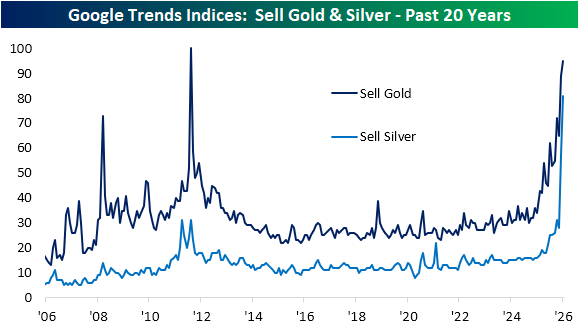

Precious Search Interest

Today has been another volatile session for gold and silver prices, with the former up over 7% as of this writing and the latter up well over 15% versus yesterday’s close.

The huge move higher (and lower) in precious metals has resulted in surging interest from consumers based on Google search interest.

Google Trends tracks and indexes search interest on Google’s search engine for a given word or phrase over a given time period. Readings of 100 indicate the peak for search interest, readings of 50 would be half of that peak, and so on.

As shown below, the latest surge in gold and silver prices has corresponded with a surge in search interest for both “sell gold” and “sell silver.”

For gold, search interest is approaching August 2011 records, whereas the reading for sell silver is now far and away at record highs. In other words, people have record or near record interest in selling their precious metals.

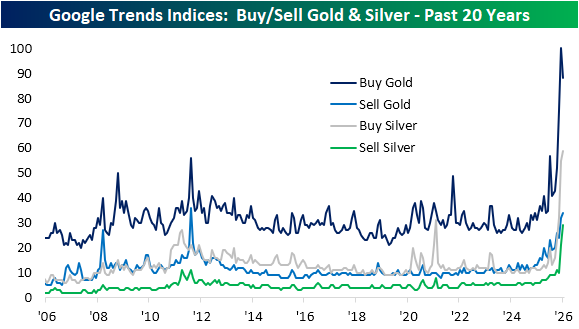

Amazingly, though, search interest for “buy gold” and “buy silver” has also surged to record highs that are at levels much higher than the “sell” version of the phrase. As prices have skyrocketed, more people seem to be interested in buying gold and silver than selling them.

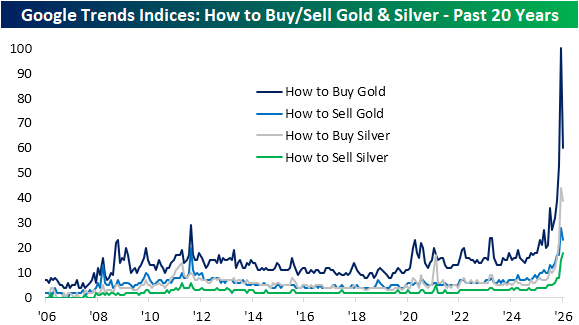

We also like to look at “How to” searches. These can proxy first time buyers or sellers, or alternatively, more casual investor interest. Again, these indices are broadly elevated and hit new records by massive margins recently. As shown below, searches for “how to buy gold” have skyrocketed as gold prices have gone parabolic, while the “how to sell” versions have also jumped but not by nearly as much.

Bespoke’s Morning Lineup – 2/3/26 – Europe Rises to the Top

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The way we do things is to begin.” – Horace Greeley

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Make sure to check out Paul Hickey on CNBC’s Squawk on the Street today at 10 AM!

Futures on the S&P 500 and Nasdaq are slightly higher this morning, as the Dow trades slightly lower. Nasdaq futures are leading the gains following a positive earnings report from Palantir (PLTR), which has the stock trading up over 10%. Treasury yields are moving higher again as the 10-year yield sits just under 4.29%, and crude oil is slightly higher. Precious metals are really in rally mode as Gold trades up over 6% and Silver is up more than twice that in percentage terms. If you were looking for things to calm down in that space, don’t hold your breath.

