Buyers Take the Afternoon Off

Last Friday we played Spot the Pattern, but today the question is, “Can you find the outlier?” The first four trading days of June were characterized by solid and steady buying in the afternoon hours (on Monday there was a brief sell-off shortly after noon ahead of Fed Chair Janet Yellen’s speech), but on Tuesday, buyers took the day off. What was a nice gain near the highs of the year around 1:30 PM ET turned into a small gain of just about 0.10% by the close. Didn’t you like it the other way around?

Biotech Stalls Out

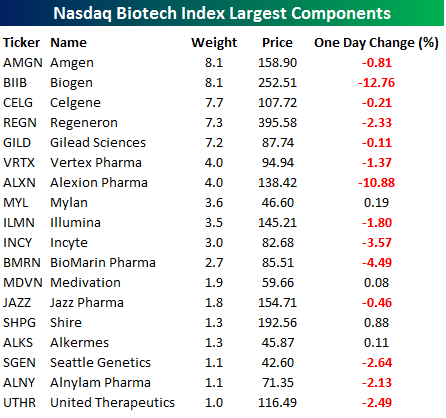

US equities closed off their intraday highs, but the Dow and S&P 500 still managed to finish in the green (just barely). The Nasdaq, however, couldn’t hold on and finished the day down 0.14%. One of the big culprits behind the weakness in the Nasdaq was the biotech sector, which was down sharply all day. The Nasdaq Biotech index fell more than 2.5% for its worst day since 5/11. While the sector has made a series of higher lows since February, the most recent rally leading up to last weekend’s ASCO conference looks to have run out of steam right at resistance corresponding to the 2015 lows and the peak of two failed rallies in January and April. It also corresponds to the downtrend from last year’s peak. Until these resistance levels can be taken out, the sector’s downtrend remains intact.

Today’s weakness in the sector was broad-based, as losers outnumbered winners by a margin of nearly 4-1 (146-41). However, there were definitely some stocks that were bigger losers than others. The table below lists the 18 stocks in the Nasdaq Biotech Index that have a weighting of 1% or more. Of those names, 14 were down on the day and just 4 were up. Of the dozen losers, the biggest decliners were Biogen (BIIB) and Alexion (ALXN), which were both down more than 10%. On the upside, Shire was the biggest winner, but it still couldn’t even manage a gain of 1%. Certainly a day to forget.

ETF Trends: US Sectors & Groups – 6/7/16

Below is our daily list of the twenty best and twenty worst performing ETFs over the last five trading days. Hedged European and Japanese indexes continue to perform poorly as the USD remains strong. Eight of the top 12 performers are related to natural resources, a group which includes gold, gas, oil, and steel stocks in addition to coffee. NASDAQ Biotech flipped from the top performer list to the worst performer list but remains marginally positive. Broad bond market and Treasury exposures have underperformed but are mostly still positive or neutral. Financial sector stocks continue to struggle with Capital Markets, Financial Services, Banks, and Financials all in the red as interest rates at the front end of the curve decline on a more dovish Fed. Latin America, Emerging Latin America, and Brazil are among the top performing regional ETFs.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Bespoke Stock Scores: 6/7/16

Chart of the Day – 6/7/16: The Greenback Tide

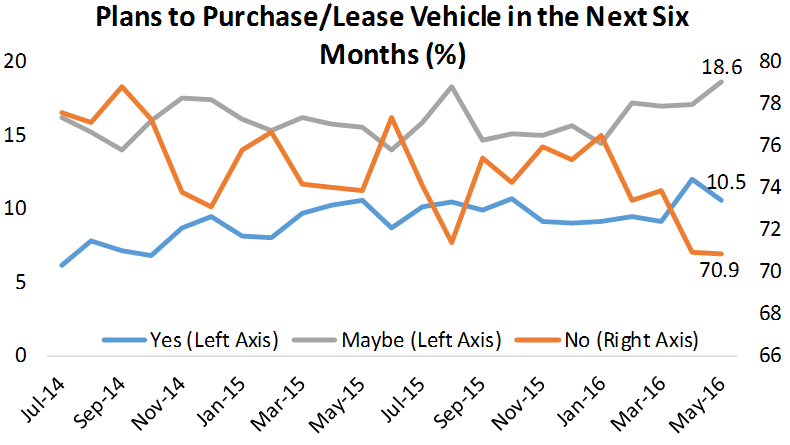

Consumer Pulse: Auto Loans Setting Records

Record Setting Auto Loans: As vehicles continue to cost more, Americans are doing everything they can to pay for them, which means borrowing more and extending loan terms to make monthly payments easier to digest. Last week, data from Experian showed that Americans are borrowing for auto loans at record rates across the board. According to Experian, the average auto loan is $30,032, which is the first time in history this number has breached the $30,000 mark. Americans are also extending their loan terms to an average of 68 months, which is the longest average term ever. Finally, the average monthly payment is $503, which is the first time the average auto payment has topped the $500 mark.

Survey Says: There is little to no sign of this trend slowing down. In our monthly Consumer Pulse survey of 1,500 US consumers balanced to census, we ask participants if they plan on purchasing or leasing a vehicle in the next six months. As shown in the results for this question below, the trend is definitely towards an increased rate of purchase. The share of consumers that are considering a purchase over the next six months is up to a new high, while the share that are sure they will buy or lease in the next six months is close to its highest level in our survey’s history. Definitive “no” responses are also at new lows.

You can see our entire data-set of proprietary survey analysis with a 30-day free trial to our Consumer Pulse offering. We have said it before, but we’ll say it again: The value in the Bespoke Consumer Pulse offering is tremendous. We strongly encourage you to give our Consumer Pulse subscription a try!

Click here to learn more about the Consumer Pulse offering, or go ahead and start a 30-day free trial using one of the checkout links below.

Annual — Bespoke Consumer Pulse — $365/Year w/ 1-Month Free Trial

Monthly — Bespoke Consumer Pulse — $39.99/Month w/ 1-Month Free Trial

Bespoke Briefs — Market Breadth — June 2016

The Closer 6/6/16 – “Ready For Rollover”

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we chart the FOMC’s Labor Market Conditions index and highlight three possible options trades to take advantage of extremely low volatility.

The Closer is one of our most popular reports, and you can sign up for a trial below to see it and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

Energy Spreads Keep Compressing

The rebound in the Energy sector continued once again today as the Philadelphia Oil Services Index rallied 9% for its best day since March 2009. Today’s rally in that part of the Energy sector followed a strong rally in credit last week where spreads on high yield rated debt of companies in the Energy sector compressed further below 1,000 basis points (bps) to their lowest level since last July.

While spreads on high yield debt are near their lowest levels in a year, the equities of companies in the sector still have quite a ways to go before recouping all of their losses since last July, when spreads were last at their current levels. At a current level of 504, the S&P 500 Energy sector still hasn’t taken out its highs from this April and late last year, let alone last July.