 500 indicated to open up 0.25% while the Nasdaq is looking much stronger, gaining 0.85% as positive earnings reports in the Technology sector drive the sector’s gains. Investors are selling treasuries as the 10-year yield pushes 4.25%.

Gold is surging again today after yesterday’s comments by the President regarding the dollar, and the SPDR Gold ETF (GLD) has already rallied at least 1% for six straight days! Silver is also strong this morning, and the Silver ETF (SLV) has rallied at least 3% for four straight days! Investors are in such a ‘buy anything mode’ that even Bitcoin is rallying more than 1%, taking it back above $90K.

In Asia overnight, most major indices were higher. Hong Kong led the way with a gain of more than 2.5%, and South Korea’s Kospi tacked on 1.7%. A 40-year JGB auction in Japan was met with strong demand as the bid-to-cover ratio came in at 2.76, which was the strongest since last March. As we said, they’re buying everything this morning!

Well, maybe investors aren’t buying everything. In Europe, stocks are lower across the board. The STOXX 600 is down 0.5% with France, Italy, and Spain both down over 1%. Luxury stocks are weighing on stocks in the region following earnings from LVMH after the close yesterday, which we covered in last night’s Closer.

Today in the US, there’s no economic data on the calendar, but at 2 PM, the Fed will announce its latest rate decision, and the market is basically pricing in 100% odds of no change in rates. After the close, though, we’ll get earnings from Meta (META), Microsoft (MSFT), and Tesla (TSLA).

Merriam-Webster’s word of 2025 was slop which described the unending stream of low-quality, computer-generated content that has inundated the internet and social media feeds over the last three years. As much as AI promises to change life for the better, some of the more immediate impacts have been less than compelling. You can’t get away from it!

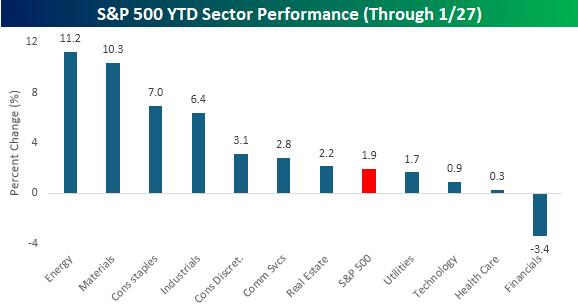

This is not even a month old, but if early indications are accurate, the term broadening could be a serious contender for the word of 2026. Looking at sector performance, the S&P 500 is up just under 2% YTD, but seven sectors have outperformed the index, including Energy and Materials, which are both up over 10%! Behind these two commodity-related sectors, Consumer Staples and Industrials are both up over 5%, while Consumer Discretionary, Communication Services, and Real Estate are all outperforming the index by a small degree.

On the right side of the S&P 500, Technology sticks out like a sore thumb with its gain of less than 1%. Along with Technology, Utilities, and Health Care are also up YTD but still underperforming, while Financials, which started the year off hitting all-time highs, is the only sector in the red for the year.

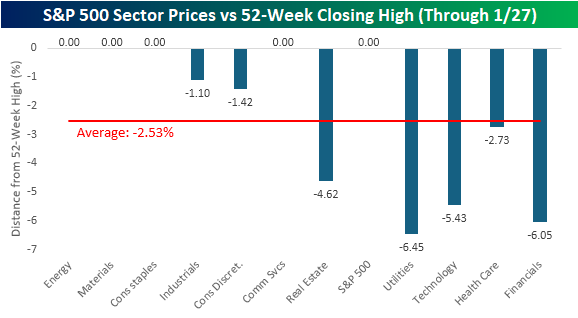

With the market broadening, we found it notable that, along with the S&P 500 yesterday, four sectors also closed at 52-week highs yesterday. Even many of the sectors that didn’t hit new highs yesterday aren’t far. Industrials and Consumer Discretionary are both within 2% of a 52-week high, while Utilities, Financials, and Technology are the only three sectors down more than 5%. The fact that the S&P 500 closed at a record high yesterday and its two largest sectors (Technology and Financials), which together account for nearly half of the entire index, are both down more than 5% from their highs is remarkable.

Regarding yesterday’s trivia, the five other schools to produce a Super Bowl winning QB and at least one US President are:

– Delaware: Biden/Flacco

– Miami (OH): Harrison/Big Ben

– Michigan: Ford/Brady

– Stanford: Hoover/Elway/Plunkett

– Navy: Carter/Staubach

Now to the bonus question. Of the 36 different head coaches to win a Super Bowl title, the school the college/university that has produced the most winning head coaches is Miami University of Ohio. The three Super Bowl-winning coaches who went there were Weeb Ewbank, John Harbaugh, and Sean McVay. Congratulations to everyone who got it right.