The only economic report on the calendar this morning is JOLTS at 10 AM, but right before that, at 9:40, Fed Governor Bowman will be speaking at a WSJ conference. On the earnings front, some of the key companies reporting after the close will be AMD, Amgen (AMGN), and Mondelez (MDLZ)

So much for that sell-off in Asian stocks to start the week. Overnight, the Nikkei surged nearly 4% to a new all-time high. Not to be outdone, the KOSPI spiked nearly 7% briefly causing another halt to trading, after Monday’s downside halt. Both Palantir’s (PLTR) positive reaction to earnings and the US India trade deal have acted as catalysts for the gains. India’s Sensex also rose over 2.5% in the wake of the trade deal, which would cut tariffs on Indian imports to 18%, and India would agree to stop buying Russian oil. All of this news overshadowed a rate hike in Australia from the RBA, which was widely expected, but the central bank did suggest tighter policy could continue as inflation accelerates.

Yesterday, it was Europe benefiting from its lack of technology exposure, but this morning, that isn’t the case. While stocks in the region are generally positive on the session, the gains are much more muted relative to Asia. The STOXX 600 is barely holding on to gains while the UK and France are both in the red.

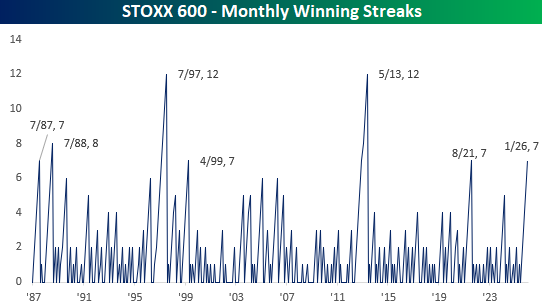

After two weeks of sideways trading, European stocks went into lift-off mode yesterday as the STOXX 600 surged more than 1% to a new all-time high. This morning, the European benchmark index added to those gains before pulling back modestly, although it’s still up for the day. YTD, the STOXX is already up over 4%, or more than twice the 1.9% gain for the S&P 500.

Like the Dow Jones, which has had nine months in a row of gains, the STOXX 600 has been up for seven straight months. That ranks as tied for the longest streak since May 2013 and tied for the fourth-longest on record.

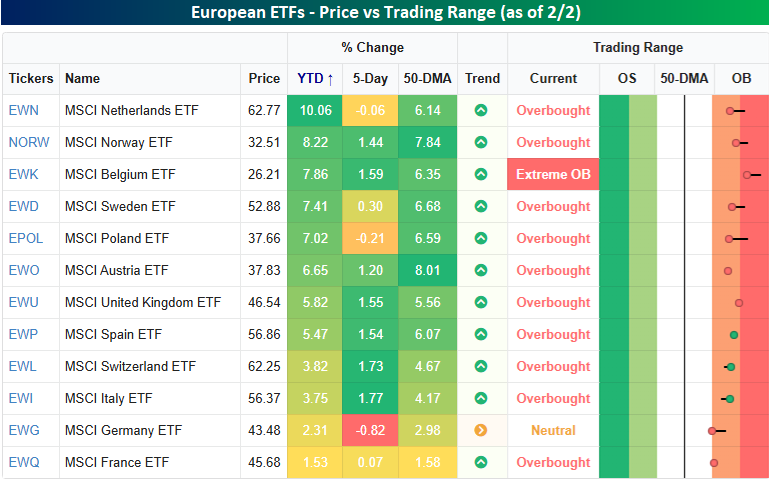

Looking at individual country performances within Europe, the snapshot below from our Trend Analyzer shows the performance of country ETFs on the continent. Of the 12 ETFs shown, all of them are up YTD, and France is the only one underperforming the S&P 500. Most of the countries have outperformed the US by a wide margin. The Netherlands (EWN) ETF is up over 10% already this year, and seven other countries have gained at least 5%. Most of the countries are also comfortably above their respective 50-day moving averages and well into short-term overbought territory. The only exception is Germany (EWG), which is also down the most over the last week (-0.82%).

It’s also interesting to note that most of the strength in European stocks this year hasn’t been coming from major economies like Germany, France, Italy, and Spain. They’re all at or near the bottom of the performance list. Instead, it’s the less talked about countries like the Netherlands, Norway, Belgium, and Sweden leading the way.

The Closer – Earnings, PMIs, Smart vs. Dumb Money – 2/2/26

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with commentary regarding today’s volatility across assets in addition to the damage that has been done to some technical pictures given these moves (pages 1 and 2). Next, we review the odd bear market for software stocks (pages 2 and 3). We follow up with earnings recaps and a quick review of today’s economic data (pages 4 and 5),

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 2/2/26

Bespoke Market Calendar — February 2026

Please click the image below to view our February 2026 market calendar. This calendar includes the S&P 500’s historical average percentage change and average intraday chart pattern for each trading day during the upcoming month. It also includes market holidays and options expiration dates plus the dates of key economic indicator releases.Click here to view Bespoke’s premium membership options.

Q4 2025 Earnings Conference Call Recaps: Meta Platforms (META)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Meta Platforms’ (META) Q4 2025 earnings call.

![]()

Meta Platforms (META) builds the social fabric of the internet through its Family of Apps, including Facebook, Instagram, WhatsApp, and Threads. With over 3.5 billion daily users, Meta makes communication tools and advanced AI models, monetizing this massive engagement via a sophisticated advertising ecosystem. While Meta is known as a social media giant, it is developing into a deep technology company, now looking to pioneer what it calls personal superintelligence and making proprietary silicon and global-scale energy infrastructure to power the next generation of computing. In Q4, revenue grew 24% YoY to $59.9 billion, funded by record-breaking holiday ad demand. However, the focal point was a 2026 capital expenditure guide of $115–$135 billion, nearly double 2025 levels, to build out Meta Superintelligence Labs and a new organization, Meta Compute. Zuckerberg is pivoting from the metaverse toward AI-powered wearables, noting that Ray-Ban glasses sales tripled last year. Internally, Meta is seeing a macro-shift in productivity. The company claims that AI coding tools have increased engineer output by 30%, allowing single contributors to handle tasks previously requiring entire teams. After reporting a triple play, the stock rose 10.4% on 1/29…

Continue reading our Conference Call Recap for META by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q4 2025 Earnings Conference Call Recaps: Tesla (TSLA)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Tesla’s (TSLA) Q4 2025 earnings call.

![]()

Tesla (TSLA) designs and manufactures electric vehicles, battery energy storage systems, and humanoid robots. Beyond its mass-market Model 3 and Y, the company is distinguished by its “Physics First” engineering and in-house semiconductor design. Tesla serves a global market of tech-forward consumers and utility-scale energy providers, offering insight into the convergence of autonomous mobility and domestic manufacturing. It is currently the only major US automaker operating its own lithium and cathode refineries. Tesla is undergoing a historic pivot, prioritizing an autonomous future over traditional hardware. Management announced the “honorable discharge” of the legacy Model S and X lines, as CEO Elon Musk put it, to convert Fremont factory space for Optimus robot production, targeting 1 million units annually. Despite 2025 delivering Tesla’s first annual revenue decline (falling 3% to $94.8B), the stock rose initially on news of a massive $20B+ CapEx plan for 2026, more than double previous guidance. This capital will fund six new factories and a domestic TerraFab to mitigate geopolitical chip risks. Tesla also confirmed a $2B investment in xAI to integrate Grok for fleet management. While the energy business hit record profits ($12.8B revenue), the focus is now squarely on the April Cybercab production launch and the transition to a subscription-only FSD model. Despite a higher open on 1/29 after posting better-than-expected results, shares fell intraday and closed near session lows, down 3.5% on the day…

Continue reading our Conference Call Recap for TSLA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke’s Morning Lineup – 2/2/26 – At Least It’s the Shortest Month

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Shut your eyes and see.” – James Joyce

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a shaky end to the week and the month for US markets on Friday, things remain somewhat unsteady as we kick off the new month. S&P 500 futures indicate a 0.3% decline at the open, while the Nasdaq is priced to open down twice as much. For both indices, current levels are well off their lows so that it could have been a lot worse.

Treasury yields are slightly lower, with the 10-year yield starting the week at 4.23%. Crude oil is sharply lower, trading down close to 5% as President Trump suggested that the Iranians are looking to come to the bargaining table. In the metals space, it’s a mixed picture with gold up about 1% while silver bounces over 6%. Copper and Platinum, meanwhile, are both lower. After moves like we saw late last week in the space, though, we would expect more wild trading in the days ahead. These types of volatility spikes have a way of lasting more than a few days before things finally settle down.

It was a negative start to the week in Asia as the Nikkei fell over 1%, while Hong Kong and China both slumped by more than 2%. The big loser, though, was South Korea, where the KOSPI plunged over 5%, and trading briefly came to a halt because of circuit breakers. The weakness in that index stemmed from a weekend story in the WSJ where Nvidia CEO Jensen Huang said that the company’s investment in OpenAI will not be the $100 billion previously reported, and that has raised new concerns about the vitality of the AI trade.

Today is one of those rare days, it seems, where the lack of a vibrant technology sector in Europe is a plus. The STOXX 600 is up 0.4%, and the German DAX and Spain’s IBEX 35 each rally over 0.75%. Better-than-expected manufacturing PMIs for January have also acted as a positive catalyst.

In the US today, the only economic report on the calendar is the ISM Manufacturin,g which is projected to rebound slightly from December’s reading of 47.9. Given the surprise strength in the Chicago PMI last week, though, don’t be surprised if that report comes in hot. Outside of economic data, the first major tech report of the week will be Palantir (PLTR) after the close. As we detailed in today’s Chart of the Day, growth-oriented sectors of the market have been messy lately, so PLTR’s report could have big implications for the sector.

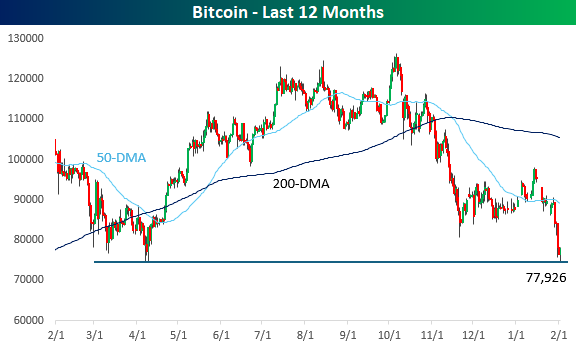

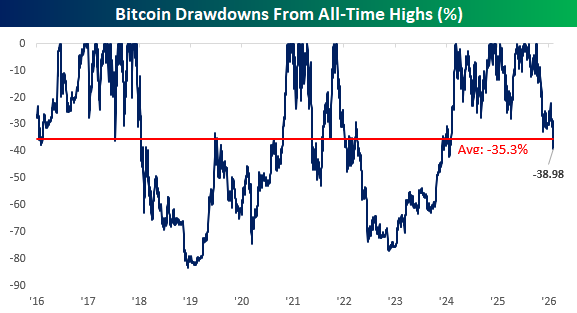

Along with growth-oriented stocks, crypto assets have been terrible performers for the last few months, and over the weekend, Bitcoin tested 52-week lows near $75K. Prices are rebounding slightly this morning along with equity futures, but the burden of proof is firmly on the back of the bulls now as Bitcoin’s price trades near the breakeven price for all of Strategy’s (MSTR) holdings.

While it’s been a painful few months for crypto, it’s worth pointing out that this remains just a run-of-the-mill decline for Bitcoin. While it’s currently down about 39% from its all-time high, on any given day since 2016, its average drawdown from an all-time high has been over 35%.

Chart of the Day – Messy Market

Brunch Reads – 2/1/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Dedicated to Definitions: On February 1, 1884, the Oxford English Dictionary debuted. Although not as a finished book, it was the first published installment of what would become the most ambitious language project ever attempted. The opening collection, covering words just from A to Ant, was released in London after decades of preparation. It was the start of a project seeking to document every English word, its meanings, and its history.

The project began in the 1850s. Under editor James Murray, thousands of volunteers, including teachers, clerks, scholars, and even inmates, submitted millions of handwritten quotation slips showing how words were actually used across centuries. Murray famously worked from a backyard “scriptorium,” surrounded by pigeonholes stuffed with these citations. What readers got in 1884 was only a glimpse of the scale to come. The full dictionary wouldn’t be completed until 1928, more than 40 years later, spanning 10 volumes.

AI & Technology

AI Productivity’s $4 Trillion Question: Hype, Hope, And Hard Data (Forbes)

While individual tasks like coding and customer service show efficiency spikes as high as 55%, AI has yet to move the needle on national economic growth. This disconnect stems from a staggering 95% failure rate in corporate pilots and a skill-leveling effect where the technology primarily boosts underperformers while occasionally slowing down experts. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.